Geographic Arbitrage & FIRE: The Complete Guide

The view that changes the calculation — sometimes the most powerful Financial Independence lever is simply where you choose to land. Photo by Nils Nedel on Unsplash.

Reading time: 15 minutes

Geographic Arbitrage for FIRE: The Complete Guide to Retiring Abroad

Quick answer:

Geographic arbitrage means using differences in cost of living between countries or regions to your financial advantage. For FIRE (Financial Independence, Retire Early), it works two ways: retiring abroad to stretch your portfolio further and retire sooner, or working abroad in a higher-salary country to build wealth faster during the accumulation phase of Financial Independence (FI). This guide covers both—with a primary focus on retiring abroad, real numbers, region-by-region rankings, the tax realities, and other trade-offs to consider.

What You'll Get From This Guide

✔ The real numbers: how many years retiring abroad can save you (with examples)

✔ A framework for choosing a retirement destination across 9 retirement suitability variables—not just cost of living

✔ Region-by-region rankings: Europe, Asia, Latin America, the Nordics

✔ The tax picture when retiring abroad—what to check, what to ignore, and what actually matters

✔ Seasonal geoarbitrage: how to benefit without permanently leaving home

✔ Expat Barista FIRE: semi-retiring abroad before reaching your full FI number

✔ The longevity dimension: why where you retire may affect how many healthy years you have

✔ A dedicated section on working abroad to accelerate your accumulation phase

TL;DR — Geographic Arbitrage at a Glance 🌍

🗺️ Two use cases: retiring abroad (lower spending, earlier exit) and working abroad (higher savings, faster accumulation)

📉 The maths: lower cost of living reduces your required portfolio and what you need to withdraw—two levers working together

⏳ The impact: geoarbitrage can cut 5–10+ years off your FIRE timeline—much more than optimising returns

🔢 The 9 variables: cost of living is just one—safety, healthcare, climate, stability, and lifestyle all belong in the decision

💸 Tax nuance: capital gains headline rates are rarely what you actually pay—but wealth and exit taxes sometimes matter more

🏡 No need to fully commit: seasonal geoarbitrage lets you benefit without permanently leaving home

🏖️ Semi-retirement option: Expat Barista FIRE can get you to semi-retirement in under 7 years starting from zero

💼 Working abroad: earn more, save faster—the accumulation play that can shave years off your timeline before you ever retire

Geographic Arbitrage for FIRE: Why Location May Be Your Biggest Lever

Most Financial Independence (FI) content focuses on optimizing two levers: save more, invest better. But there is a third lever that gets comparatively less attention—and for many people it has a bigger impact than either: where you choose to live, and specifically whether retiring abroad could fundamentally change your timeline.

Every $1,000 you cut from your annual retirement spending reduces the portfolio you need to accumulate by roughly $25,000, as per the 4% rule of thumb. Retire somewhere with €15,000 lower annual costs than where you currently live, and suddenly you need roughly €375,000 less as your portfolio target.

For most of us, that’s not a marginal difference, but the difference between working several more years. That is the core logic of geographic arbitrage: you are not optimising your investment returns or squeezing your savings rate further. You are changing the portfolio target itself.

This guide covers two different ways geoarbitrage can change your FIRE timeline: retiring abroad to reduce your portfolio target and working abroad during accumulation phase of FI to build it faster. It also covers what most guides skip: 9 different variables that matter beyond cost of living; the tax picture that people routinely over- and underestimate; and other options that don't require permanent relocation.

If you're short on time: the Quick Answer and TL;DR above give you the essentials in under two minutes. If you want the full framework—numbers, destinations, tax picture, and how to build your own plan — the complete guide is below.

A note on where this comes from: I've been pursuing Financial Independence from Germany for the past seven years as a foreigner—which puts me in an interesting position on the geoarbitrage question. Working here has meaningfully accelerated my path to FI relative to my home country in Southern Europe. And yet I'm unlikely to retire here. So I've thought about both sides of the geoarbitrage coin more than most: how to use location to build wealth faster, and where to eventually deploy it. This guide is built partly from that experience, and partly from the data we've accumulated across 100+ countries and several years of writing about FIRE at The Good Life Journey.

Porto, Portugal. In our recent analysis, Portugal ranked as the top destination for retirement in Europe.

How Many Years Can Geographic Arbitrage Save You? The Real Numbers

The Dual Maths Effect: Why Geoarbitrage Works Better Than It Looks

Retiring abroad does not just reduce your annual spending. Because your Financial Independence (FI) number is a multiple of your spending, reducing your spending also reduces the portfolio you need to accumulate in order to reach FI in the first place. These two effects combined are more powerful than they appear at first sight.

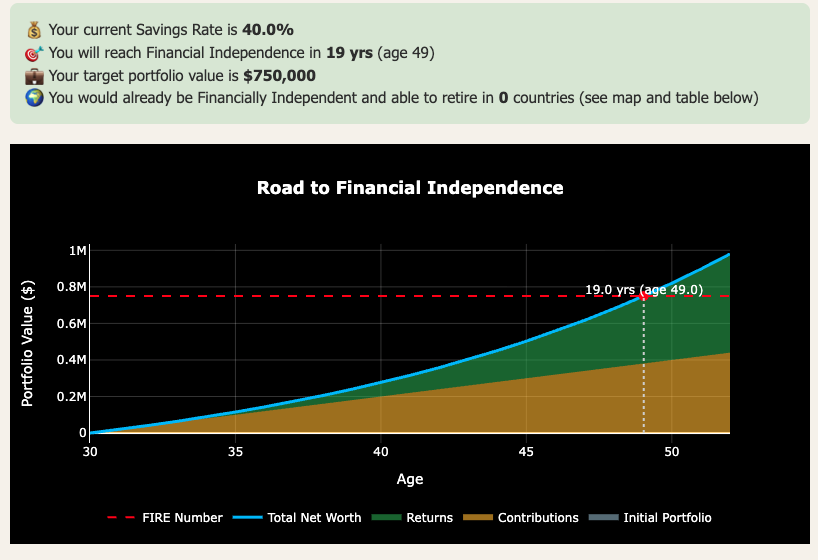

Consider the following example: someone earning a salary in Germany of around $50,000 and saving aggressively at a 40% savings rate. Using a FI Calculator, their path to Financial Independence takes roughly 19 years (Figure 1).

Figure 1: Screenshot of our FI Calculator (free, email unlock). Assuming a $50,000 salary, 40% savings rate, and a 7% real return on investments, the baseline timeline to FI is around 19 years for a 30-year old with no savings.

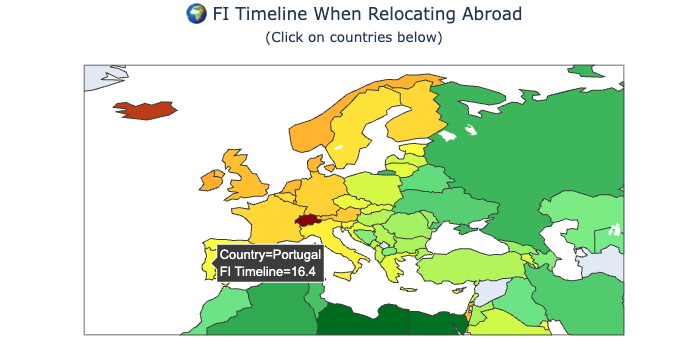

Now consider if the same person decided to retire in Portugal instead of Germany, not only because they wanted to lower their annual spend but also because they genuinely preferred the climate, culture, or lifestyle. Their annual spend (and portfolio needs) would also drop roughly by 25%, shortening their FI timeline by 3 years to 16 years (see our FI Calculator map in Figure 2).

That’s earning three full years of freedom without needing to earn more, invest better, or make any dramatic sacrifice. On the contrary—you're moving to the beach in Portugal and eliminating 36 months of Zoom meetings in the process.

Figure 2: Screenshot of our FI Calculator (free, email unlock). Under the conditions assumed above, moving to Portugal at retirement reduced the FI timeline by about 3 years. The Calculator allows you to visualize how your FI timeline changes depending on which 100+ country you decide to retire to.

Push further to destinations like Thailand, Indonesia, or Mexico and the retirement timeline gap starts to widen substantially by about 6-8 years. The gap becomes even larger if your starting home country is more expensive, e.g., the US or Switzerland.

These are not theoretical numbers; we’ve modelled them in detail using our FI Calculator across many destinations, and the pattern is clear: the cost-of-living reduction lever reduces the timeline to retirement more reliably than nearly any other factor. This makes geoarbitrage one of the most powerful levers available to anyone starting FIRE later in life, where every year shaved off the timeline counts double.

👉 Deep dive: How Much Earlier Could You Retire Abroad? The Timeline Maths

👉 Deep dive: The Atlas of FIRE: What Your Retirement Number Looks Like in 100+ Countries

📊 Want to run these numbers for your own situation and country? Our free FI Calculator models the geoarbitrage effect across 100+ countries and produces a similar global map to the one displayed above (email unlock):

Why this often beats chasing returns

Many investors say they prefer to optimize their timeline by improving their investment returns. The problem is that this return optimization is, in the best of cases, uncertain and limited. Reliably adding 1-2% to long-term returns consistently comes with higher risk and is extraordinarily difficult, even for professional investors.

For most retail investors, attempting to chase returns through stock picking and high-conviction bets doesn’t produce higher returns in the vast majority of cases, but lower ones and a later retirement. Geoarbitrage, by contrast, works with near-mathematical certainty: a 30% reduction in annual expenses is a 30% reduction in required portfolio. You don't need markets to cooperate or any investor skill.

You just need to move. This is why geoarbitrage has become one of the most discussed strategies in the FIRE community—not because it requires financial sophistication, but precisely because it doesn't.

There is also a lifestyle upside for many people. If you come from a high-cost northern European or North American city, retiring in places like Lisbon, Chiang Mai, Playa del Carmen, and many others (see further below) isn’t a tradeoff but often means retiring with a higher standard of living than in your home country—better weather, richer food culture, and a slower pace—all at a fraction of the cost.

