The Hidden Risk of Geoarbitrage: When Your Cheap Country Stops Being Cheap

Southeast Asia and Latin America offers some of the most compelling geoarbitrage opportunities for early retirees— from Thailand and Indonesia to Costa Rica and Mexico. See our guides to the best retirement destinations in Latin America and Asia. Photo by Stiven Rivera on Pexels.

Reading time: 7 minutes

Quick answer:

While geoarbitrage can dramatically shorten your timeline to Financial Independence and early retirement (FIRE), most plans assume today's cost advantage will persist indefinitely. In practice, two separate risks can erode it over time: local price inflation in your destination country, and exchange rate movements between your portfolio currency and your spending currency. Both can operate independently, and both can compound with sequence-of-returns risk if they hit in the early years of retirement. The right response is not to avoid geoarbitrage, but to stress-test your destination the same way you stress-test your portfolio.

What you'll get from this article:

✔ Why the 4% rule and standard withdrawal research doesn't account for geoarbitrage risks

✔ Case studies of destinations that already lost their cost advantage and the reasons behind

✔ Real data on what happened to US retirees in Thailand in 2024-2025

✔ Two practical responses: buffer vs flexibility—and their trade-offs

✔ A framework for choosing destinations with more durable cost advantages

TL;DR — The Geoarbitrage COL Risk 🌍📉

🏖️ Geoarbitrage works—but most plans treat today's COL advantage as permanent. It isn't

💱 Two separate risks to consider: local price inflation (things cost more in local currency) + exchange rate moves (your currency buys less)

🇹🇭 Real example: Although Thai inflation was near-zero in 2024-25, the Baht strengthened 15-18% vs USD, making Thailand meaningfully more expensive for US retirees

🇵🇹 Portugal: Lisbon apartment prices tripled between 2015-2025, driven by multiple demand-side pressures and supply constraints

📊 If local costs rise 6% per year and hit you in year 1-2 of retirement, it compounds directly with sequence-of-returns risk (SORR)

🛡️ Two responses: build a larger buffer (costs working years) or build genuine location flexibility

🔁 Treat geoarbitrage as a living strategy—not a one-time destination decision

🧮 If returning home is possible, target a very conservative withdrawal rate—remember that a portfolio built for Thailand can't fund a US retirement

What Happens When Your Cheap Country Gets Expensive?

Geographic arbitrage in retirement is one of the most powerful levers available to shorten your timeline to FIRE (Financial Independence, Retire Early). The concept is very simple: retire to a country where your money goes significantly further and you can aim for a substantially smaller nest egg and a much shorter working career.

If you envisioned needing $1.5M for retirement in the US to support your desired lifestyle, you may only need to accumulate around $750,000 to sustain a comparable—sometimes higher—quality of life in Thailand or Indonesia. Although it depends on many factors—like savings rate or current portfolio value, it’s not unusual that this decision can shorten FIRE timelines by 5-10+ years.

Personally, I think about geoarbitrage often—I'm currently based in Germany, seven years into my own FI journey, and unlikely to stay here full-time in retirement. The plan I keep returning to is a version of what I've written about in our seasonal geoarbitrage guide: splitting the year between Germany and southern Europe—a pattern sometimes called snowbirding, well-established among retirees long before the FIRE community “discovered” it. In our case, it could mean staying close to family in spring and summer, escaping the cold in autumn and winter.

While the maths underpinning geoarbitrage appear straightforward at first, it’s usually built on a static view of the retirement destination: we assume that today’s cost of living (COL) will remain constant or have a moderate inflation rise.

But what happens if the country you retired to stops being as cheap as when you planned your early retirement? This article covers this specific risk, what pushes up costs in popular expat destinations, how to consider them in relation to the sustainability of your withdrawals, and how to build a geoarbitrage plan resilient enough to survive any scenario.

One of the key insights of this article is that we shouldn’t just stress-test our portfolio against bad market sequences (i.e., sequence-of-returns risk), but we should stress test the potentially changing conditions of our retirement destination too.

Porto is one of Europe's most beautiful cities, and Portugal in general topped our best destinations for retirement in Europe. However, it’s also one of the clearest examples of a geoarbitrage destination whose cost advantage has narrowed significantly over the past decade. Photo by Nick Karvounis on Unsplash.

