The "Go Back to Work" Argument for Early Retirees: Why It Ignores How Hiring Actually Works

Early retirement isn't idleness—it's the payoff of decades of disciplined saving. Photo by ping lee on Unsplash.

Reading time: 7 minutes

Quick Answer

The "early retirees should go back to work" argument sounds compelling in the abstract—but it underestimates three hard realities: age discrimination in hiring is well-documented and begins as early as the mid-40s; skill half-lives are compressing; and AI is reshaping which roles remain open to career returners. For anyone pursuing Financial Independence, this debate has direct practical implications. Relying on uninterrupted employment until 65 may be riskier than it looks.

What You'll Get From This Article

✔ Why the "early retiree golfers should return to work" narrative rests on shaky labor market assumptions

✔ What academic research says about age discrimination and callback rates

✔ How AI and compressing skill cycles are raising re-entry barriers for older workers

✔ What this means concretely for your FI timeline and career optionality

✔ A practical FI planning takeaway: how to build optionality before you need it

TL;DR — Should Early Retirees Return to Work? 🏌️💼

The macro argument is familiar: ageing populations in developed economies need more workers. But the micro reality is messier.

🎯 Age discrimination in hiring is real and begins as early as the mid-40s—documented across US, UK, and OECD studies

📉 Skill half-lives are shortening; in fast-moving fields, half your knowledge may be outdated within 5 years

🤖 AI is compressing hiring selectivity—making re-entry harder for older workers, not easier

🏌️ The "golfers on the course" framing obscures what early retirement often is: decades of disciplined saving and planning

💡 For FI seekers, the real risk isn't retiring too early—it's assuming you can work until 65 and finding out too late you can't

🔑 Build financial optionality early; treat continued employment as upside, not baseline

⚠️ Policy pressure without incentive change doesn't move labor markets—people respond to incentives, not guilt

👉 Curious where you stand in relation to early retirement? The numbers matter more than you might think—our free FI Calculator is linked at the bottom of this article.

Should early retirees Go Back to Work? The Reality Behind the Latest “Work Harder” Narrative

A recent Guardian column,“Get early retirees off the golf course and back to work”, argued that early retirees in the UK should return to the workforce to support economic growth, echoing similar calls from policymakers like Friedrich Merz in Germany for citizens to work more and longer.

The framing carries a strong moralizing undertone—but it rests on assumptions about hiring, age, and labor market re-entry that don't hold up to scrutiny. It's also a version of a broader set of criticisms levelled at the FIRE movement—that early retirees are some sort of drain on society, that the math doesn't hold up, or that they'll eventually be forced back to work anyway.

In this piece, we examine what the research shows about age discrimination and skill obsolescence, why the "return to work" case is weaker than it sounds, and what this means concretely for anyone building toward Financial Independence and redesigning their career on their own terms (FI).

But the macro argument only holds if the labor market actually works the way the narrative assumes—and that's where things get more interesting.

The 'Return to Work' Argument — and Its Hidden Assumptions

The Guardian’s piece makes a familiar macroeconomic argument: in light of ageing populations and increasing fiscal pressure, the UK economy would benefit if more early retirees returned to paid work. The logic is about boosting the tax base, easing labor shortages, and improving overall productivity.

Similar to political messaging elsewhere in Europe, the framing carries a subtle civic dimension: working longer is presented not merely as economically beneficial but as socially responsible. This echoes, in part, the same “do your part” rhetoric we examined in the Merz debate, where increased labor participation is presented as some form of collective duty rather than individuals making rational choices based on existing incentives.

