The Dutch Box 3 Tax Reform Explained: What Changes in 2028 and What It Means for Your Investments

Amsterdam’s iconic canals as the Netherlands prepares a major Box 3 tax overhaul. Photo by Supradoc on Unsplash.

Reading time: 7 minutes

Quick answer:

The Dutch Box 3 reform replaces fictional assumed returns with taxation of actual annual investment gains—including unrealized ones on liquid assets like ETFs. The main argument in favour is fairness: people should be taxed on what they actually earn. The main arguments against: it penalises long-term savers, creates liquidity problems, distorts incentives toward property, and can meaningfully delay Financial Independence—in some scenarios by 5+ years. The reform is planned for 2028 but still subject to Senate approval.

What you’ll get from this article:

✔ What Box 3 is, and why courts forced reform

✔ What the new system taxes (stocks, ETFs, real estate, illiquid assets)

✔ The “bridging” regime until 2028

✔ Pros/cons: fairness vs complexity, liquidity risks, and potential workarounds

✔ FI math: how annual tax drag can delay your timeline

✔ What to do about policy risk (and how to model it)

TL;DR — Dutch Box 3 Reform 🇳🇱📈

⚖️ Courts forced reform after ruling the old “fictional return” system unfair

🧾 New plan targets actual annual returns, with rollout aimed for 2028

💧 Liquidity risk: some investors may need to sell assets to pay their taxes

🏠 Housing asymmetry: primary homes are mostly outside Box 3, so incentives may tilt toward homeownership

🌍 Unusual in Europe: most countries tax wealth or realized gains, not annual returns

🧠 Behavioral effects (relocation, asset shifts) could reduce the revenue governments expect

🧮 FI impact: even ~1% annual drag on returns can delay Financial Independence by years

⚠️ Big picture: policy risk is rising. Build margin of safety into long-term plans

🛠️ Action step: stress-test your FI timeline with more conservative return assumptions

Dutch Box 3 Reform: Pros and Cons at a Glance

| Point | Detail | |

|---|---|---|

| ✅ | Fairer taxation | People taxed on actual returns, not fictional ones |

| ✅ | Eliminates lock-in effect | No incentive to hold losing assets just to defer tax |

| ✅ | Stable government revenue | Less dependent on market timing than realized gains taxes |

| ✅ | Corrects historical over-taxation | Fixes the unfair fictional returns applied during the low-rate era post-2008 |

| ❌ | Liquidity risk | Investors may need to sell assets to cover tax bills |

| ❌ | Penalises long-term savers | Annual drag on compounding can delay Financial Independence by 5+ years |

| ❌ | Valuation challenges | Illiquid assets like startups and art are difficult to value annually |

| ❌ | Housing asymmetry | Owner-occupied homes largely exempt, tilting incentives toward property |

| ❌ | Behavioural risk | May trigger capital flight, residency changes, or asset restructuring |

| ❌ | Administrative complexity | Heavy burden for both taxpayers and tax authorities to implement fairly |

The Netherlands’ Planned Unrealized Gains Tax — Could It Spread Across Europe?

The Netherlands is overhauling its “Box 3” investment tax system. From January 1, 2028—pending final Senate approval—the new framework will tax actual annual investment returns, including unrealized gains on liquid assets like ETFs and stocks. The old system, which taxed fictional assumed returns regardless of what investors actually earned, was ruled unlawful by Dutch courts in 2021.

For long-term investors and anyone on the path to Financial Independence, this matters for one concrete reason: taxing returns annually reduces compounding—and as we'll show below, even a 1–1.5% annual drag can delay Financial Independence by five or more years.

Beyond the technical tax challenges, the reform also raises a deeper moral and economic question: how many times should the same euro of savings be taxed? European investors typically earn income that is first taxed through income tax, then taxed again when investments are sold at a profit—capital tax on realized gains. Moving toward annual taxation of unrealized gains introduces a potential third layer of friction—especially if investors must sell assets to pay for the tax. Critics view this shift as a meaningful change to long-term savings incentives.