The 4% Rule Was Built for One Country. Geoarbitrage Adds a New Risk Layer

The 4% rule of thumb and its variants (e.g., 4.7%) were designed and backtested against very specific conditions—US market returns and US inflation. However, when you decide to pull the geoarbitrage card to retire abroad, you introduce two new variables (and risks) that withdrawal research didn’t account for: local cost inflation in your destination country and exchange rate movements between your portfolio currency and your spending currency.

Most geographic planning tools model today's cost advantage and assume it will persist. Having a sense of differences in cost of living across countries to inform the decision is certainly a very useful—and necessary—starting point (see Figure 1 below and its associated tool).

Figure 1: Timelines to FIRE (Financial Independence, Retire Early). Screenshot of our Financial Independence Calculator (free, email unlock). Enter your data on income, savings, and existing portfolio, and explore how your timeline to FI changes depending on where you choose to retire.

Using our FI and Geoarbitrage Calculator, a retiree envisioning needing around $5,000 per month in the US may find they could fund a comparable (or better) lifestyle in Thailand with 44% of that—$2,200. Applying a 4% withdrawal rate, that would mean needing to accumulate a $660,000 portfolio instead of $1.5M. This can be a life-changing realization for many, because it can shorten working careers by years, sometimes a decade.

But here come the caveats. This estimation treats the $2,200 figure as stable in real terms and denominated in USD. In practice, though, that figure will be subject to local price inflation in Thai Baht, and to exchange rate movements between the Baht and the USD. If Thai prices rise 4% annually in Baht and the Baht appreciates 2% against the USD simultaneously—both plausible in a growing economy—your effective cost in USD could rise by about 6% per year.

In practice, most early retirees hold a mix of stocks and bonds, so a 5% real return is a more realistic planning assumption than the 7% you'd expect from 100% equities. Against that backdrop, a 6% annual rise in effective costs starts to look very uncomfortable—and if it hits in the first years of retirement, it compounds directly with sequence-of-return risk (SORR).

The two factors—local inflation and exchange rates—are conceptually separate risks, even though they can move together in some situations. Local price inflation means the things you buy in Thailand cost more Baht each year. Exchange rate appreciation means that same Baht costs more of your USD or EUR each year.

To make this concrete, let’s consider what actually happened to a US retiree living in Thailand over the past two years: Thai consumer price inflation averaged just 0.4% in 2024 and was even slightly negative in 2025. By this measure alone, the US early retiree would not have much to worry about. Indeed, as observed in Figure 2, the consumer price index has been lower compared to the US for the last decade or so.

Figure 2: Thai consumer price inflation has run consistently below US levels for the past 15 year—and turned slightly negative in 2025 (not shown in graph). Local prices alone were not the problem for US retirees in Thailand. Source: IMF / World Bank