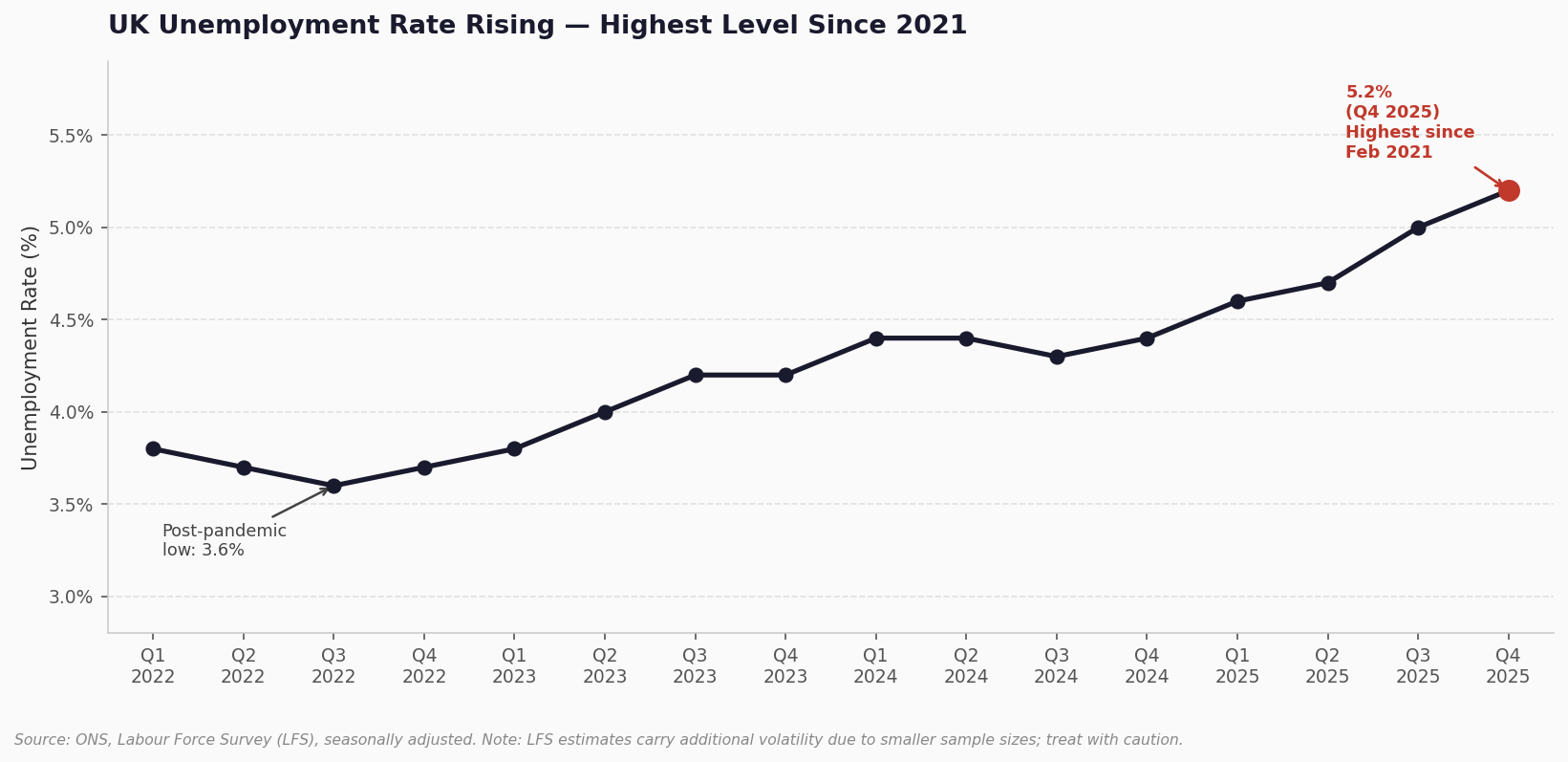

But this narrative does not fully fit current labor market data.UK unemployment, while still low by long-run historical standards, has risen steadily from its post-pandemic trough of 3.6% to 5.2% by Q4 2025, its highest level since early 2021 (Figure 1). Youth unemployment has climbed sharply in parallel. This is not the picture of a labour market straining for workers and eager to absorb early retirees back from the golf course.

Economists point to sectoral labor shortages—for example, in healthcare, logistics, and skilled trades—but that is different from stating that the economy can seamlessly absorb large numbers of older retirees.

Figure 1. UK unemployment has risen steadily since its 2022 trough and hit its highest level since 2021 by end of 2025. Source: ONS Labour Force Survey (seasonally adjusted).

This distinction matters, because when commentators talk about labor shortages in the abstract, they tend to simplify a messy reality of skills mismatches, geographic constraints, and employer preferences that shape actual hiring decisions on the ground.

Most importantly, the argument treats labor supply as almost frictionless, as if 60-year-old retirees could simply decide to re-enter the workforce and employers would eagerly absorb them. In reality, successful re-entry requires alignment across multiple layers: current skills, employer demand, wage expectations, health, and hiring bias.

There is also the practical reality of the modern hiring process itself. In many countries, applying for jobs has become a very lengthy and often demoralizing experience involving multiple interview rounds, automated screening systems, personality tests, and weeks—or months—of uncertainty. I personally went through two major job changes in the last ten years in two different European countries, and each transition required close to a year to materialize.