In this article, we’ll break down what has actually changed in the Netherlands, why courts forced reform of the old system, how the new rules may affect stock market returns and long-term compounding, and what this could mean for your own FI projections. This is relevant to consider even if you don’t live in the Netherlands, since tax policy experiments on private wealth are closely watched—and sometimes copied—across Europe.

By the end, we’ll have a clearer sense of whether to adjust your expected returns, your strategy, or your margin of safety on your path to Financial Independence.

Taxing unrealized gains can create real cash-flow pressure for investors. Photo by Kaboompics on Pexels

The Context: Why the Netherlands Is Changing Box 3

The Dutch income tax system is divided into three categories called “boxes”. Box 1 covers employment income and primary residence, Box 2 covers substantial business ownership (owning more than 5% of a business), and Box 3 covers most personal investments and savings. The planned reform is often referred to as the “Wet werkelijk rendement box 3” (Actual Return Box 3 Act).

From 2001 to 2017, Box 3 did not tax your actual investment returns. Instead, the government assumed you earned a fixed fictional return on your wealth and taxed you on that assumption regardless of the reality of your investment portfolio. For example, if the state considered a 4% return and applied a 30% tax, you effectively paid about 1.2% of your assets annually—no matter whether your portfolio went up or down. Even in a year when your portfolio dropped 25%, the tax system still assumed roughly a 4% gain.

Without going into the merits of such a system, it was simple and predictable. But it became increasingly detached from reality after the global financial crisis pushed interest rates toward zero. Many savers—remember this applies not only to stock market investors—were earning close to 0–1% while the tax system still assumed returns of around 4%.

To address this criticism, the government introduced a major reform in 2017. Rather than using a single flat assumed return for everyone, the new method applied different deemed returns depending on the size and composition of your wealth. It was based on the assumption that wealthier households would hold more investments and less cash. Therefore, higher net worth households faced higher assumed returns and taxes, even during years when their portfolios performed poorly.

Dutch courts, including the Supreme Court, eventually ruled the system unfair because it violated the principles of proportional taxation and property rights: taxpayers were being taxed on income they never actually received. Imagine having €500,000 invested in a low-yield environment earning 1% (€5,000), but being taxed as if you earned 4-6% (€20,000–€30,000).

Many savers, especially conservative ones, ended up paying tax that consumed a large share of their real return. Courts found this particularly problematic, as mentioned, after years of ultra-low interest rates. So while politicians always frame it as “making sure wealthy investors pay their fair share,” the legal trigger for the latest reform was actually protecting taxpayers from fictional over-taxation.

Following the Supreme Court’s landmark 2021 ruling, the Dutch government was forced to redesign Box 3 again. A temporary “bridging” system is currently in place while officials work toward a fully new framework scheduled for 2028 that aims to tax actual investment returns more directly. Until 2028, the tax authority still uses assumed returns, but taxpayers can request taxation based on lower actual returns under a rebuttal mechanism—an approach widely described as administratively heavy.

So what does the proposal actually tax—and where do the problems start?

Favorable treatment of owner-occupied housing may further tilt incentives toward property. Photo by Gaurav Jain on Unsplash.

What the New Box 3 System Taxes (and Why It’s Complicated)

While the old Box 3 system assumed returns, the new framework aims to tax actual returns, including interest, dividends, rental income, and in many cases unrealized market gains on financial assets. However, its implementation is complex and still evolving. Portfolios composed of stocks, ETFs, or bonds are the clearest targets because they have observable market prices.

But illiquid assets, such as startup shares or private equity, create valuation challenges, and policymakers have acknowledged the system must treat them carefully to avoid administrative chaos. This is one of the major technical criticisms raised by economists.

Another practical concern raised by critics is liquidity. Because the planned system would assess tax based on value changes even when assets are not sold, many investors could need to sell a portion of their portfolio to cover the tax bill. Such sales can themselves trigger further realized capital gains, potentially creating an additional layer of taxation.