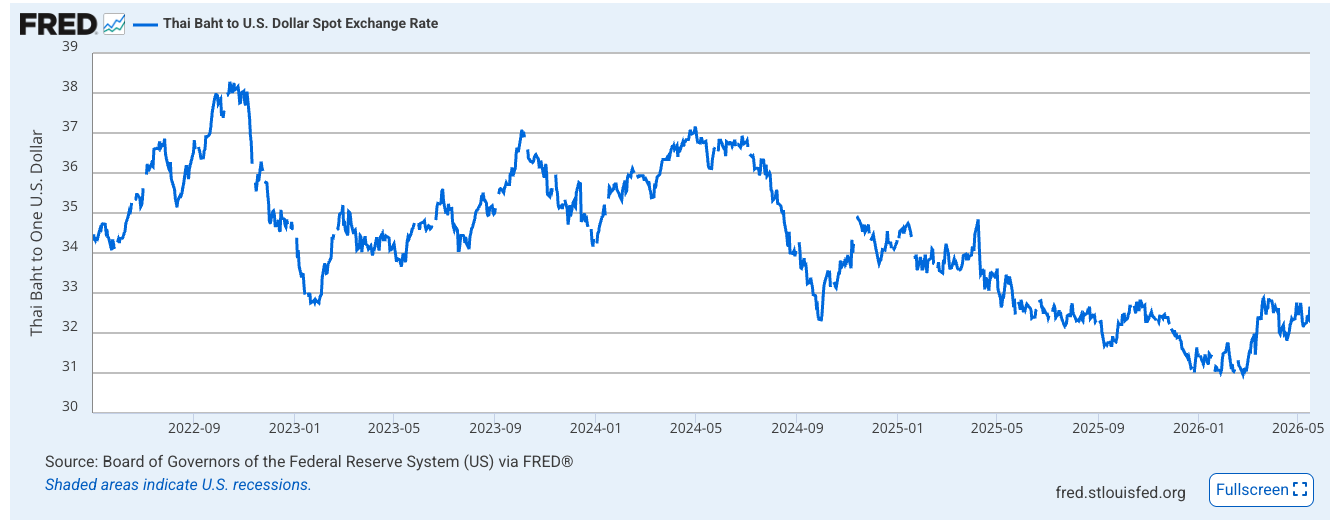

But the exchange rate told a very different story. The Thai Baht strengthened from around 37-38 Baht per USD in mid-2022 (Figure 3) back down to approximately 31-32 Baht per USD by early 2026—a shift of roughly 15-18% (Figure X). A US retiree who had budgeted $2,200/month when the rate stood at 37 would now need closer to $2,600 to fund the same desired lifestyle. That’s a large cost increase driven entirely by the currency channel, and may negatively impact an early retiree’s withdrawal plan.

Figure 3: The Thai Baht strengthened from around 38 Baht per USD in mid-2022 to approximately 32 by early 2026—a 15-18% shift that made Thailand meaningfully more expensive for US dollar holders. Source: FRED, Federal Reserve.

Exchange rate volatility of this magnitude—a 15-18% shift over three years—is not unusual for emerging market currencies. Movements of 10-20% over multi-year periods are common across Southeast Asia, Eastern Europe, and Latin America, driven by shifts in monetary policy, trade balances, and capital flows.

Stock markets were fortunately on an upwards trajectory during this period. But had there been a simultaneous market downturn, the combination would have been very damaging: higher-than-expected withdrawals driven by currency changes and a portfolio diminishing by falling markets. This is the classic SORR that early retirees are wary of, but with an added “inconvenience” that’s usually not considered.

This example is instructive because it involves one of the most popular geoarbitrage destinations—a place many FIRE investors feel confident in their numbers. The lesson here is not to avoid geoarbitrage, but to plan geoarbitrage abroad considering these two channels of risk explicitly, not just the difference in cost of living.

The Thailand example is a recent data point—but we can find many other destinations that have experienced rapid changes in cost of living over the last few years.

Note: While currency-hedged ETFs could theoretically address exchange rate risk on your portfolio returns, they don't protect your actual spending power abroad. Moreover, switching from an unhedged to a hedged ETF does not only increase fees but typically triggers a taxable event. Currency forwards and options exist but require derivatives access, active management, and are expensive for emerging market currencies due to interest rate differentials. For most FIRE retirees already holding a global index fund, hedging is an impractical and costly partial solution. Flexibility and buffer remain the more realistic responses.

Destinations That Got Expensive — and What Drove the Change

Several well-known retirement destinations have already experienced meaningful erosion of their cost advantages. Understanding what drove those increases helps identify the forces likely to affect other destinations in the future.

Portugal is one of the clearest European examples. Between 2015 and 2024, house prices more than doubled, driven by multiple factors: sustained foreign investment (e.g., via the Golden Visa program and the Non-Habitual Resident tax regime), tourism growth, a surge in short-term rentals converting long-term housing stock, and domestic economic recovery. All these demand-side dynamics met a supply market that hadn't built meaningful new housing in years. In Lisbon and Porto specifically, prices rose well above the national average—with some municipalities seeing increases of over 100% between 2018 and 2024 alone.

What does this mean for would-be expat retirees? Firstly, that while areas outside of larger cities like Lisbon and Porto remain more affordable, some of these attractive destination cities may no longer provide the huge geoarbitrage impact they once did—the math in 2026 will look very different than it did in 2015. Secondly, there is a perception that locals are being driven out of their cities by foreign expats. Although the reality is more nuanced, and the supply aspect is also important, it's worth knowing that in some areas, the welcome for foreign expats has cooled.