Anyone who has gone through a serious job search knows how draining it can be, even in their 20s or 30s. Asking people who have already managed to retire to voluntarily re-enter that process, potentially facing age bias and corporate bureaucracy, purely out of a sense of economic patriotism is quite a strong ask.

Once you start to examine some of these frictions, the simple macro story begins to look far less convincing, especially for professionals who’ve spent time inside the hiring process.

Some early retirees do return to work—but on their own terms and with the right incentives, not because a columnist told them to. Photo by Marcus Aurelius on Pexels.

What Research Actually Shows About Age Discrimination in Hiring

Academic evidence on age discrimination looks remarkably consistent across countries. Resume audit studies in the US, UK, and broader OECD economies repeatedly find that callback rates for older job applicants begin to decline meaningfully as early as the mid-40s—well before most workers consider themselves at risk of age discrimination in hiring—and fall further into their 50s and early 60s.

Of course, there are important exceptions. Highly specialized experts, senior executives, or individuals with rare skills can remain extremely attractive in the job market well into their 50s or 60s. But those roles represent a small fraction of the overall labor market. Most workers compete in far more crowded hiring pools where small perception differences—energy, adaptability, long-term potential—can tilt decisions toward younger candidates.

One well-known US empirical study found older applicants had to submit significantly more applications to receive the same number of callbacks as younger candidates, even when qualifications were held constant. UK evidence is thinner but directionally similar, and OECD reports have long documented lower re-employment rates and longer unemployment durations for older workers.

But why does this happen when most firms explicitly deny age bias in their hiring process? Because the underlying incentives are aligned that way. Employers naturally perceive younger hires as more trainable, more adaptable to new technologies, and more likely to remain with the firm longer, extending the potential return on training investment.

Salary expectations can also play a role: it’s a fair assumption to expect that mid-career candidates will demand higher compensation or greater flexibility compared to younger hires. Of course, none of this is written down explicitly as company policy, but the outcome shows up nonetheless through coded language, talking about “energy,” “cultural fit,” “trajectory,” or “long-term potential.”

This is one of the key blind spots in the “golfers should go back to work” narrative. If labor markets systematically tilt towards younger workers, then the pool of willing older workers is not the same as the pool of employable candidates. Employers facing competitive pressures and rapid technological change often see older hires as risky.

But data only tells part of the story. What does age bias actually look like when it plays out inside a real hiring process?"

Audit studies show callback rates for older applicants decline as early as the mid-40s—well before most workers expect it. Photo by Edmond Dantès on Pexels.

Inside One Hiring Room — What Bias Actually Looks Like

Earlier in my career, I experienced this from the other side of the hiring table. In one hiring round at my consultancy, we had three finalists for a technical role whose qualifications were almost indistinguishable. I know because I had been tasked with finding candidates with very advanced technical skills, and had significant influence over who made the final round—though not the final say.

Similar experience, similar technical assessments, and similar communication skills. Yet when the final decision came down, two offers went to the two younger candidates in their late 20s and early 30s. The candidate in his mid-40s was left out. The explanation was never framed as age; our boss framed it as perceiving the two winners as more “dynamic” during their interview and being of a gut-feel decision.

At the time, nothing about the decision felt discriminatory. But this is how most age bias manifests in modern professional environments: through soft signals and gut feelings rather than explicit exclusion. Hiring managers or bosses won’t say “we prefer the younger candidate,” but the adaptability, energy, and growth potential they talk about correlate in practice with age.

Each decision looks reasonable in isolation. The pattern only becomes visible—and troubling—when you zoom out. For mid-career professionals and especially for would-be returners, this matters a lot. If highly qualified candidates in their 40s can lose out in competitive processes despite near-identical profiles, the idea that large numbers of retirees in their 60s can smoothly re-enter the workforce looks naive at best.

I want to be careful not to overgeneralize from a couple of my personal experiences—hiring outcomes vary by sector, firm size, and role level. But the pattern I observed in that role and in others is consistent with what the academic literature documents at scale: soft signals often carry more weight than objective qualifications, and those signals tend to correlate with age.

AI is compressing skill half-lives and raising the bar for re-entry—the modern workplace moves faster than ever. Photo by Josh Sorenson on Unsplash.

AI, Skill Half-Lives, and Why Mid-Career Risk Is Rising

Age dynamics alone would be enough—but there's a second force compounding re-entry risk. Researchers increasingly talk about the “skill half-life”, which represents the time it takes for half of what professionals know to become outdated. In fast-moving fields, estimates have fallen toward the five-year range. The ongoing deployment of AI tools is likely to compress this cycle further—automating routine tasks, reshaping workflows, and raising the bar for re-entry for older workers returning to the job market after a career break.

The reality is that technological disruption can affect workers at both ends of the age spectrum—but in different ways. Younger workers may face fewer entry-level opportunities as automation replaces routine tasks, while older workers face steeper re-entry barriers because the skills they built their careers on can become obsolete faster than they can be updated. The thread running through both is the same: when technology raises productivity, employers simply become pickier.

We can also observe a clear generational tension here. If entry-level hiring is starting to become more constrained in some sectors due to automation and slower hiring, pushing large numbers of retirees back into the workforce could intensify competition for a smaller number of roles. In sectors already struggling to absorb graduates and younger workers, do we really want to encourage early retirees to return from the golf course?

As writers like Financial Samurai have argued, the more prudent stance in a rapidly unraveling AI environment is not to assume stable, linear careers into one’s mid-60s. Instead, the emerging risk profile looks more complex: long stable runs for some, but sharper and earlier dislocations for others.

If skill relevance cycles are shortening and hiring filters tightening, the probability of involuntary mid-career disruption increases, even for high performers. This is where the standard “just keep working until 65” advice starts to look dated. It assumes a stable, predictable labor market—and that assumption is looking increasingly shaky.

So what does all of this mean practically, for someone building toward Financial Independence today?

If policymakers want more older workers in the labor market, incentives will work far better than moral pressure. Photo by Andy Gill on Unsplash.

What This Means for Your FI Plan — and Why the Policy Debate Misses the Point

From a Financial Independence perspective, the lesson is not necessarily to “retire as early as possible,” but rather that the priority in this era is to build optionality before you need it.

The prevalent narrative (like the Guardian column) often frames early retirement as a lifestyle luxury, something pursued by golf enthusiasts stepping away from productive work to become lazy. But as AI disruption unfolds, for many professionals, pursuing FI may function more like insurance against increasing labor market fragility.

If age discrimination is real and skill cycles are compressing, then planning to rely on continuous employment until your mid-60s may be an extraordinarily risky assumption to make.

Encouraging older workers to remain economically active can make sense at the margin in specific sectors. Experienced professionals often bring valuable institutional knowledge, judgment, and client credibility that younger teams sometimes lack. But policy aspirations cannot override market incentives. Firms hire based on expected return, productivity, and adaptability—not on appeals to a sense of social duty.

If policymakers genuinely want more people to remain in the workforce longer, the solution is unlikely to be moral pressure or public scolding. As we discussed in the Merz debate, people respond to incentives. Higher wages for scarce skills, better working conditions, flexible work arrangements, or lower taxes on additional working hours would all do far more to encourage longer participation than telling retirees to leave the golf course out of a sense of civic duty.

For FI readers, the practical takeaway is straightforward. Plan financially as if your peak earning window may end much sooner than the official retirement age—perhaps in your early-to-mid-50s. Treat any additional working years as upside rather than a baseline. A continuous, uninterrupted 40-year career may already be becoming the exception rather than the rule. If you haven't stress-tested your own timeline against that assumption, our FI Calculator at the end of this article is a good place to start.

Pursuing Financial Independence preserves freedom and optionality. If you love your work and opportunities remain strong, you can continue to work as long as you like from a position of strength. But if labor market realities shift, whether due to age dynamics, AI disruption, or sectoral changes, you are not forced into a late-career scramble precisely when re-entry becomes hardest.

If you enjoyed this article, here are some next steps:

👉 Want the complete framework for building career optionality through Financial Independence? See our complete guide to work, purpose, and Financial Independence

👉 New to Financial Independence? Start with our complete guide to FI and FIRE

👉 Use our free FI Calculator (email unlock) to stress-test your early retirement timeline

👉 Related reading:[Friedrich Merz wants Germans to work harder — is he right?

👉 Subscribe to get free FI tools and the weekly newsletter (one-click unsubscribe)

👉 Browse 130+ articles on FI, investing, work, and health at The Good Life Journey

💬 What do you think: is the 'return to work' case stronger than the data suggests? Share your view in the comments.

🌿 Thanks for reading The Good Life Journey. I share weekly insights on personal finance, financial independence (FIRE), and long-term investing — with work, health, and philosophy explored through the FI lens.

Disclaimer: I’m not a financial adviser, and this is not financial advice. The posts on this website are for informational purposes only; please consult a qualified adviser for personalized advice.

Check out other recent articles

About the author:

Written by David, a former academic scientist with a PhD and over a decade of experience in data analysis, modeling, and market-based financial systems, including work related to carbon markets. I apply a research-driven, evidence-based approach to personal finance and FIRE, focusing on long-term investing, retirement planning, and financial decision-making under uncertainty.

This site documents my own journey toward financial independence, with related topics like work, health, and philosophy explored through a financial independence lens, as they influence saving, investing, and retirement planning decisions.

Frequently Asked Questions (FAQs)

-

The macro case is real—ageing populations create fiscal pressure and sectoral labor shortages. But the argument breaks down at the micro level: age discrimination is well-documented, re-entry barriers are rising, and the modern hiring process is a significant undertaking even for younger candidates. Encouraging participation works far better with real incentives—flexible arrangements, wage premiums—than appeals to civic duty.

-

Yes—and earlier than most expect. Resume audit studies across the US, UK, and OECD consistently show callback rates declining for applicants in their mid-40s and falling further into their 50s and 60s. One well-cited NBER study found older applicants needed significantly more applications to receive the same callbacks as younger candidates with equivalent qualifications. Bias typically surfaces through coded language—"energy," "cultural fit," "long-term potential"—rather than explicit exclusion.

-

OECD data consistently shows longer unemployment durations and lower re-employment rates for workers over 50 who exit the labor market. The barriers are multilayered: skills currency, employer perception, salary expectations, and hiring bias all interact. Highly specialized experts can remain attractive into their 60s, but they represent a small fraction of the overall market.

-

AI is compressing skill half-lives and increasing employer selectivity—both of which amplify existing age hiring biases. As productivity tools expand effective labor supply, employers can afford to be pickier, and older workers re-entering after a gap face steeper hurdles. The dynamic tends to widen, not close, the age gap in hiring outcomes.

-

The skill half-life is how quickly professional knowledge becomes obsolete—estimated at around five years in fast-moving fields, and likely shortening further with AI deployment. For FI planning, this means assuming continuous employment until 65 is increasingly risky. If your skills erode faster than they can be updated, the window of peak employability may close well before official retirement age.

-

People respond to incentives, not moral pressure. Higher wages for scarce skills, genuinely flexible arrangements, and reduced tax friction on additional income would move labor supply far more effectively than public scolding. In the UK specifically, pension and tax interactions can make part-time re-engagement financially penalizing—a structural problem that rhetoric doesn't solve.

-

Achieving early retirement typically requires decades of high savings, disciplined investing, and careful planning—behaviors that generate capital formation and tax revenue during earning years. Whether reduced labor participation creates a net economic cost depends heavily on sector-specific shortages and whether automation is already reducing demand in affected areas. The "free-rider" framing oversimplifies a more complex picture.

-

The prudent approach treats continuous employment until traditional retirement age as an optimistic scenario, not a baseline. Age discrimination, AI-driven skill obsolescence, and sector restructuring make mid-career disruption a real probability for many professionals. Achieving financial independence early shifts the risk: continued employment becomes an option rather than a necessity, preserving agency exactly when re-entry is hardest.

-

If age discrimination begins in the mid-40s and skill cycles are shortening, planning to work until 65 may be a significant financial planning error. The FIRE (Financial Independence, Retire Early) insight—that the cost of over-saving is modest relative to under-saving—becomes especially compelling when you factor in labor market fragility as a real retirement risk. Building optionality early is insurance against a labor market that may not want you back on your timeline.

-

The headline argument is similar in both countries, but the specifics differ. The UK faces post-Brexit labor rebalancing, relatively high youth unemployment, and shortages concentrated in healthcare, logistics, and skilled trades—gaps that general retirees can't easily fill. In both markets, abstract calls for older workers to return often paper over skills mismatches and employer preferences that limit actual absorption.

Join readers from more than 100 countries, subscribe below!

Didn't Find What You Were After? Try Searching Here For Other Topics Or Articles:

<script>

ezstandalone.cmd.push(function() {

ezstandalone.showAds(102,109,110,111,112,113,114,115,119,120,122,124,125,126,103);

});

</script>