The maths make the case. But knowing geoarbitrage can shorten your career is only half the answer—the other half is knowing where.

The Decision Framework — More Than Just Cost of Living

Why the Cheapest Country Is Rarely the Right Answer — and What to Use Instead

However, the biggest mistake in geoarbitrage is optimitzing purely for cost. The countries with the lowest cost of living often also come with the sharpest trade-offs on safety, healthcare quality, political stability, or infrastructure that only become clear once you are actually living there.

A retirement that saves you $20,000 per year in living costs but puts you in constant danger or in a situation of insecure healthcare is certainly not a good trade to make.

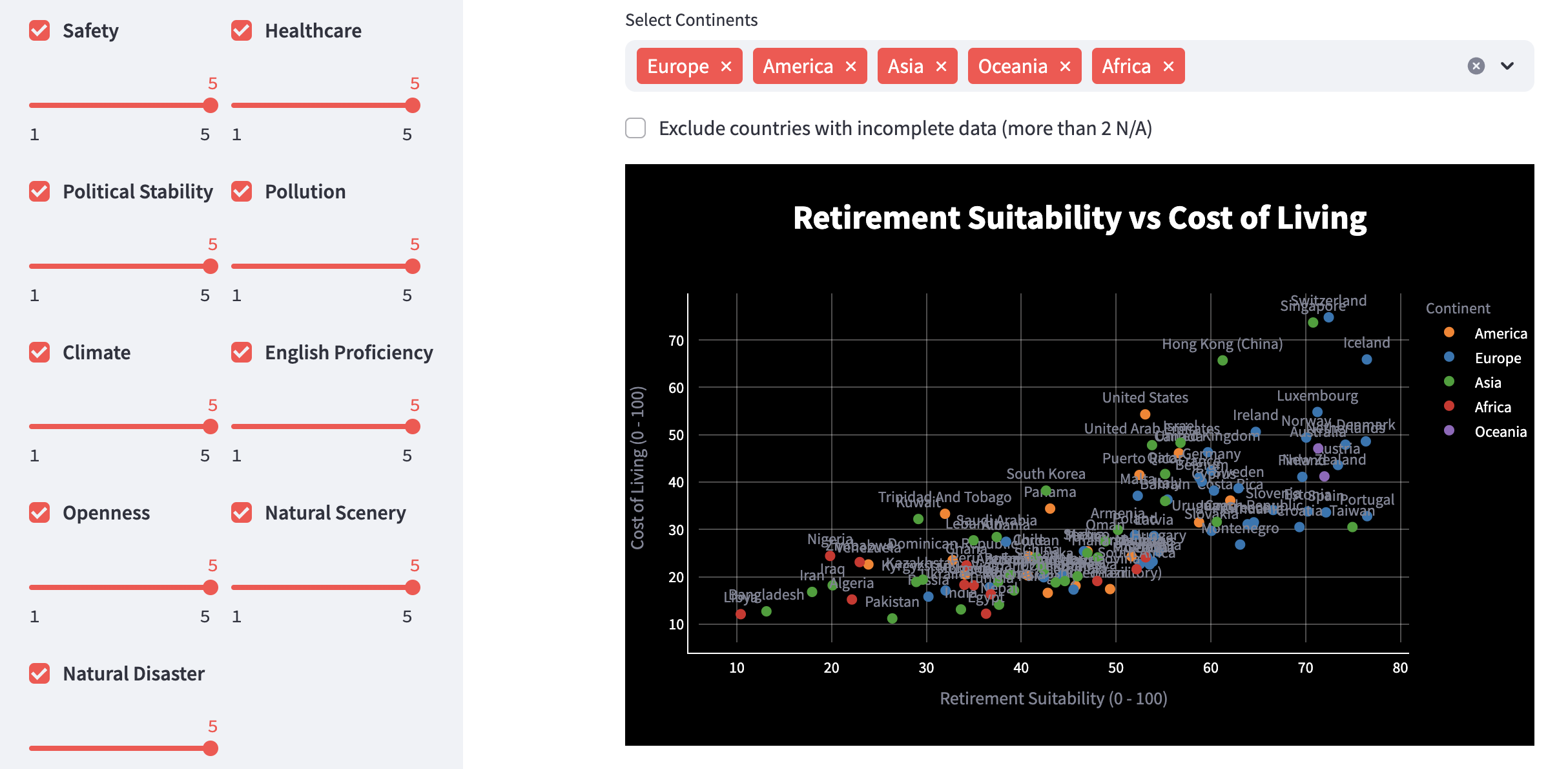

Over the past few years, we’ve developed a data-driven Retirement Relocation Tool (Figure 3), which evaluates over 100 countries across 9 retirement suitability variables. In addition to cost of living, it considers:

Safety

Healthcare quality

Political stability

Pollution levels

Climate

English proficiency

Openness to foreign residents

Natural Scenery

Natural disaster risk

For a full breakdown of sources, variable weights and tool limitations, see our methodology guide.

In practice, the relative weight of these variables differs dramatically between individuals. A retiree with a chronic health condition will weight healthcare quality very differently from a healthy 42-year-old. This is exactly why we built the tool with adjustable sliders rather than a single fixed ranking—everyone can decide on the relative importance of the variables.

In addition, we use cost-of-living figures sourced from Numbeo, the largest crowd-sourced database of cost-of-living data globally.

Figure 3: Screenshot of our free Retirement Relocation Tool (email unlock). It uses cost of living and 9 other retirement suitability levers to identify best retirement destination candidates.

The practical value of the tool is that you can adjust the weighting of the different retirement suitability variables to reflect your own priorities. As observed in the screenshot above, you can adjust the different levers across different variables. The sliders let you tighten or relax requirements for each factor. Move the safety slider from 5 to 4, for instance, and it drops the 20% lowest-scoring countries on safety from the results—leaving only destinations that clear your threshold.

👉 Deep dive on the full framework: Best Countries for Geographic Arbitrage in 2026 (Ranked)

👉 Try the free tool (email unlock): Retirement Relocation Tool

Europe — A Natural First Stop for Many FIRE Retirees

For people pursuing FIRE from Europe or with European roots, the continent has obvious appeal: freedom of movement across 27 EU countries, healthcare systems that are broadly high-quality and often accessible to long-term residents, cultural familiarity, and a climate that ranges from cool Nordic to warm Mediterranean.

It’s not the cheapest region in the world—Southeast Asia and Latin America offer lower costs—but the combination of quality, accessibility, and lifestyle makes it a very popular starting point for many.

Top 5 destinations in Europe

Our data-driven ranking for Europe places Portugal, Spain, Croatia, Greece, and Cyprus at the top, after considering both cost of living and a combination of the 9 retirement suitability variables presented above.

Each of these countries offers a meaningfully lower cost of living than their northern European counterparts without the stronger trade-offs found in some of the cheapest global options. Spain and Portugal in particular have well-established international communities, good infrastructure, and a lifestyle that many northern European retirees find very appealing. In many cases, it’s not just cheaper, but the quality of life for a retiree can be superior.

👉 Deep dive and rankings: Best Countries to Retire in Europe in 2026

Another factor increasingly worth weighing alongside cost and safety islocal social reception. Anti-tourism sentiment has grown significantly in parts of Spain, Portugal, and Italy—and it affects long-term expat residents, not just tourists:

👉 Deep dive: “Tourist Go Home”: What Europe's Anti-Tourism Backlash Means for Expat Retirees

The Nordics: high quality, high cost

Don’t mind (or actually enjoy) the cold and snow? The Nordic countries rank very highly globally on safety, healthcare, and quality of life. The downside is they are expensive compared to other regions. However, depending on where you are coming from you can also find lower-cost options outside major cities.

Within the five Nordics, Denmark is one of the most popular choices—high English fluency, exceptional healthcare, and a coastal lifestyle that gets surprisingly affordable outside Copenhagen. Though safety scores lower than its Nordic counterparts, Sweden is the most affordable of the five and scores well across most retirement variables. Finland is underrated: consistently among the world's safest and happiest countries, with lower costs than its neighbours. Norway is the expensive outlier—although beautiful, high costs plus a wealth tax on large portfolios make it hard to justify financially. Iceland is a lifestyle choice more than a financial one: breathtaking and safe, but small, remote, and costly.

👉 Deep dive: Which Nordic Country Makes the Most Sense for Early Retirement?

If you're based in Germany and Denmark has caught your eye, we ran the numbers on exactly that comparison. The intuitive assumption is that Denmark's higher costs and more complex investment tax structure make it the weaker financial choice for retirement—but the answer depends heavily on housing. Coastal Danish properties, particularly in rural areas and in islands like Ærø, can be dramatically cheaper than equivalent German real estate. If you own rather than rent, that gap could more than offset the tax disadvantage between the two countries. It requires careful personal modelling though.

👉 Case study: Retiring in Denmark vs Germany: Can Low-Cost Homes Beat Higher Taxes?

A forward-looking note: climate change

Climate change is a factor that barely featured in retirement destination decisions a decade ago, but now increasingly belongs in the conversation. This isn't purely a future concern; in parts of Southern Europe today, summer heat already shapes daily life in ways that matter for retirement.

In July and August across much of Spain, Greece, and Southern Italy, outdoor activity is effectively curtailed for several hours in the middle of the day, and prolonged heat exposure carries real physiological risks: heat stress, cardiovascular strain, and disrupted sleep hit older adults harder—both in frequency and severity. Some of these regions are projected to see substantially more days above 30°C in the decades ahead, compounding what is already a challenging summer baseline.

In the context of early retirement timelines that could last 40–50 years, the climate a destination has today may look quite different in a couple of decades. For a 40-year-old retiring now, the climate of their chosen destination in 2050 should not be an abstraction, but part of the retirement they are planning for. Northern coasts, Atlantic-facing regions, and higher-altitude locations are expected to become more attractive as climate change impacts progress.

👉 Deep dive: How Climate Change Will Reshape Europe's Best Retirement Destinations

Cavtat, Croatia. In our recent analysis, Croatia ranked in the top-5 destinations for retirement in Europe. Photo by Conor Rees on Unsplash.

Asia and Latin America — Higher Cost Advantage, Different Trade-offs

For retirees willing to look beyond Europe, Southeast Asia and Latin America offer cost-of-living advantages that Europe simply cannot match. The trade-offs are real but manageable with the right research.

Asia

The financial case for Southeast Asia is strong: in countries like Thailand, Indonesia, Malaysia, and Vietnam, you can find a very comfortable lifestyle—good food, quality accommodation, and beautiful natural environment—that can cost 40-60% less than in the US or Western Europe.The trade-offs differ across countries but tend to centre on healthcare access, visa stability and rule changes, and cultural adjustments.

Our data-driven rankings highlight which countries perform best when you weight cost of living alongside other important retirement suitability variables.

👉 Deep dive: Best Countries to Retire in Asia (2026 Rankings & Costs)

Latin America

Latin America follows a similar pattern to Asia: the lowest-cost options demand more selectivity on safety at the city level, while the safer and more stable destinations like Uruguay or Costa Rica offer a straightforward transition for western retirees but are also more expensive. Our deep dive below explores the different trade-offs and presents a retirement suitability ranking for the region.

👉 Deep dive: Best Countries to Retire in Latin America (2026)

The cross-regional comparison

If safety is one of the critical levers you consider when evaluating low-cost of living countries for early retirement, we explored this exact question in our article below, covering the different regions of Europe, Asia, and Latin America. It is particularly useful if you have not yet narrowed down a region and want to see the full picture before committing to deeper research.

👉 Deep dive: Safest and Most Affordable Countries to Retire in 2026: Europe, Asia & Latin America Compared

In our recent analysis, Thailand ranked in the top-3 destinations for retirement in Asia. Photo by Darren Lawrence on Unsplash.

Taxes When Retiring Abroad: What Actually Matters (and What Doesn't)

Why people overestimate capital gains tax

One of the most common factors would-be-retirees evaluate is the capital gains tax (CGT) rate of destination countries. If you are withdrawing money from an investment portfolio in Spain and Portugal and see a headline CGT of 25-28%, it’s easy to assume that almost a quarter of your withdrawal goes to the government. This is almost never what actually happens.

With some exceptions (e.g., Netherlands), CGT applies only to the gain component of your portfolio—the growth above your original contributions. So, if your $1M portfolio was built roughly from $600,000 in contributions and $400,000 in gains, and you withdraw $40,000, only the proportion representing gains (roughly $16,000 in this example) is subject to CGT.

The calculation itself is more complex than what’s shown above, but the key message here is that the effective tax rate on a full withdrawal is much lower than the headline rate—often 10–15% in practice where statutory rates are 25–28%.

The actual tax bill is considerably more manageable than many fear, and therefore choosing a retirement destination based solely on CGT headline rates is generally not a good idea and can lead to a poor decision.

There is no universal answer on tax efficiency when retiring abroad. It depends on many factors, including portfolio size, asset mix, country of origin, and the specific country's treaties. The figures above are illustrative; always model your own numbers with a local tax adviser before relocating.

👉 Deep dive: Retiring Abroad? You're Probably Overestimating Your Capital-Gains Tax

👉 Deep dive: Capital Gains Taxes and Financial Independence in Retirement Locations

The taxes that sometimes matter more

That said, capital gains is not the only tax story. Several other levies can matter significantly more:

Wealth taxes (annual taxes on total net worth, not just gains) exist in Spain, Norway, and a handful of other countries, and can be more damaging to a large portfolio than CGT

Exit taxes: Some countries charge tax on unrealised gains when you leave, not when you sell—relevant if you are considering relocating back to your home country at some point

Inheritance and estate taxes are often overlooked in early retirement planning but worth modelling, particularly in countries with complex succession rules

The Dutch Box 3 reform is a live example of how investment taxation can shift in ways that matter for FIRE planning. The Netherlands has long taxed investment wealth, but the new system moves from assumed fictional returns to actual annual returns—including unrealised gains. The broader lesson is that the tax environment in any country should be treated as dynamic: model your plan under current rules, but also stress-test it against plausible changes.

👉 The Netherlands exception explained: A Tax on Unrealized Gains in Europe? The Dutch Box 3 Reform Explained

Seasonal Geoarbitrage: Get the Financial Benefits Without Leaving Home Permanently

The most common psychological barrier to geoarbitrage is the assumption that it must mean permanently leaving your home country. Many folks understandably don’t want to leave their family, social network, and roots behind.

Seasonal geoarbitrage partially removes this barrier. The idea is simple: rather than relocating once permanently, you split your year between locations, spending part of it in a lower-cost country and part at home. You still get most of the financial benefit without some of the downsides of permanent relocation.

The Numbers: How Much Seasonal Geoarbitrage Actually Saves

One case study we recently modelled: a Germany-based early retiree spending six months in Germany, three in Spain, and three in southwest France, on a €60K annual budget. The cost-of-living reduction comes out at approximately 15%, which translates to a reduction in the annual withdrawal rate from 4% to roughly 3.4%—a meaningful improvement in portfolio longevity and a significant buffer against sequence of returns risk in the early years of retirement.

Seasonal geoarbitrage also works well as a trial run before any permanent decision (taking a mini-retirement does too). Living somewhere for three or four months gives you a real impression on whether you actually enjoy it—something that is difficult to replicate with a two-week holiday. It reduces the risk of making a permanent decision you may later regret.

👉 Full case study and framework: Seasonal Geoarbitrage: Live Better for Less Without Leaving Your Roots

👉 The money side of seasonal geoarbitrage: The setup for spending months abroad without conversion fees

🗺️ Not sure where to start? Our Retirement Relocation Tool (email unlock) lets you filter 100+ countries by cost, safety, healthcare, and climate in under 2 minutes:

Expat Barista FIRE — Semi-Retiring Abroad Before You Hit Your FI Number

What is Barista FIRE?

Barista FIRE is a hybrid FIRE strategy where you stop working your main career before reaching full Financial Independence, and instead cover part of your living expenses through flexible, lower-stress, part-time work. This allows your investment portfolio to continue compounding in the background.

The name comes from the idea of working a relaxed coffee-shop job for income and benefits rather than staying on the corporate treadmill. It is particularly well-suited to people who are burned out and need to stop, but have not yet quite crossed the full FI finish line.

Add geoarbitrage and the timeline compresses dramatically

Expat Barista FIRE combines this approach with geographic relocation. The logic is to move to a lower-cost country, reduce your required annual spending significantly, cover the remainder through some form of flexible work, and let your existing portfolio continue growing until it reaches the level needed for full FI. At that point the part-time work becomes optional.

The headline result from our analysis: this approach can realistically get you to semi-retirement in under 7 years, even for people who have not yet built a substantial portfolio. The compressed timeline comes from two forces working together—lower cost of living abroad shrinks the portfolio you actually need, and the willingness to earn a modest income means you don't need to fully fund your lifestyle from investments yet. Neither lever alone gets you there nearly as fast; combined, they can move the semi-retirement date by over a decade.

👉 Deep dive with examples: Expat Barista FIRE: Achieve Semi-Retirement Abroad in Under 7 Years

Costa Rica is not only one of the five original Blue Zones for longevity, but tops our ranking of best locations to retire in Latin America. Photo by Frames For Your Heart on Unsplash.

The Longevity Dimension — Blue Zones and Healthy Aging Abroad

Most retirement relocation decisions are made on financial and lifestyle grounds. There is a third dimension worth considering too: where you retire may affect not just your finances but how many healthy years you have to enjoy them (i.e., healthspan).

This is where the concept of “Blue Zones” becomes relevant. The five original regions identified by longevity researcher Dan Buettner where people live significantly longer and healthier lives than average and share a set of lifestyle characteristics: daily natural movement, a plant-rich diet, strong social bonds, a sense of purpose, and a slower pace of life.

What is interesting from a FIRE (Financial Independence, Retire Early) perspective is that several of these Blue Zones actually overlap with regions that already appear in retirement destination rankings—think Italy, Greece, or Costa Rica. All are places where an early retirement could, almost by default, incorporate the lifestyle patterns associated with exceptional longevity.

A retirement designed around walkable communities, fresh food, outdoor activity, and genuine social integration is likely to produce better health outcomes than one designed purely around financial optimisation. And better health outcomes mean more years of genuinely active retirement—which changes the whole picture of what your portfolio needs to support.

👉 Deep dive: Retire Early in a Blue Zone: Where Healthy Aging Meets Lifestyle Design

So far, everything above has been about retirement—spending less, living better, lasting longer. The final section flips the direction entirely: using geography not to reduce spending in retirement, but to maximise income during the years you're still building wealth.

Working Abroad to Build Wealth Faster: The Accumulation-Phase Play

Note: In contrast to all the above, this section covers the accumulation phase of Financial Independence—working in a higher-salary country to build wealth faster. It is a different decision from the retirement relocation content above, and the best countries for each purpose are often different.

The framework: salary-to-cost-of-living ratio

During the accumulation phase, the logic of geoarbitrage runs in reverse. Instead of moving somewhere cheap to spend less, you move somewhere with high net salaries relative to local costs in an attempt to maximize your savings rate—the most important predictor on the length of your FI timeline. In the majority of cases it means moving to a more expensive country.

The global top destinations for accumulation

Our recent analysis of 43 countries put Luxembourg, Switzerland, Qatar, the US, Kuwait, Denmark, the Netherlands, UAE, Australia, Germany, and Sweden at the top for building wealth quickly. Luxembourg and Switzerland lead because of exceptionally high net salaries, even relative to their high cost of living; Gulf countries (Qatar, Kuwait, UAE) combine high gross salaries with zero or very low income tax, producing strong net take-home pay; and English-speaking markets like the US and Australia offer large labour markets with strong salary levels.

👉 Deep dive: Top 11 Countries to Work Abroad and Achieve Financial Independence (2026)

Country-level data is a starting point, but not the final answer. Within any country, city-level differences in salary and cost of living can be just as significant as the differences between countries. In the deep dive below, we mapped this across 37 European countries and 90+ cities, and separately across 51 US and Canadian cities, and the variation was substantial in both cases.

👉 Deep dive: Where to Work and Build Wealth in Europe (2026 Rankings)

👉 Deep dive: Best and Worst Cities in the US and Canada for Financial Independence in 2026

One final note worth emphasising: the best country to work in during accumulation phase of FI is rarely the same as the best country to retire in—and that's fine. Think of them as two separate optimisation problems, in two separate phases of the same journey. If you're willing to optimise both phases—where you work and where you retire—the combined effect on your timeline can be dramatic.

Germany: A Personal Case Study in Accumulation-Phase Geoarbitrage

We also covered the accumulation phase in Germany specifically—a separate piece based on my own experience as a foreigner living here. It documents the pros and cons of pursuing FI in Germany: what you actually take home after tax and social contributions, the housing question, and what it's like trying to build wealth in a country that isn't exactly known for its investing culture. Regarding this last point, though, things are slowly changing.

👉 Deep dive: How to Retire Early in Germany: Key Insights into Financial Independence

Choosing where to retire is less about finding one “best” country and more about aligning location with your priorities. Photo by Denise Jans on Unsplash.

📬 We publish new country-level analysis and FIRE articles every week. Subscribe here—one-click unsubscribe anytime:

Conclusion: Building Your Own Geoarbitrage Plan

Like most meaningful life decisions, there are no purely right answers or decisions without trade-offs—proximity to family, healthcare familiarity, and language are real costs that don't show up much in geoarbitrage discussions. The maths is compelling, but the decision is very personal.

Geographic arbitrage doesn’t come in a single flavor. It ranges from a few months of seasonal living in a lower-cost country, to Expat Barista FIRE in Southeast Asia, to full permanent relocation. The right point on the full spectrum of options depends on your own priorities, your family situation, your health, and how much lifestyle change you are genuinely comfortable with.

A practical approach to finding your point on that spectrum:

Start with the maths. Use a FI Calculator to model the effect of a 20%, 30%, or 40% reduction in annual spending on your required portfolio and timeline. This tells you how much the financial lever is actually worth to you before you make any lifestyle decisions. Our Calculator produces this geoarbitrage calculation automatically across 100+ countries in a single interactive map.

Define your non-negotiables. Healthcare access, language, family proximity, climate preferences—these are the filters that rule destinations in or out before cost even enters the conversation. They vary from person to person.

Use the 9-variable framework to build a shortlist of retirement candidate countries. Don't trust any single ranking; adjust the weights to reflect your own priorities. The cheapest country is rarely the right answer.

Stress-test the tax picture. Check specifically for wealth taxes, exit taxes, and the stability of the CGT regime—not just the headline rate. Try to figure out what your effective tax rate would be on annual withdrawals.

Plan the money logistics before the move. Whichever destination you choose, your income will likely arrive in one currency while your life runs in another—for years. Left to your bank’s default exchange rates, that costs a retiree thousands per year in hidden conversion markups. Our guide to managing your money when you move abroad covers the three-account setup that fixes this once, before you leave.

Model a return home scenario. A portfolio sized for lower costs abroad may not comfortably fund a return to the expensive city you left. That's not a reason to avoid geoarbitrage—but it is a reason to plan with a buffer, or to think of a potential return in terms of a cheaper domestic location rather than your original base.

Stress-test your destination, not just your portfolio. Most geoarbitrage plans treat today's cost advantage as permanent—but popular destinations can change. Local inflation, currency movements, and growing expat demand have already eroded the cost advantage in Lisbon, Chiang Mai, and parts of Eastern Europe. Our guide to geoarbitrage and rising costs covers this risk in detail with real data from Thailand and Portugal.

Try before you commit. Seasonal geoarbitrage or taking a mini-retirement is the lowest-risk way to gather real data. Before committing to any permanent relocation, try a few months in a couple of candidate destinations.

The financial case for geoarbitrage is strong enough on its own. But for many people the more compelling realization is that retiring in a place with better weather, fresher food, a slower pace, and a stronger community often produces a genuinely better and healthier life, not just a cheaper one.

Many places that appear at the top of retirement destination rankings tend to overlap, not coincidentally, with the regions where people live the longest and stay healthiest. The financial case and the quality-of-life case often point in the same direction.

If you enjoyed this guide, here are some next steps:

👉 Estimate your FI timeline using our free FI Calculator (email unlock) and how it changes with geoarbitrage

👉 New to The Good Life Journey? Check out our Start Here archive section for all our Financial Independence articles

👉 Subscribe to get free FI tools and the weekly newsletter (one-click unsubscribe anytime)

💬 Are you considering geoarbitrage—for retirement, work, or both? Share with us in the comments where you're thinking and what's holding you back.

🌿 Thanks for reading The Good Life Journey. I share weekly insights on personal finance, financial independence (FIRE), and long-term investing — with work, health, and philosophy explored through the FI lens.

Disclaimer: I’m not a financial adviser, and this is not financial advice. The posts on this website are for informational purposes only; please consult a qualified adviser for personalized advice.

Check out other recent articles

About the author:

Written by David, a former academic scientist with a PhD and over a decade of experience in data analysis, modeling, and market-based financial systems, including work related to carbon markets. I apply a research-driven, evidence-based approach to personal finance and FIRE, focusing on long-term investing, retirement planning, and financial decision-making under uncertainty.

This site documents my own journey toward financial independence, with related topics like work, health, and philosophy explored through a financial independence lens, as they influence saving, investing, and retirement planning decisions.

Frequently Asked Questions (FAQs)

-

Geographic arbitrage means using cost-of-living differences between countries or regions to your financial advantage. In FIRE, it works two ways: retiring abroad to stretch your portfolio further, or working abroad to build wealth faster. Because your FI number is a multiple of your annual spending, a 25–30% reduction in expenses reduces the portfolio you need by the same proportion—often cutting several years off your career timeline without touching your savings rate or investment returns.

-

Based on our modelling across 100+ countries, retiring in Portugal instead of Germany can shorten a FIRE timeline by approximately 3 years for someone with a 40% savings rate. Moving to Southeast Asia or Latin America—where costs run 40–60% lower than Western Europe—can compress timelines by 6–10 years or more. The effect is larger the more expensive your home country is.

-

For early retirement in Europe, our 2026 ranking puts Portugal, Spain, Croatia, Greece, and Cyprus at the top—lower costs without the sharper trade-offs of the cheapest global options. In Asia, Thailand, Malaysia, and Indonesia offer the largest cost advantages. In Latin America, Uruguay and Costa Rica offer the smoothest transition; Colombia and Mexico the largest savings with reduced tradeoffs. The right answer depends heavily on your priorities across safety, healthcare, climate, family proximity, and other factors.

-

No. Seasonal geoarbitrage captures most of the financial benefit without permanent relocation. In our Germany-based case study—six months at home, three in Spain, three in southwest France—annual spending dropped by around 15%, reducing the effective withdrawal rate from 4% to 3.4%. That meaningfully improves portfolio longevity without leaving family or roots behind.

-

CGT applies only to the gain portion of your withdrawal, not the full amount. For a typical FIRE portfolio after 20 years of accumulation, roughly 50–55% of a withdrawal represents gains. Applying Spain or Portugal’s progressive brackets to that portion produces an effective rate of around 10–12% on the full withdrawal—well below the 26–28% headlines. Wealth taxes and exit taxes sometimes matter more than CGT, and are worth checking specifically.

-

Expat Barista FIRE combines relocation with a hybrid semi-retirement strategy: move to a lower-cost country before reaching full FI, cover part of living expenses through part-time work, and let your portfolio compound toward full independence in the background. In our case study, a household starting from zero reached semi-retirement in Thailand after 7 years.

-

Seasonal geoarbitrage means splitting your retirement year between your home base and one or more lower-cost locations—typically 3–5 months somewhere cheaper and warmer. In our Germany-Spain-France case study, a 15% spending reduction translated to a 0.6 percentage point drop in withdrawal rate, from 4% to 3.4%. Beyond the numbers, it also functions as a low-commitment way to test destinations before any permanent decision.

-

Even if you never relocate, modelling the geoarbitrage effect is useful—it tells you what optionality you have if you ever need to reduce spending. Many FIRE planners find that knowing they could reduce withdrawals by 20–30% through relocation allows them to retire with a higher SWR than they'd otherwise be comfortable with. It's a planning tool as much as a lifestyle decision.

-

Beyond capital gains tax, three things deserve specific attention: wealth taxes (Spain and Norway both charge annual taxes on net worth above a threshold); exit taxes (some countries tax unrealised gains when you leave, not when you sell); and inheritance taxes (often overlooked but worth modelling). The Dutch Box 3 reform is a useful case study in how tax rules can change after you've already relocated.

-

Several of the most financially attractive FIRE destinations overlap with Blue Zone regions—areas where people live significantly longer and healthier lives. Greece and Costa Rica appear in both retirement destination rankings and longevity research. The lifestyle patterns associated with Blue Zone longevity—walkable communities, fresh food, strong social bonds, slower pace—tend to be more accessible in lower-cost countries than in high-cost urban environments.

Join readers from more than 100 countries, subscribe below!

Didn't Find What You Were After? Try Searching Here For Other Topics Or Articles:

<script>

ezstandalone.cmd.push(function() {

ezstandalone.showAds(102,109,110,111,112,113,114,115,119,120,122,124,125,126,103);

});

</script>