Real estate receives special treatment depending on usage. Owner-occupied primary residences generally fall under Box 1, not Box 3, which already creates a clear asymmetry critics highlight. Some analysts argue this can distort investment choices by favoring homeownership over financial investing and may indirectly disadvantage renters who are unable to enter today’s expensive housing market and instead build wealth through financial assets.

From a generational perspective, critics note the system may offer relative protection to households whose wealth is concentrated in owner-occupied housing, while younger cohorts—who often face greater difficulty accessing the housing market and rely more on financial assets—could be more exposed to Box 3 taxation.

It’s also not hard to imagine unintended, second-order effects could arise from this change in incentives. If financial portfolios face relatively higher taxation than owner-occupied housing, the policy could strengthen incentives to allocate wealth toward property. In already supply-constrained urban housing across the Netherlands and wider Europe, even small demand shifts could impact property prices.

Consider two households each worth €1 million. One has most of its wealth tied up in an owner-occupied home, which largely falls under Box 1. The other rents their home and holds €1 million in ETFs within Box 3. Despite having worked and saved to reach roughly the same net worth, the second household can face significantly higher ongoing taxation on their financial assets.

The system is creating unequal treatment of assets and indirectly providing incentives to build wealth through certain paths. But what about people who are simply not into real estate and don’t want to buy a house?

Furthermore, assets like art, jewelry, collectibles, and other financial assets that don’t have secondary markets to accurately gauge their price add another layer of complexity, as they are theoretically part of taxable wealth but notoriously difficult to value annually, creating both potential loopholes and enforcement challenges.

Cross-border mobility is another major concern. Dutch residents are taxed on worldwide assets, so moving money abroad does not eliminate liability. However, individuals can change tax residency, restructure ownership through companies, or shift toward assets treated differently under the new rules.

Historically, even modest wealth taxes in Europe triggered behavioral responses. France saw periods of high-net-worth migration during earlier wealth tax regimes, and Sweden ultimately abolished its wealth tax in part due to capital flight concerns. Whether the Dutch reform reaches that level remains uncertain, but policymakers are clearly aware of the risk.

Will other European countries follow the Dutch approach to taxing wealth? Photo by Antoine Schibler on Unsplash.

Is the Netherlands the First — and Could Others Follow?

Netherlands is not the first European country to tax wealth, but its move toward taxing actual annual returns—including unrealized gains on liquid assets such as publicly traded stocks—is relatively unusual. Countries like Switzerland, Norway, and Spain operate classic net wealth taxes, where a percentage of total net worth is taxed each year regardless of performance.

Importantly, though, many of these systems include substantial exemptions or high starting thresholds, meaning the tax often applies primarily to higher-net-worth households rather than typical middle-class investors or younger generations trying to build wealth.

For FI investors building a long-term index investing portfolio, the key difference is compounding. Systems that allow tax deferral let wealth accumulate more efficiently, while annual taxation of returns tends to apply a steady brake to long-term portfolio growth.

By contrast, most large EU economies, including France and Germany, primarily tax realized capital gains, meaning that taxes are generally triggered only when you sell assets.

All of these structural differences matter. Under a traditional wealth tax (say 1% of assets) the annual drag is relatively stable but largely disconnected from market performance. Under a realized gains system like Germany’s, long-term investors benefit from powerful tax deferral, allowing portfolios to compound mostly uninterrupted for decades.

The Dutch approach reduces this deferral advantage and, over time, can compound into a meaningful gap in final portfolio value or a longer timeline to Financial Independence.

The question for other countries, especially in Europe, is whether this type of policy may spread. Although there are no confirmed initiatives, the broader policy backdrop suggests the question is not entirely hypothetical. Across Europe, governments are grappling with aging populations, rising pension costs, and persistent budget pressures.