Chiang Mai tells a slower but similar story. A decade ago it was one of the digital nomad hubs, cited for $800-1,000 per month expenses for a single person. By 2026, though, a single person living comfortably in Chiang Mai—with a private apartment, regular meals out, and basic transport—now runs more like $1,800–$2,500/month.

This increase has been gradual and its drivers are somewhat different from Portugal: rising Thai incomes and domestic economic development have pushed up prices across the whole economy, while growing expat and digital nomad demand in specific neighbourhoods has added another layer of pressure. While Thailand remains significantly cheaper than Western countries, the margin continues to narrow.

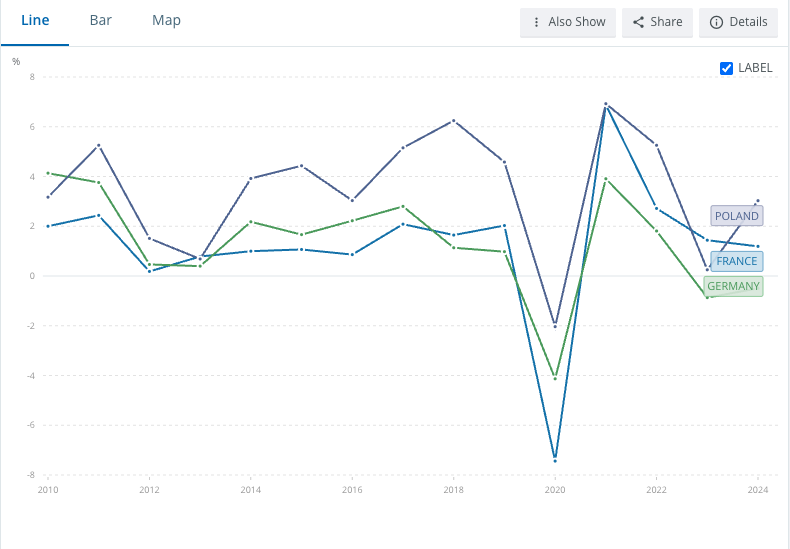

Other examples can be found in Eastern Europe. Countries like Poland—one of the fastest growing economies of Europe (Figure 4)—Czech Republic, and the Baltic states were considered very affordable for much of the 2010s. But main cities like Warsaw or Prague have seen real estate prices rise sharply toward Western European levels, driven by EU economic integration, rising local wages, and foreign investment.

Figure 4: Poland has been one of the fastest-growing economies in Europe over the past decade—a success story for its population, but also a reminder that fast economic development tends to narrow the cost advantage that initially attracts expat retirees. Source: World Bank

The common thread across these destinations is fairly predictable: fast economic development, growing foreign demand, and housing supply that can't keep up. For a FIRE investor planning a retirement abroad, the takeaway is that no destination can be assumed to keep its cost profile indefinitely. The question is not whether your chosen country will change, but whether your portfolio will accommodate those changes or not.

Buffer or Flexibility: The Two Ways to Protect Your Geoarbitrage Plan

There are two ways to protect your plan, and they involve a genuine trade-off.

The first one would be to build a larger buffer—retire with a lower withdrawal rate. In other words, target a larger portfolio than the destination would at first suggest as reasonable. In our previous example, if we needed to fund $2,200 per month in Thailand, instead of targeting a $660,000 portfolio, maybe it would make sense to target $750,000 instead (corresponding roughly a 3.5% withdrawal rate).

This is the simpler and more conservative approach, but it comes at a real cost: a lower withdrawal rate means a larger required portfolio, which means working and saving for more years. If building that extra buffer requires two or three years more of accumulation, you need to decide whether that higher peace of mind is worth the time. For expat early retirees who genuinely cannot or will not relocate once settled abroad, a large-enough buffer is probably the safer path.

The second approach is genuine location flexibility—treating geoarbitrage not as “I'll retire to Thailand” but as “I’ll always live somewhere with a cost that keeps my withdrawal rate sustainable.” In this case, if Thailand’s cost advantage narrows to the point that you’re withdrawing more from your portfolio than you should, then you consider moving again—to Vietnam, Malaysia, or whatever country continues to provide a good lifestyle and a reasonable cost in the future.

The advantage of this approach is that it costs nothing in extra working years, but it does require genuine willingness to move, which is not everyone's reality. Family proximity, language, children's schooling, and leaving established social networks are all important factors at play.

