Why I’m Comfortable With a 5% Withdrawal Rate (Even for Early Retirement)

Flexible retirees have multiple safeguard levers they can pull if markets underperform (see Table below). Photo by Tima Miroshnichenko on Pexels.

Reading time: 8 minutes

Quick answer:

A 5% safe withdrawal rate (SWR) can be reasonable for some early retirees—but only when paired with flexibility and risk management. The traditional 4% rule assumed rigid spending and limited asset classes. In practice, many FIRE-focused retirees have multiple levers they can pull if markets underperform. Used thoughtfully, a higher withdrawal rate can significantly shorten your timeline to Financial Independence. But it is not universally safe and requires honest self-assessment around flexibility, risk tolerance, and backup options.

What you’ll get from this article:

✔ When a 5% safe withdrawal rate can be reasonable for early retirees

✔ Why many historical 4% rule “failures” assume unrealistic retiree behavior

✔ The flexibility levers that meaningfully improve withdrawal sustainability

✔ How SWR assumptions can shift your Financial Independence timeline by years

✔ The biggest risks and who should avoid a 5% withdrawal strategy

✔ How to balance mathematical safety vs. real-life freedom in early retirement

TL;DR — 5% Withdrawal Rate 🎯

📉 The classic 4% rule assumed rigid spending and limited diversification

📊 Updated research from Bill Bengen suggests slightly higher rates may be viable

🔄 Dynamic spending rules can materially improve sustainability

🧠 Early retirees have unique flexibility (income options, geoarbitrage, etc.)

🛡️ Tools like bond tents and valuation awareness can reduce sequence risk

⏳ The biggest hidden cost: overly conservative withdrawal rates can delay FI by years

⚠️ 5% is not for everyone—rigidity and long horizons increase risk

🧮 Bottom line: flexibility is what turns 5% from reckless into potentially reasonable

The Flexibility Levers Behind a 5% Plan

Before we dive into the details, it helps to see the bigger picture. A 5% withdrawal strategy doesn’t need to rely on a single optimistic assumption—it can become more robust when combined with multiple flexibility levers. Think of these as practical risk-management tools you can use in early retirement.

The table below summarizes the key flexibility levers you can actively use to strengthen a 5% withdrawal strategy, when they tend to matter most, and the trade-offs to keep in mind.

| Lever | How it helps | When it matters most | Trade-offs / caveats |

|---|---|---|---|

| Spending flexibility (ad-hoc cuts) | Temporarily reducing discretionary spending lowers withdrawal pressure during downturns | First 5–10 years (sequence-of-returns risk window) | Requires willingness to adjust lifestyle in weak markets |

| Guardrails (rule-based adjustments) | Creates structured rules for when to cut or raise spending based on portfolio health | Any time markets move sharply | Can feel restrictive; requires discipline to follow the rules |

| Income backstop (only if needed) | Even modest earnings can materially reduce drawdowns in poor markets | Prolonged downturns; weak early returns | Not guaranteed; depends on skills and willingness |

| Lifestyle income (likely anyway) | Passion projects or light work can naturally offset withdrawals | Often emerges organically within first decade of FIRE | Uncertain and variable; shouldn’t be required for baseline success |

| Geoarbitrage | Lower cost of living reduces withdrawal rate when it matters most | Early retirement years; during market stress | Family, visa, tax, and lifestyle constraints may apply |

| Bond tent / glidepath | Reduces need to sell equities after a crash in early retirement | First 5–10 years | Depends on yields, tent size, and allocation mix |

| Valuation awareness | Starting conditions influence long-term returns and sequence risk | At retirement start | Not a timing tool—only a risk awareness input |

| Spending smile awareness | Recognizes that spending often declines later in retirement | Mid-to-late retirement planning | Early retirees must remain flexible given long horizons |

Let’s now unpack why each of these levers materially changes the traditional 4% conversation.

When a 5% Safe Withdrawal Rate Can Work (and When It Doesn’t)

In some FIRE (Financial Independence, Retire Early) forums, the 4% rule of thumb is often treated as gospel. But in the real world, retirees don’t behave as rigidly as the original models underpinning this rule assume. In this article, I’ll show when a 5% safe withdrawal rate can be reasonable for early retirees, when it becomes risky, and which flexibility levers can meaningfully improve the odds.

The goal is not to claim that withdrawing 5% is universally safe—it isn’t—but to help you make a more informed trade-off between retiring sooner and playing it ultra-safe.

Before we go further, though, a quick definition. A “safe withdrawal rate” (SWR) is the percentage of your investment portfolio you plan to withdraw each year to fund life after you stop working. In other words, it’s a post-retirement concept: you’ve hit Financial Independence (FI), and now the question becomes how much you can sustainably take out each year from your portfolio without depleting it over the long term.

The exact percentage number this should look like is heavily debated in the early retirement community because it directly determines how big your portfolio “needs” to be. A plan implementing a 3% SWR requires a much larger nest egg to retire than a 5% one—often meaning years of additional work. So you can see why this can be a heated conversation—there are many potential years of freedom at stake.

When I first started modeling our own plan, I defaulted to a very conservative 3.5–4% withdrawal rate. It felt prudent and sensible at the time. What I hadn’t really thought through was the key trade-off: every small drop in the withdrawal rate was adding years to the FI timeline just to protect against very low-probability scenarios. Only after digging deeper into sequence risk, spending flexibility, and how early retirees actually behave did I start to question why such conservative withdrawals are implemented.

In this article I'll focus on why 5% can be reasonable for some people when paired with safeguards. For the detailed mechanics behind the classic 4% rule or Bill Bengen's updated 4.7% analysis, see our complete guide to safe withdrawal rates for early retirees.

Withdrawal rate assumptions have a direct impact on how long you need to work. Photo by Mikhail Nilov on Pexels.

The “4% Rule” Has Already Evolved

It’s worth remembering that the famous 4% rule (of thumb) was never meant to be some universal law of nature. It was the output of a specific historical analysis that used a relatively narrow set of asset classes and fairly rigid assumptions.

As researchers have improved the analysis—adding more asset classes and better data—the “safe” withdrawal number has changed. So, the first takeaway is to remember that we shouldn’t only care about the exact percentage number, but understand that the results depend heavily on the assumptions that are used.

Bill Bengen, the creator of the 4% rule, recently updated his analysis and produced a figure that is closer to 4.7%, after looking beyond only large-cap US stocks and intermediate Treasuries. While that doesn’t automatically make a 5% withdrawal rate safe, it does narrow the gap between what many FIRE adherents treat as conservative and what updated research suggests may be viable under broader portfolio diversification.

Crucially, both the study underpinning the 4% rule and Bengen’s updated work still assumes fixed, inflation-adjusted withdrawals regardless of market conditions. I find this to be one of the biggest disconnects between academic modeling and human behavior in practice.

In the historical failures of the 4% rule, retirees were modeled as continuing to spend the same real amount even as they observed their portfolios tank severely. In practice, very few financially-engaged early retirees would behave in this way—they would adjust, at least slightly, their spending. And when you fully grasp the implications of this real-world behavior it makes even the updated 4.7% rule look conservative. After all, the 4.7% updated rule of thumb is also supposed to weather some of the worst-case scenarios.

The original framework was intentionally rigid to make it easier to model, not because retirees should withdraw fixed amounts every year no matter what. When we recognize this, it becomes clearer that the “safe number” is highly sensitive to behavioral assumptions and that the methodology matters just as much as the headline percentage number we’re considering. Retirement researchers such as Wade Pfau and Michael Kitces have similarly shown that withdrawal sustainability improves significantly when spending flexibility is introduced.

If improving diversification already moves the historical boundary of SWR closer to 4.7%, forcing your plan down to 4% or even 3% as advocated by very risk-averse FIRE folks could mean unnecessarily working several years more to build a larger portfolio. This trade-off illustrates that this isn’t just a math problem but also a lifestyle design decision. As we’ll discuss in more detail later on, there is a lifestyle risk-reward tradeoff to consider.

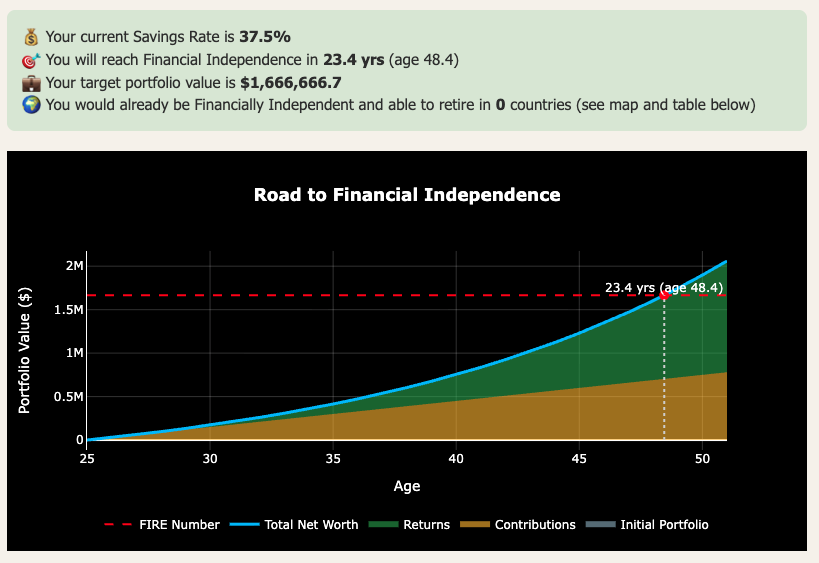

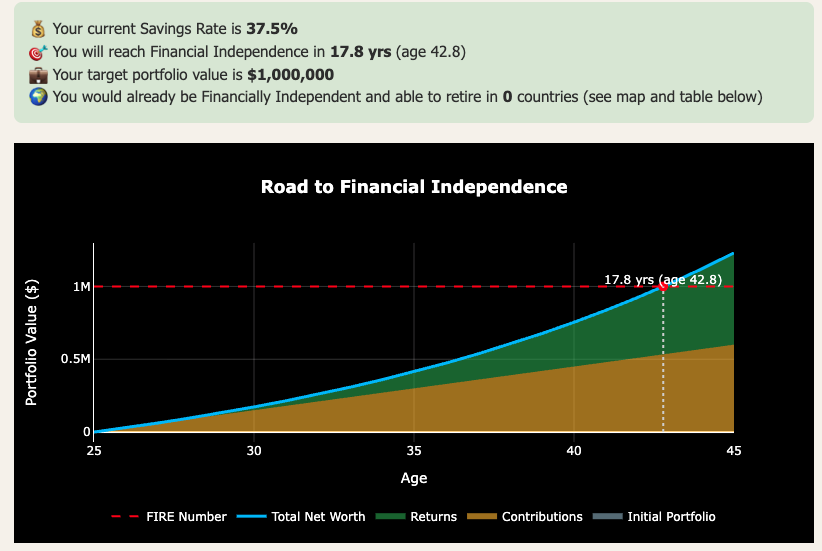

To make this concrete, here’s what different withdrawal rate assumptions can do to your timeline to early retirement. Below is the same situation modeled with a more conservative SWR (3%—Figure 1) versus a higher SWR (5%—Figure 2) .

As observed, the difference in timeline to retirement between both scenarios is 5.6 years. That’s 67 months of your life to take back potentially earlier, when you’re still relatively young and fit. Of course, your own timeline will depend on your savings rate, spending, and investment assumptions. If you haven’t run your personal numbers yet, this is exactly where many FIRE plans benefit from a quick reality check. If you want, you can use our free FI Calculator (email unlock).

Figure 1. Output of our FI Calculator (free, email unlock). Timeline to early retirement under a conservative 3% SWR scenario. Assumptions: age (25), annual net income ($80,000), annual spending ($50,000), annual real returns on investment (7%).

Figure 2. Output of our FI Calculator (free, email unlock). Timeline to early retirement under a conservative 5% SWR scenario. As observed, this scenario reaches early retirement 5.6 years faster than using a 3% SWR. Assumptions: age (25), annual net income ($80,000), annual spending ($50,000), annual real returns on investment (7%).

Next, we discuss how dynamic withdrawal strategies—as opposed to static ones—can act as safeguards for implementing higher withdrawal rates than are traditionally considered in the FIRE space.

Why Dynamic Spending Makes Higher Withdrawal Rates More Viable

A key reason many historical “failures” of the 4% rule appear so fragile is the very rigid assumption that spending never adjusts. In other words, the “safe” withdrawal rate depends heavily on how rigid your spending actually is in retirement.

In classic backtests using historical data, retirees are assumed to keep withdrawing their inflation-adjusted amount even through deep bear markets. But in the real world people adapt. They delay big purchases, trim discretionary travel, pause renovations, or are naturally less spendy until their portfolios have recovered slightly.

When researchers model guardrails or other dynamic spending frameworks (such as Guyton-Klinger style rules), sustainable starting withdrawal rates frequently move up into the ~4.8%–5.6% range depending on parameters. In other words, flexibility is not a minor tweak, but can fundamentally change the retirement math and the portfolio you need to target.

This is where the gap between textbook assumptions and real retiree behavior starts to matter. Early retirees—and especially FIRE folk—aren’t robots following fixed spending year after year irrespective of how their portfolio looks, but highly engaged planners who routinely monitor and update their spreadsheets. If markets turn ugly, the majority will notice and adapt.

This ability to remain somewhat flexible in retirement spending is one of the strongest arguments for why a thoughtfully managed 5% starting point may be reasonable for certain profiles.

Bogleheads’ Variable Percentage Withdrawal (VPW) framework further reinforces this conclusion through another lens.VPW explicitly ties withdrawals to both portfolio value and age. Early withdrawal percentages in aggressive stock-to-bond allocation often land not far from the 5% benchmark.

The key insight from VPW isn’t that VPW is more conservative, but that higher withdrawal rates can work when spending is allowed to flex with market reality. From a FI timeline perspective, this matters greatly: if modest flexibility can support even a slightly higher starting rate, many FIRE seekers could reclaim more years of working life—years that would otherwise get sacrificed to protect agains extremely low-probability events.

Markets can be volatile early in retirement—guardrails help smooth the ride. Photo by Pixabay on Pexels.

Early Retirees Have Unique Safety Mechanisms

One of the most overlooked hidden assets early retirees have is human capital flexibility. Someone retiring in their 30s, 40s, or even 50s is very different from a traditional 65-year-old retiree. Skills are fresher and the ability to generate some level of income—whether consulting, freelance work, passion-driven projects, or in the online economy—is often still strong.

It really doesn’t take much income to dramatically improve your portfolio longevity. Even modest earnings during poor market environments can materially reduce withdrawal pressure during the most dangerous first stages of retirement, where early retirees face sequence-of-returns (SORR) risk.

When you factor this ability to produce some income into the overall risk picture, the binary “portfolio survives or fails” framing that is used in many studies, again, becomes overly simplistic. There are simply many ways one can react in the face of a very unlucky, prolonged market downturn early in retirement.

Closely related to this is the reality that many early retirees don’t actually want to earn zero forever. A meaningful portion will gravitate toward some form of productive activity—entrepreneurial experiments, creative work, advisory roles, or part-time engagement on their own terms. This is not about needing to grind again, but the fact that in many cases optional income will organically emerge for many engaged lifestyles.

When planning a 5% withdrawal strategy, acknowledging this adds another layer of resilience. Personally, if we reach FI at age 42–44, it is highly unlikely we’ll just sit on our hands and never earn any income again. This is another soft backstop traditional models—designed for clean math—don’t fully capture.

Geoarbitrage and lifestyle mobility add another practical layer of protection, especially for those who enjoy travel. Temporarily or seasonally living in a lower cost-of-living region can meaningfully reduce withdrawal pressure, especially in the vulnerable early years of retirement. For many in the FIRE community, this isn’t even a sacrifice—travel and location flexibility are often part of the retirement vision from the start. We explore this approach in depth, including how geographic arbitrage and optional income can replace years of extra saving, in our dedicated article on why flexibility beats a 3% withdrawal rate.

Importantly, this lever can work both proactively and defensively. You might choose to spend time in lower-cost locations early in retirement simply because you want to explore the world while you’re still young, which indirectly reduces SORR when it matters most.

But it can also serve as a temporary backstop if markets turn ugly. Knowing you have the option to reduce expenses geographically adds another margin of safety that rigid retirement models rarely capture, while potentially shortening your timeline to Financial Independence in the first place.

Location flexibility can be a powerful lever to reduce withdrawal pressure. Photo by Nils Nedel on Unsplash.

Portfolio Design and Timing Can Reduce Sequence Risk

Sequence-of-returns risk (SORR) remains a central danger for any elevated withdrawal strategy, but thoughtful portfolio construction can meaningfully reduce its impact. One commonly discussed tool is the bond tent: holding a larger allocation to high-quality bonds around the retirement transition and then gradually increasing equity exposure over time.

The goal is not to eliminate risk altogether, but to reduce the probability of being forced to sell large amounts of equities during the most vulnerable early years of retirement. Historical simulations suggest that properly implemented glidepaths can improve success rates, particularly for long-horizon retirees. That said, the impact depends also on starting bond yields, tent size, and overall asset allocation. A bond tent should therefore be viewed as a meaningful risk reducer that can help support higher withdrawal rates at the margin—not a magic lever that automatically makes a 5% SWR safe in all environments.

Starting conditions also matter, and this is where valuation awareness enters the discussion. Historical analysis shows that retirement outcomes are highly sensitive to the valuation environment at the start date of retirement. Metics like CAPE rations have a meaningful predictive power for long-term real returns.

While no one can time markets precisely, early retirees often have more flexibility than traditional ones to adjust their retirement date slightly if valuations are extremely stretched. Even modest awareness here can reduce SORR slightly. This doesn’t require perfection, but simply acknowledging that “not all retirement starting points are created equal.”

Finally, there’s another important factor many people miss: the retirement spending smile. Empirical data suggests many retirees do not spend a constant inflation-adjusted amount for decades, but instead spend more in the early years, moderate in mid-retirement, and often less later in life (the “Go-Go" years, “Slow-Go”, and “No-Go”).

That said, very early retirees need to be thoughtful here given their much longer retirement horizons. The key is not to blindly assume lower future spending, but to recognize that some front-loaded spending is reasonable—Bill Perkins would say necessary—especially if it remains broadly aligned with portfolio performance.

In other words, awareness of the spending smile can support a more balanced withdrawal strategy, but it works best when combined with the same flexibility and market sensitivity discussed earlier on.

Many retirees have more geographic flexibility than they initially assume. Photo by Linh Nguyen on Unsplash.

The Real Risk: Being Too Conservative (Plus Key Caveats)

All this leads to the core risk-reward question: what is the cost of being too conservative? Planning around extremely low-probability worst-case scenarios can easily push your FI number high enough to require many additional years of work (we estimated almost 6 years in our example above). Those years don’t come without cost—they come at the expense of time, energy, family presence, and in many cases health.

Especially for those in demanding careers, the difference between targeting a 3-4% withdrawal rate versus thoughtfully managing around 5% can translate into materially different retirement timelines. The key insight is not that higher withdrawal rates are universally better, but that over-optimization for safety and extreme conservatism has real life costs that deserve equal weight in the decision. As we mentioned at the beginning, this is not only math problem to solve, but also a lifestyle one.

That said, a 5% starting withdrawal rate is not appropriate for everyone. Critics correctly point out that long early retirements leave less room for error, which is why flexibility and margin of safety become especially important at higher withdrawal rates. The strategy becomes far riskier for retirees with highly inflexible spending, very low equity allocations, heavy fixed obligations (large mortgages, private school tuition, etc.), or a complete unwillingness to ever earn again under any circumstance.

It’s also more fragile under extremely long retirement horizons if none of the flexibility mechanisms discussed in this article are considered, and outcomes remain sensitive to starting valuations and inflation regimes. In short, the more rigid your financial life is, the less margin a 5% approach provides.

Personality fit and risk tolerance may be the most important filter. A 5% framework tends to suit better flexible, engaged planners who monitor their finances, are comfortable with making corrections, and value reclaiming time earlier in life. But it’s far less suitable for anxiety-prone investors seeking mathematical certainty or for households running extremely lean budgets with no discretionary buffer in their spending.

In the end, the question isn’t whether a 5% withdrawal rate is universally safe—it isn’t—but whether the trade-off makes sense for your specific situation. Designing your plan to withstand extremely low-probability worst-case scenarios often means working several additional years to build a larger portfolio. Those extra years come with real, overlooked costs: less time with loved ones, fewer healthy and energetic years to pursue travel and hobbies, and more time spent in demanding work that may not align with the life you’re trying to build.

For flexible planners who are willing to adapt if needed, accepting a modestly higher withdrawal rate can be a rational choice, because the life benefits of retiring younger may meaningfully outweigh the small probability of needing to adjust course later on.

If you enjoyed this article, here are some next steps:

👉 See what 3% vs 5% does to your FI timeline: Run our free FI Calculator (email unlock)

👉 New to Financial Independence? Start with our Start Here guide for the full framework.

👉 Subscribe to get free FI tools and the weekly newsletter (one-click unsubscribe anytime).

💬 Where do you personally land on the 3%-to-5% debate—and what flexibility levers give you the most confidence in your plan?

🌿 Thanks for reading The Good Life Journey. I share weekly insights on personal finance, financial independence (FIRE), and long-term investing — with work, health, and philosophy explored through the FI lens.

Disclaimer: I’m not a financial adviser, and this is not financial advice. The posts on this website are for informational purposes only; please consult a qualified adviser for personalized advice.

Check out other recent articles

About the author:

Written by David, a former academic scientist with a PhD and over a decade of experience in data analysis, modeling, and market-based financial systems, including work related to carbon markets. I apply a research-driven, evidence-based approach to personal finance and FIRE, focusing on long-term investing, retirement planning, and financial decision-making under uncertainty.

This site documents my own journey toward financial independence, with related topics like work, health, and philosophy explored through a financial independence lens, as they influence saving, investing, and retirement planning decisions.

Frequently Asked Questions (FAQs)

-

A 5% withdrawal rate can work for some early retirees, but it depends heavily on flexibility, asset allocation, and willingness to adjust spending. Research based on rigid withdrawals is more conservative than real-world behavior. If you have multiple safety levers and remain adaptable, 5% may be reasonable—but it is not universally safe.

-

For highly flexible early retirees, the classic 4% rule can be conservative because it assumes fixed inflation-adjusted spending regardless of market conditions. However, for retirees with rigid expenses or very long horizons, 4% may still be appropriate. The key variable is behavioral flexibility, not just the percentage.

-

There is no single universally safe withdrawal rate. Historical research often points to around 4%, but dynamic strategies, diversification, and flexible spending can support higher starting rates in some cases. Your personal safe rate depends on risk tolerance, portfolio mix, and willingness to adapt over time.

-

Yes—multiple studies show that adjusting spending during downturns significantly improves portfolio longevity. Guardrails, percentage withdrawals, and discretionary spending cuts reduce sequence risk. The biggest failures of fixed withdrawal models often occur because retirees were assumed not to adjust behavior.

-

The impact varies, but moving from a 3–4% assumption to 5% can shift financial independence timelines by several years. Because required portfolio size falls materially, the savings phase shortens. However, this comes with higher sensitivity to market conditions and requires flexibility.

-

Sequence of returns risk refers to the danger of poor market returns early in retirement, when withdrawals begin. Losses in the first decade can have an outsized impact on portfolio longevity. Strategies like bond tents, spending flexibility, and part-time income help mitigate this risk.

-

Often yes. Early retirees typically have stronger human capital, more geographic flexibility, and greater willingness to adjust spending. These factors can improve withdrawal sustainability compared with traditional retirees modeled in many historical studies.

-

Variable Percentage Withdrawal (VPW) is not necessarily safer, but it is more flexible. Because withdrawals adjust with portfolio value and age, VPW avoids the rigidity of fixed real withdrawals. It demonstrates that higher withdrawal rates can be mathematically viable when spending adapts.

-

A 5% rate becomes much riskier if spending is inflexible, equity allocation is low, retirement horizon is extremely long, or the retiree is unwilling to earn supplemental income if needed. Personality and behavioral discipline matter as much as the math.

-

Flexibility often matters more than the precise starting withdrawal rate. Retirees who can adjust spending, earn modest income, or reduce costs during downturns significantly improve success odds. A rigid plan can fail even at lower withdrawal rates.

Join readers from more than 100 countries, subscribe below!

Didn't Find What You Were After? Try Searching Here For Other Topics Or Articles:

<script>

ezstandalone.cmd.push(function() {

ezstandalone.showAds(102,109,110,111,112,113,114,115,119,120,122,124,125,126,103);

});

</script>