One country’s policy change can travel to others faster than investors expect. Consider the recently approved social media ban in Australia and how it took days for other governments to take up the discussion. For FI-minded households, the takeaway is not that identical rules will spread everywhere, but that capital taxation is firmly back on the European policy agenda. Long-term plans for FI investors should be built with this increasing uncertainty in mind.

If this sounds abstract, the FI math makes it concrete—small annual drags can add years to your working career.

Liquidity risk: some investors may need to sell assets to pay annual tax bills. Photo by Towfiqu Barbhuiya on Pexels

FI Math: How Much Can Annual Tax Drag Delay Financial Independence?

For FIRE investors, the critical question is about compounding. Under the old Dutch system, the effective drag depended on the assumed return versus your real return. Under the new approach, the drag becomes more directly tied to market performance.

To illustrate, suppose a long-term global equity portfolio earns 7% real returns. If we assume Box 3’s taxation effectively removes roughly 1–1.5 percentage points annually in a typical equity-heavy portfolio, your net real return would likely fall into the 5.5–6% range.

In scenarios where investors must periodically realize gains to fund tax payments, the effective drag could be slightly higher. (If you want to see how sensitive your own timeline is to even small return changes, this is exactly the kind of scenario worth stress-testing in a FI calculator.)

Let’s consider a case study to estimate the impact on FI timeline. Consider a young household with the following characteristics:

Age: 26

Net annual income: €50,000

Annual expenses: €42,000 (16% savings rate)

Portfolio value: €0

Safe withdrawal rate: 4% (as per the 4% rule of thumb)

Real annual return on investments: 7% (baseline scenario) vs 5.5% (annual taxation scenario)

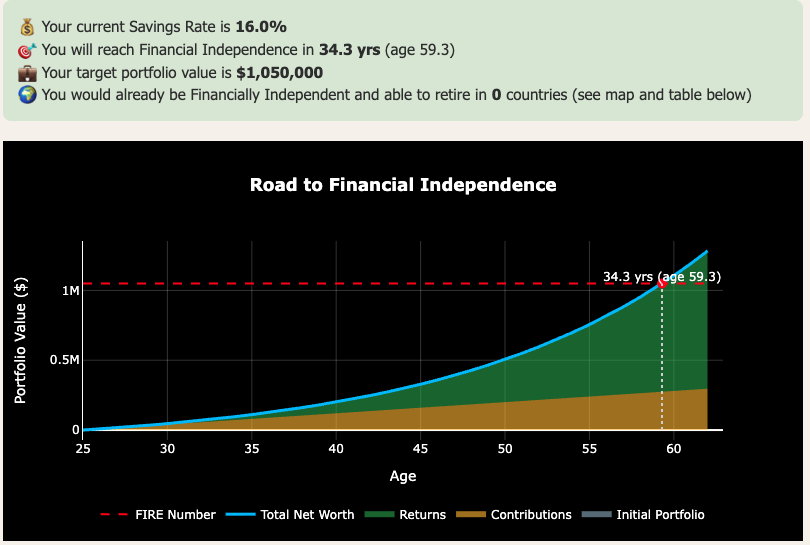

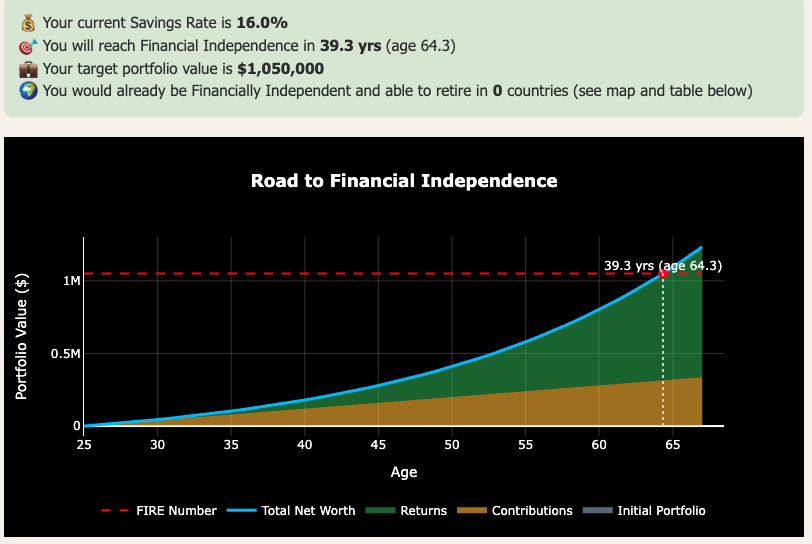

As per our free FI Calculator and as observed in Figure 1, the household reaches Financial Independence after 34 years at age 59 under in the baseline scenario. If we implement a 5.5% rate of return, though, this timeline would be lengthened by 5 full years to age 64.

Taxing unrealized gains of your portfolio on an annual basis can extend your working career by five years (Figure 2). The implementation of this policy therefore has a dramatic impact on your ability to grow wealth. In practice, the exact impact also depends on how aggressive your savings rate is: this policy will impact disproportionately more households with lower savings rates and impact comparatively less aggressive FIRE savers.

Figure 1. Screenshot of our free FI Calculator (email unlock). In the baseline scenario, our household example works 34.3 years until Financial Independence.

Figure 2. Screenshot of our free FI Calculator (email unlock). In the unrealized tax scenario, our household example works 39.3 years until Financial Independence—5 more than in the baseline scenario.

Dutch Box 3 Reform: Pros, Cons and Trade-offs

On the surface, there are good-faith arguments on both sides. Supporters argue wealth accumulation should contribute more to public finances, especially as populations age and pension systems strain. Critics counter that investment capital is generally already funded from after-income-tax in Europe, and that layering additional taxes—on unrealized capital gains on top of realized ones—risks penalizing long-term savers relative to consumers.

There is also an important philosophical tension. Governments are simultaneously warning citizens to save more for retirement due to the fragility of the European pension systems, while at the same time disincentivizing savings and investments by adding tax frictions.

The contrast becomes even clearer when viewed internationally. In the US, for example, retirement systems such as 401(k) plans and traditional IRAs explicitly incentivize long-term investing of its citizens by allowing contributions with pre-tax income and tax-deferred growth for decades.

Although there have been some changes in attitude towards encouraging investing in major European countries (e.g., Germany’s Early-Start Pension, which sets up investment accounts automatically for kids), the Dutch example shows how differently countries view the role of investing of their citizens.

The hard part is predicting how people will respond. When economists warn about relocation of capital, it’s not just wiring money abroad. It means high-net-worth individuals changing residency, investors favoring assets treated more favorably (with unintended consequences, for example potentially inflating housing market), or entrepreneurs structuring ownership differently. These behavioral shifts help explain why wealth-related taxes across Europe have often raised less revenue than headline projections initially suggested.

Investors in the Netherlands will unfortunately have to incorporate more conservative assumptions in their long-term planning and remain attentive to how the rules evolve before full implementation in 2028. As mentioned, higher savings rates can offset part of the additional drag, and portfolio structure may matter more than in the past.

Periodically stress-testing your plan under different return and tax scenarios—using tools like our FI calculator—can help quantify the real impact on your timeline to early retirement. Over the longer term, some households may also consider geographic flexibility in retirement, including geographic arbitrage or seasonal relocation, as tax residency continues to play a meaningful role in European wealth taxation.

For investors elsewhere in Europe, there is no guarantee other countries will follow this same path, but the broader direction of travel—greater scrutiny of private wealth in a fiscally constrained environment—is becoming harder to ignore. FI plans that assume today’s tax rules will remain the same for 30–40 years may prove very optimistic.

The bottom line for me is to remember the importance of policy risk, which is increasingly part of the investing landscape in many countries. The most resilient FI strategies are not built on perfect forecasts, but on flexibility, margin of safety, and the ability to adapt if the rules of the game change.

If you enjoyed this article, here are some next steps:

👉 Stress-test your own timeline to FI using our free FI Calculator (email unlock).

👉 For the full investing and retirement framework—see our complete guide to investing for Financial Independence

👉 Subscribe to get free FI tools and the weekly newsletter (one-click unsubscribe anytime).

💬 Do you think policies like the Dutch Box 3 reform could spread across Europe? How, if at all, are you preparing your portfolio for that possibility?

🌿 Thanks for reading The Good Life Journey. I share weekly insights on personal finance, financial independence (FIRE), and long-term investing — with work, health, and philosophy explored through the FI lens.

Disclaimer: I’m not a financial adviser, and this is not financial advice. The posts on this website are for informational purposes only; please consult a qualified adviser for personalized advice.

Check out other recent articles

About the author:

Written by David, a former academic scientist with a PhD and over a decade of experience in data analysis, modeling, and market-based financial systems, including work related to carbon markets. I apply a research-driven, evidence-based approach to personal finance and FIRE, focusing on long-term investing, retirement planning, and financial decision-making under uncertainty.

This site documents my own journey toward financial independence, with related topics like work, health, and philosophy explored through a financial independence lens, as they influence saving, investing, and retirement planning decisions.

Frequently Asked Questions (FAQs)

-

Box 3 is the Dutch tax category for most personal savings and investments (stocks, ETFs, cash, second homes/investment property). It’s separate from Box 1 (salary/primary home) and Box 2 (substantial business ownership). The reform aims to move Box 3 from assumed returns toward actual returns.

-

The target start is 1 January 2028, but the bill still needs Senate approval and the Finance Minister has indicated amendments may be needed, so the timeline remains politically and technically sensitive. The practical takeaway: treat 2028 as the working plan, not an unchangeable certainty.

-

For liquid assets with clear market prices (stocks/ETFs), the planned approach can effectively tax annual value changes, which resembles taxing unrealized gains. But some assets (e.g., certain real estate, startup shares) may be treated differently because valuations are harder, creating a hybrid system.

-

Courts ruled that taxing “fictional” returns—especially after 2017—could violate property rights and anti-discrimination principles when real returns were lower. The key issue was being taxed on income you didn’t actually earn. This triggered a legal and political necessity to redesign Box 3.

-

Until the new regime starts, Box 3 still relies on assumed returns, but taxpayers can claim taxation based on lower actual return under rebuttal rules. This creates extra administrative burden and uncertainty because it mixes deemed rates with case-by-case correction.

-

It can. Broad index funds often deliver most of their return via price appreciation, not cash dividends. If tax is due on annual value increases, investors without cash buffers may need to sell some holdings to fund the bill—potentially realizing gains and adding friction. The effect varies by portfolio and final rules.

-

Annual tax drag reduces compounding. In FI math, even a 1% reduction in long-run net returns can delay FI by years, especially for households with modest savings rates.

-

Not the first to tax wealth, but the move toward taxing actual annual returns—including value changes on liquid assets—is relatively unusual in Europe. Many countries either tax net wealth annually or tax capital gains primarily when assets are sold.

-

There’s no confirmed wave, but the Netherlands is being watched because it’s a large “test case” for taxing annual returns in a modern EU economy. With pension and budget pressures, the policy idea may be discussed elsewhere even if implementation differs.

-

Build margin of safety: stress-test returns, keep flexibility in withdrawal timing, consider tax diversification, and avoid FI plans that only work under perfect assumptions. Your FI calculator CTA is the right tool because it turns abstract policy risk into a concrete timeline impact.

Join readers from more than 100 countries, subscribe below!

Didn't Find What You Were After? Try Searching Here For Other Topics Or Articles:

<script>

ezstandalone.cmd.push(function() {

ezstandalone.showAds(102,109,110,111,112,113,114,115,119,120,122,124,125,126,103);

});

</script>