Another risk worth highlighting regardless of the approach: if you design your portfolio for a low-COL destination, returning to your home country can become structurally difficult—and not only if costs rise in the retirement destination, but even if they don’t. A $660K portfolio built for Thailand was never intended to fund a US or European retirement.

If returning home is a realistic possibility—for family, health, or other personal reasons—this should influence your target portfolio size from the start. An even lower withdrawal rate of around 3% could your portfolio room to grow over time, preserving the option to relocate to a higher-COL destination later if needed.

Cyprus made our top 5 retirement destinations in Europe—also popular for its tax advantages, climate, and English-speaking infrastructure. Like all attractive destinations, it’s worth monitoring its cost trajectory. Photo by Katerina Bot on Unsplash.

A Framework for Choosing Destinations That Last

Not all geoarbitrage destinations carry the same risk of cost increase, and some practical indicators can help us distinguish more durable from more fragile ones.

First, we can consider where a given destination sits in its “expat discovery cycle.” Countries that appear regularly in digital nomad guides and in FIRE-related media are more likely to be late in the discovery cycle—demand pressure is likely already building. In contrast, countries requiring more active research are more likely to be earlier in the cycle, potentially offering more long-term attractive costs.

Another indicator could be housing supply flexibility. What constraints do countries or cities face in relation to new construction—for example, heavy planning bureaucracy, coastal restrictions, or historical centres? A third indicator could be to consider the recent economic development trajectory: a country growing at 5-6% GDP annually for a decade is likely to see meaningful cost convergence with richer countries over a long retirement horizon.

In the end, though, none of these indicators will offer complete certainty—and that’s also a key takeaway from this article. A destination that scores very well on retirement suitability variables today can still surprise you 10 years from now.

The better response is not to find the perfect destination and commit permanently, but to treat geoarbitrage as something you revisit rather than a decision you make once. Build a plan that works under adverse scenarios, maintain genuine flexibility, and size your portfolio with the possibility of change in mind.

If you enjoyed this guide, here are some next steps:

👉 For the full geographic arbitrage framework—including country rankings—see our complete guide to geoarbitrage and FIRE

👉 Model your timeline to Financial Independence—and where you could retire sooner abroad—with our FI Calculator (email unlock)

👉 Want to understand how withdrawal rates interact with this strategy? See our complete guide to safe withdrawal rates

👉 Browse 130+ articles on FI, investing, work, and lifestyle at The Good Life Journey

👉 Subscribe for weekly insights—one-click unsubscribe

🌿 Thanks for reading The Good Life Journey. I share weekly insights on personal finance, financial independence (FIRE), and long-term investing — with work, health, and philosophy explored through the FI lens.

Disclaimer: I am not a financial adviser, and this content is for informational and educational purposes only. Please consult a qualified financial adviser for personalized advice tailored to your situation.

Check out other recent articles

About the author:

Written by David, a former academic scientist with a PhD and over a decade of experience in data analysis, modeling, and market-based financial systems, including work related to carbon markets. I apply a research-driven, evidence-based approach to personal finance and FIRE, focusing on long-term investing, retirement planning, and financial decision-making under uncertainty.

This site documents my own journey toward financial independence, with related topics like work, health, and philosophy explored through a financial independence lens, as they influence saving, investing, and retirement planning decisions.

Frequently Asked Questions (FAQs)

-

The 4% rule was designed and backtested against US market returns and US inflation — it doesn't account for the two additional risks of retiring abroad: local cost inflation in your destination country, and exchange rate movements between your portfolio currency and your spending currency. If local costs rise faster than your portfolio returns, or if the exchange rate moves against you, the plan can fail even if your portfolio performs as expected. For geoarbitrage retirees, a more conservative withdrawal rate — or ongoing location flexibility — provides a better safety margin than the standard 4% assumption.

-

If your destination's costs rise faster than your portfolio returns in real terms, your effective withdrawal rate increases even if you make no change to your spending in local currency. For example, if Thai prices rise 4% in Baht while the Baht appreciates 2% against the USD, your effective USD cost rises roughly 6% per year — more than most portfolios return in real terms. If this happens in the first few years of retirement, it compounds with sequence-of-returns risk, which can permanently impair portfolio longevity. The practical response is to stress-test your plan against destination-specific cost increases, not just historical market sequences.

