Why Your FI Number Is Wrong (and Why That’s OK)

Calculating your Financial Independence (FI) number looks straightforward at first glance. The reality, though, is that it’s only a rough approximation—the FI number you calculated is almost certainly wrong. Photo by Vitaly Gariev on Unsplash.

Reading time: 7 minutes

Quick takeaway: If you’re wondering whether your Financial Independence (FI) number is “right,” the answer is probably no. And yet that’s perfectly normal. This article explains why FI numbers are inherently difficult to estimate, what actually matters instead, and how to stop letting uncertainty create anxiety or paralysis. You’ll learn how flexibility, income optionality, and thinking in ranges—not point estimates—lead to more resilient Financial Independence journeys and outcomes.

What you’ll get

✔ Why FI numbers are inherently unstable

✔ How flexibility beats conservative math

✔ Why expenses and identity evolve

✔ How to think in FI ranges

✔ How to reduce anxiety and paralysis

TL;DR — Your FI Number

📊 FI numbers are estimates, not truths

🔁 Life, markets, and rules change

🧠 Flexibility beats perfect math

💼 Optional income lowers risk

📈 Savings rate—paired with flexibility—is your compass

If you’re looking for a quick answer: your FI number will change, and that’s OK. The rest of this article explains why—and how to plan anyway.

Why Your FI Number Is Probably Wrong (And Why That’s Actually Fine)

The illusion of precision—and a calmer way to think about financial independence planning

The moment you reach Financial Independence (FI)—and surpass the crossover point of FI—often feels like a source of clarity. People often tell themselves that once they reach that figure, they’ll be “safe”. At that point, perhaps, they will be able to stop worrying about money entirely and fully focus their attention elsewhere.

Unfortunately, for many people in the FI space, the reality can become the opposite: their FI number can become a moving target that ends up fueling anxiety and endless spreadsheet tweaking and optimizing.

In this article, we’ll explain why your FI number is almost certainly wrong. Your FI number is likely not incorrect because of a math mistake, but because the future is more uncertain than we’d like to admit. Instead, we should embrace how flexibility, potential identity shifts, and imperfect math could actually make your financial journey not only more enjoyable but more resilient.

Later in the article, I’ll also show how to use FI calculations more realistically—and how a simple tool can help you explore ranges instead of chasing a single number.

Some people in the FIRE space overoptimize their finances from a place of fear and a mindset of scarcity. Instead, we should embrace uncertainty and acknowledge that having a good-enough ballpark FI number is sufficient. Photo by Zendure Power Station on Unsplash.

The False Precision Problem: Why FI Math Feels Exact but Isn’t

The classic FI formula of multiplying annual expenses by 25 is seductive because it feels clean and objective. After all, it’s rooted in the 4% rule of thumb, which was designed around historical market data. In practice, the 4% rule is a safe withdrawal rate (SWR): the idea that you can withdraw about 4% of your portfolio’s value each year—adjusted for inflation—without running out of money over a 30-year timeframe.

It’s a useful starting point, but it was never meant to be a precise prediction—especially for early retirees with much longer time horizons of 40-60 years.

Small changes in assumptions, like inflation, real returns, taxes, fees, or withdrawal timing, can compound against you over long periods of time. In the end, a number that looks precise is built on layers of uncertainty in the underlying assumptions. The danger here is treating this guideline as a rigid rule.

In practice, I personally think early retirees can follow the 4% rule, or even a higher safe withdrawal rate (SWR), provided they have flexibility built in their spending (e.g., spending rules and guardrails). But for those implementing the SWR religiously—without adjusting withdrawal spending to market reality—they can get into problems quickly.

Sequence of returns risk (SORR) makes the early years disproportionately important. Even if long-term averages look reasonable, the order in which they occur matters enormously—especially for early retirees. A poor sequence of returns in the first decade of retirement can permanently affect a portfolio, especially when using higher SWRs.

Many FIRE folks respond to SORR by reducing dramatically their SWR, hoping to eliminate risk entirely. They also tend to model worst-case spending, pessimistic return forecasts, and, by doing so, end up extending their career substantially just to feel safe. While this looks prudent on paper, it often amplifies insecurity. The underlying issue isn’t whether your SWR should be 3%, 3.5%, or 4.7%, but the belief that any single withdrawal rule can protect you from uncertainty.

Some readers may prefer ultra-conservative assumptions and SWRs for peace of mind—and that’s fine in many cases. The key distinction is to reflect on whether that conservatism reduces anxiety or fuels it.

Your FI number is wrong because you’ll end up changing more than you expect. Photo by Ilya Pavlov on Unsplash.

Your Expenses Will Change—Because You Will Change Over Time

A second reason has less to do with math and more to do with how you change over time. When we estimate future expenses in our 20s or 30s, we often project forward a very limited version of ourselves. We ignore the well-documented “end-of-history illusion” and assume that today’s preferences, habits, and values will persist indefinitely in the future.

In reality, everything will change: relationships, children, health considerations, aging parents, shifting energy levels, desired levels of comfort or convenience, and much more. What once felt like a luxury may later feel like a basic comfort. Early on in my own FI journey, I targeted monthly expenses that now feel comically low. I don’t think I’ve failed at being disciplined—I still feel like we’re implementing healthy savings rates—but simply life has evolved in many dimensions.

Sometimes lifestyle inflation isn’t a mistake, but the result of a deliberate decision. Part of the FI community often frames rising expenses as some sort of moral failing or lack of optimization. But many increases in spending reflect conscious tradeoffs: paying for convenience to gain more free time with your kids while they’re young, prioritizing investing in health, reducing friction to make life easier for your kids, or choosing experiences over austerity.

These changes can occur naturally over time and in many cases—especially if the tradeoffs are made consciously, not automatically—can signal that money is serving life, not the other way around. Our own spending habits have evolved over the course of our FI journey; early on, we buckled down and implemented a very high savings rate for many years. After 7 years on the journey, though, I’ve come to realize that the marginal impact of frugality has started to decrease.

Put simply, at a certain point the returns from your portfolio start having an outsized effect in comparison to any extra savings you manage to invest from being overly frugal. We covered the 0.01% spending rule in a recent post, which can help to gauge what amounts of spending are simply not worth the extra thought.

For some major expenses, it’s difficult to anticipate how much they may change over time. Consider, for instance, medical costs, family obligations, or housing needs. While these realities might be predictable in direction, they’re very difficult to estimate in magnitude.

Either way, in practice it means that the FI number evolves over time—and that your original FI number estimate was always going to be wrong. A static FI number simply can’t keep up with shifting values, changing priorities, and the way real life unfolds over time.

Your FI Number Might Be Too High, Not Too Low

As mentioned, many FI plans assume zero flexibility—which is not only unrealistic, but often extends our working careers more than necessary. A common mistake is building a FI number around the assumption that spending must remain fixed, regardless of market conditions or evolving life circumstances.

In reality, most people are more flexible than they give themselves credit for. Discretionary spending can be delayed, downscaled, or reshaped. Perhaps you budgeted for vehicle expenses, but you can be flexible with the timing of the purchase: if markets are down 30%, most retirees can wait until markets recover before withdrawing large, one-time expenses. Even modest flexibility can dramatically improve portfolio longevity. Unfortunately, this ability is rarely reflected in headline FI calculations.

Retirement spending often declines over time. Research on retirement behavior shows that spending frequently follows a “smile” pattern: higher in early retirement, lower in middle years, and rising later (in some countries) due to health care costs.

And yet, many FIRE folks are modeling their FI number based on their current lifestyle, ignoring that in later decades they will prefer to travel less, spend more time with family, and likely be more home-bound. Planning as if our peak spending persists forever can significantly inflate your required nest egg, and is another reason your FI number may be wrong.

This matters especially for late starters, who are often closer to pension age and can therefore target a meaningfully lower number—see FIRE for late starters for the full breakdown.

In this blog we’ve covered from multiple angles the optionality provided by geographic and lifestyle arbitrage. The ability to live in different places—temporarily or permanently—introduces flexibility that many FI models ignore. Whether it’s spending time in lower-cost regions, downsizing housing as you age, or adapting travel styles, these options don’t necessarily require sacrifices in quality of life. For many they actually increase it.

A flexible mindset requires openness and an ability to be OK with some uncertainty. We don’t have a magic ball to predict the future, but we do have more flexibility cards up our sleeve than we think.

Flexibility is an under-appreciated tool on your path to FI. In early retirement, you are much more adaptable than you think. Photo by Mesut Kaya on Unsplash.

FI Is Rarely Binary: Work, Income, and Purpose Often Continue

Many FI folks discover they don’t actually want to stop working entirely in their 30s or 40s. As some FIRE folks progress through their journey they realize that despite not being FI yet, they are already reaping many of its benefits today. Personally, being already 7 years into the journey has allowed me to completely rethink what I want my career and timeline to FI to look like.

Being on the journey to FI helped me step away from an unhealthy career trajectory. And now that I’m working on something I actually enjoy, the urgency of reaching FI as fast as possible has gone down. Early retirees that discover meaningful, creative, or self-directed work may still want to work despite their FI status.

In this case, optional work changes everything. It not only reduces pressure to sprint to a very large FI number, but also reframes FI as enhancing freedom rather than optimizing for escape from a career path you don’t enjoy.

Even small amounts of income have an outsized impact. Earning a modest amount post-FI—either part-time consulting, freelancing, seasonal work, passion projects—can dramatically lower the withdrawal burden on a portfolio. This happens naturally to many on the FI journey; although it doesn’t show up in early-stage spreadsheets or underlying assumptions, it becomes obvious in real life. FI numbers calculated under the assumption of zero income forever are frequently too pessimistic.

The World Will Change in Ways No FI Model Can Predict

The world will change in ways you can’t model and that long-term forecasts may not materialize under political and policy changes. Markets don’t exist in a vacuum, but respond to changing economic environments. Tax regimes and healthcare systems can dramatically change over time, and social safety nets can expand or contract.

These forces affect both returns and expenses, yet are nearly impossible to forecast decades in advance. Treating today’s rules as permanent is one of the quiet assumptions we bake into our FI number estimates. But deep down we know that this is a big simplification.

Consider as well how technological shifts—including AI—are reshaping how value is created. It’s likely to change how work is compensated and what skills remain in demand. This transition will likely create and destroy opportunities, reduce costs, and destabilize existing models in ways we don’t anticipate. Saving too much—or too little—are both plausible outcomes.. This is another reason why flexibility and the right mindset matter more than precision.

FI planning tends to treat the future as risky but knowable, when in reality much of it is simply unknowable. But I don’t think the goal should be to eliminate uncertainty—which is not possible—but to build a life that can respond to it without panic. In the end, risk can be measured, but uncertainty must be lived with.

Taken together, these uncertainties point to a deeper issue—not faulty math, but the way we frame Financial Independence itself.

AI alone is likely to change our world in ways we don’t yet envision. You can fight the uncertainty and live in a perpetual state of anxiety or embrace the uncertainty as an integral part of life. Photo by Adi Goldstein on Unsplash.

From a Number to a Mindset: Why Being “Wrong” Is the Point

All of this leads us to an uncomfortable but liberating conclusion: your FI number was never meant to be exact. If you compared the FI numbers people projected early in their journey with the numbers they actually reached when they pulled the plug, the vast majority would look very different. And yet, many of those people still succeeded not because they predicted the future correctly, but because they build in flexibility, optionality, and adjusted their assumptions and expectations along the way.

This is where reframing FI as an identity shift rather than a destination can become powerful. Financial Independence is less about hitting a very precise net worth figure and more about moving from a state of dependence to one of optionality. From needing income at all costs to having the ability to say no and do what you’d prefer instead. It goes from optimizing every decision to trusting your ability to adjust as reality unfolds.

One practical way to internalize some of this is to stop thinking in static point estimates and start thinking in dynamic ranges and checkpoints. At the lower end of the range is a lean FIRE number: a version of independence that covers essentials and assumes a very high degree of flexibility. At the upper end is a more “fluffed-up” FI number, with extra margin for comfort, convenience, and uncertainty.

Somewhere in between likely lies the lifestyle you’d be perfectly happy with most of the time. But reaching the bottom of this range will already be enough to make you feel free. The mistake I think is assuming that only the top number counts.

For many, the real source of anxiety isn’t that FI projections are imperfect, but the belief that imperfection means inaction. But you don’t really need perfect forecasts to move forward. You may not control future returns, tax policy, or income with precision, but you do have agency over your savings rate, your spending awareness, and your willingness to adapt. Let those be your compass and adjust as needed. Accept the math will always be a little wrong.

If you’ve figured out how to save consistently and think intentionally about money, then you’ve done the hardest part. The same skills that got you close to FI will allow you to navigate uncertainty successfully—even if the future looks nothing like we expected.

Should You Still Calculate Your FI Number? Yes—but Use It Correctly

If you’ve made it this far, a natural question to ask yourself might be: does this mean I shouldn’t pursue Financial Independence or even bother to calculate an FI number? Not at all. Calculating a FI number is still very useful—it gives us a rough orientation, helps to clarify tradeoffs, and makes progress feel more tangible. Used well, it’s a compass: a way to stress-test assumptions, compare scenarios, and update your plan over time.

The key, I think, is understanding that it’s a large, imperfect ballpark estimate, not a promise or a finish line.

Instead, think of your FI number in ranges, by using a combination of different expenses in retirement, stock market outcomes, and safe withdrawal rates (SWR). Somewhere in between lies the scenario you’d be content with, but be ready to adjust over time as reality unfolds. There are many variables that simply aren’t under your control.

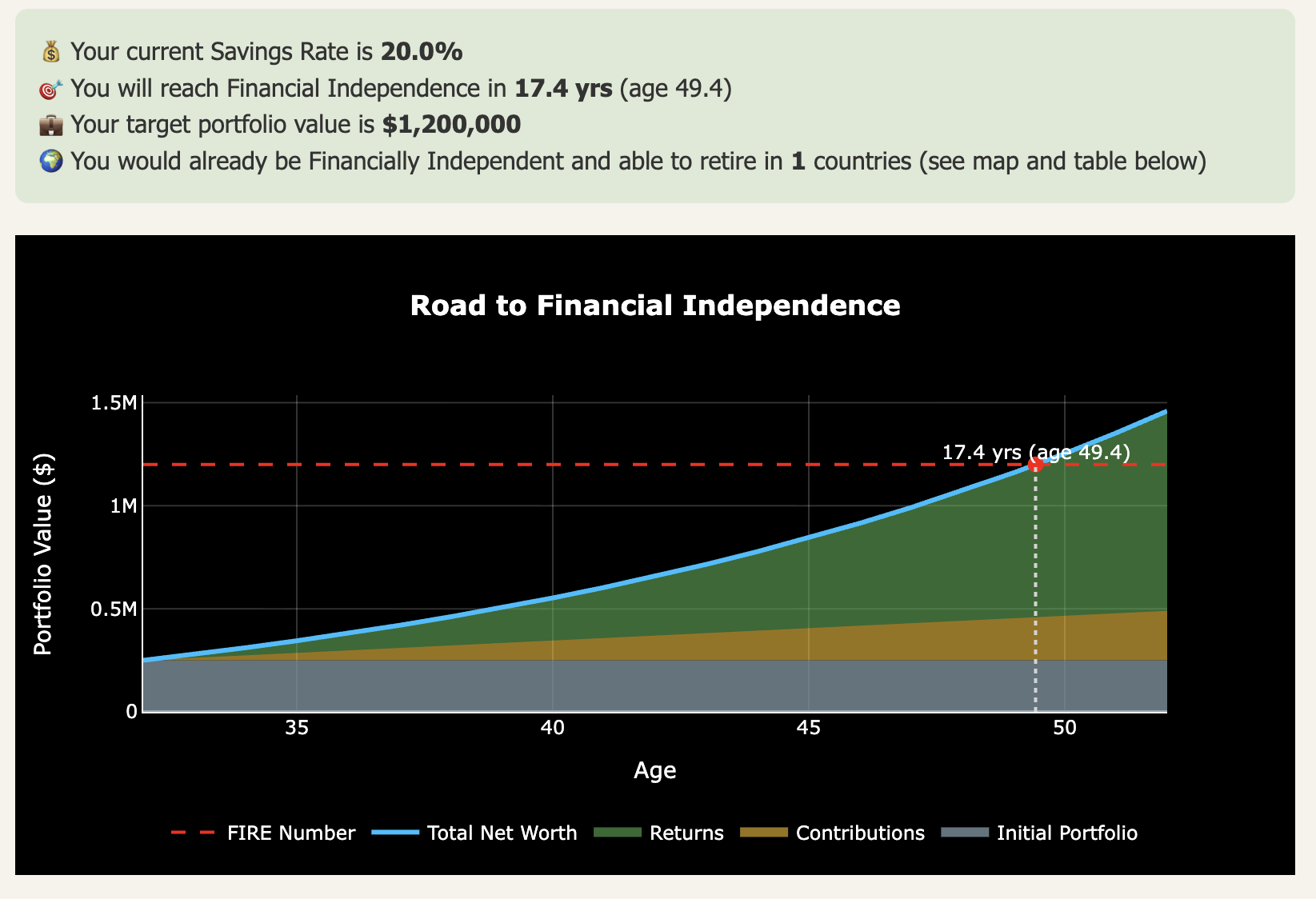

In Figure 1 below we present a screenshot of our FI Calculator, which is free for email subscribers. You can plug in your numbers and calculate how soon you could go into early retirement.

Figure 1: Screenshot of our FI Calculator—free for email subscribers. Enter your household annual salary, expenses, and current portfolio to calculate your timeline to early retirement. Play around with assumptions—expenses in retirement, stock market returns, and SWR—to build your FI number range.

💬 Which part of your FI plan feels the most “fragile” right now—expenses, market returns, or future income? What flexibility could you realistically build in to strengthen your plan?

👉 Want to understand how to reach Financial Independence in your mid-40s? Check out what savings rate will get you there depending on age and current portfolio size.

🌿 Thanks for reading The Good Life Journey. I share weekly insights on personal finance, financial independence (FIRE), and long-term investing — with work, health, and philosophy explored through the FI lens. If this resonates, join readers from over 100 countries and subscribe to access the free FI tools and newsletter.

Disclaimer: I’m not a financial adviser, and this is not financial advice. The posts on this website are for informational purposes only; please consult a qualified adviser for personalized advice.

About the author:

Written by David, a former academic scientist with a PhD and over a decade of experience in data analysis, modeling, and market-based financial systems, including work related to carbon markets. I apply a research-driven, evidence-based approach to personal finance and FIRE, focusing on long-term investing, retirement planning, and financial decision-making under uncertainty.

This site documents my own journey toward financial independence, with related topics like work, health, and philosophy explored through a financial independence lens, as they influence saving, investing, and retirement planning decisions.

Check out other recent articles

Frequently Asked Questions (FAQs)

-

Most likely, yes—but not because you made a mistake. FI numbers rely on assumptions about markets, spending, and life that will change over time. Being “wrong” is normal and expected.

-

Because your life, values, and expectations are evolving. Expenses, risk tolerance, and desired comfort change over time, making static FI targets unstable.

-

Yes. Many people assume zero flexibility, zero income, and peak spending forever. In reality, most retirees adapt, spend less over time, or earn some income.

-

Often, yes. Research shows a “retirement spending smile,” with higher spending early, lower spending mid-retirement, and rising healthcare costs later.

-

Flexibility, optional income, and savings rate matter more than precision. These allow you to adapt when assumptions break.

-

Many people choose to. Optional work can reduce portfolio stress, provide purpose, and increase resilience without undermining independence.

-

Think in ranges: lean FI, baseline FI, and “fluffed-up” FI. Any point in the range may already provide freedom.

-

That risk can’t be eliminated, but it can be managed through spending flexibility, income optionality, and geographic or lifestyle arbitrage.

-

Shift focus from perfect forecasts to controllables: savings rate, adaptability, and building optionality over time.

Join readers from more than 100 countries, subscribe below!

Didn't Find What You Were After? Try Searching Here For Other Topics Or Articles:

<script>

ezstandalone.cmd.push(function() {

ezstandalone.showAds(102,109,110,111,112,113,114,115,119,120,122,124,125,126,103);

});

</script>