-

Thailand remains significantly cheaper than most Western countries — a comfortable lifestyle in Chiang Mai still runs $1,800-2,500/month in 2026 compared to $5,000+ in many US cities. But the margin has narrowed from a decade ago, when $800-1,000/month was widely cited, and the Baht has strengthened meaningfully against the USD in recent years. For a US retiree, Thailand is still a powerful geoarbitrage destination — but the plan should account for continued cost convergence rather than assuming today's advantage is permanent.

-

Currency risk in retirement refers to the impact of exchange rate movements on your purchasing power when your portfolio is denominated in one currency but your expenses are in another. Even if local prices in your destination stay flat, a strengthening local currency makes those expenses more expensive in your portfolio currency. In 2025, for example, Thai consumer prices were essentially flat or slightly negative — but the Baht strengthened roughly 9% against the USD, effectively raising the cost of living in Thailand for US retirees by the same amount through the currency channel alone.

-

The most durable geoarbitrage destinations combine genuine current cost advantages with slower discovery curves — meaning they haven't yet been heavily promoted in mainstream FIRE and nomad media, giving more cost runway before demand pressure builds. Countries earlier in the discovery cycle across Southeast Asia, Central America, and parts of the Balkans offer more runway than established destinations like Lisbon, Chiang Mai, or Prague, which have already experienced meaningful cost convergence. The right destination also depends on healthcare access, visa stability, and personal lifestyle factors — cost alone is an incomplete criterion.

-

The appropriate buffer depends on how volatile you expect destination costs to be and whether you have the flexibility to relocate if needed. As a rough guide, if your destination numbers work at 4%, planning for 3-3.5% provides meaningful protection against both local cost increases and currency movements without dramatically extending your working career. If you're targeting a fast-growing destination with significant foreign demand — a late-discovery market — the case for a more conservative withdrawal rate is stronger. If you have genuine location flexibility and would relocate if costs rose significantly, the buffer requirement is lower.

-

Portugal's cost increases between 2015 and 2025 were driven by a combination of factors: the Golden Visa and Non-Habitual Resident tax programs attracting substantial foreign investment, tourism growth, short-term rental platforms converting housing stock, and domestic economic recovery — all meeting a housing supply market that hadn't built significantly since the 2008 crisis. Lisbon apartment prices rose roughly 209% in that decade. Portugal outside the major cities remains more affordable, and the country still offers a good quality of life — but the geoarbitrage maths in 2026 looks very different from 2015, particularly in Lisbon and Porto.

-

Yes, but you need to plan for it explicitly rather than assuming your portfolio can fund both scenarios. A portfolio sized for Thailand — perhaps $660K at 4% — was never designed to fund a US or European retirement. If returning home is a realistic possibility for family, health, or personal reasons, targeting a 3% withdrawal rate rather than 4%+ allows the portfolio to grow over time, preserving the option to relocate to a higher-cost country without the plan collapsing. Treating the move abroad as reversible requires building a portfolio that can survive the reversal.

-

Standard FIRE planning stress-tests your portfolio against bad market sequences — falling returns in the first years of retirement. Robust geoarbitrage planning adds a second stress test: what happens to your withdrawal sustainability if local costs rise 4% per year for 10 years? What if the exchange rate moves 15% against you? Tools like cFIREsim allow you to model variable spending assumptions over time, approximating destination-specific inflation scenarios. Our FI Calculator shows how different expense levels affect your timeline to FI. Neither tool perfectly models geoarbitrage risk, but running scenarios with higher assumed costs gives a more honest picture of plan resilience.

-

These are two distinct risks that both erode your purchasing power when retiring abroad, and they can operate independently. Local inflation risk means the things you buy in your destination country cost more in local currency each year — your grocery bill goes up in Thai Baht, regardless of what the exchange rate does. Currency risk means the exchange rate between your portfolio currency and the local currency moves against you — so even if local prices stay flat, you need more USD or EUR to buy the same Baht. Both risks compound each other in fast-growing economies and both sit completely outside the assumptions of standard safe withdrawal rate research.

Join readers from more than 100 countries, subscribe below!

Didn't Find What You Were After? Try Searching Here For Other Topics Or Articles: