Health & Longevity: The Other Half of Your FIRE Plan

Consistent aerobic exercise—whether swimming, running, cycling, or something else—is the single most powerful investment you can make to your longevity. My grandparents swam laps every morning in a retirement that lasted nearly four decades. Photo by Kate Trifo on Unsplash.

Reading time: 15 minutes

Health & Longevity and Financial Independence: The Complete Guide

Quick answer:

Most FIRE (Financial Independence, Retire Early) planning focuses on optimizing your portfolio in relation to the accumulation and drawdown phases of your Financial Independence journey. But almost none of it applies the same rigour to optimizing for our health—which is arguably the most important return of all, determining how long we’ll be able to enjoy our portfolio.

The average American has just 64 healthy years—compared to over 73 in Japan or South Korea, and around 69 in Germany. This guide covers what the science says drives longevity, why your environment matters as much as any health protocol, and how health connects to your FIRE number in concrete financial terms.

What You'll Get From This Guide

✔ Difference between lifespan and healthspan—and why healthspan is what matters for FIRE

✔ The HALE data: healthy years by country, and what explains the gap

✔ What the science says drives longevity across exercise, sleep, and nutrition

✔ Why your physical environment matters as much as any specific health protocol

✔ The mental health and stress dimension—and why FI may be a powerful health interventions

✔ Why being healthy now—during accumulation—matters as much as preparing for later

✔ How health affects your FIRE number: the spending curve, nursing costs, and how healthspan reshapes the plan

TL;DR — Health & Longevity for FIRE 🏃♂️

⏳ Healthspan ≠ lifespan: the average American has ~64 healthy years vs ~73 in Japan

🏥 Many people retire near their healthy life expectancy, building a portfolio they won't enjoy

📊 VO2max is the strongest predictor of all-cause mortality

💪 Sleep, aerobic fitness, and nutrition are the three foundational pillars—nail these before optimising anything else

🌍 Blue Zone communities live longer through enabling physical environments

🧠 Chronic work and financial stress directly damages healthspan—FI removes one of the most persistent stressors

💰 A longer healthspan changes your FIRE plan in different directions: more active years to enjoy (and fund), but also less healthcare costs near the end

🔑 The compounding approach that works for investing works for health—start early and be consistent

Health & Longevity: Why It Belongs in Every FIRE Plan

Most people who discover and buy into FIRE (Financial Independence, Retire Early) do so because they want more agency over their life: time to live on their own terms, travel, be present for their family, or pursue other interests that are meaningful to them. The financial framework is a means to an end: a longer, richer life is the ultimate goal, even if it looks different for everyone.

Despite this overarching objective, a lot of FI content stops at the instrument. We tend to obsess about whether a 4% or 5% is the right safe withdrawal rate, debate the merits of different ETF providers, and optimize as much as possible our investment portfolios. But then we rarely apply the same rigor and evidence-based thinking to the question of what are we actually going to do with those decades—or whether our bodies will be healthy enough to be capable of living the life we had envisioned.

Health and longevity should not be a separate concern from your Financial Independence journey. Extending your healthspan is, in a very literal sense, extending the return on your FI investment.

There is also a dimension that often gets underemphasized: health matters now too, not just later. At The Good Life Journey, we argue that the journey to FI matters as much as the destination, and this applies equally to the health dimension. A FI journey that grinds you into the ground through overwork can provide you with chronic stress, poor sleep, little movement, and no recovery. You may have projected getting to your FI number faster, but at a cost that you could pay for decades.

Note: the research in this pillar—and the articles it branches out to—draws on the work of leading health and longevity researchers: Dr. Peter Attia, Prof. Andrew Huberman, Prof. David Sinclair Dr. Emeran Mayer, and Drs. Sonnenburg. It also weaves in personal experience: my own observations of what chronic work stress does to the body, and the lived example of my grandparents, who retired at 58, lived to 96 and 97, and unknowingly followed almost everything the science now recommends. Anecdotal, yes, but hard to ignore. The content is interpreted to the extent possible through the same evidence-based lens we apply across this blog, but please remember that I'm not a medical doctor. Nothing here should be taken as medical advice—please consult a qualified healthcare professional before making big changes to your health routine.

The Go-Go years are finite—and they pass faster than you think. The question isn't whether you'll retire, but whether you'll still be capable of being active when you do. Photo by Greg Rosenke on Unsplash.

1. Building the Portfolio Is Only Half the Plan

Why You've Optimised the Portfolio but Maybe Not the Years to Enjoy It

Most FIRE planning focuses on the same side of the equation: how much do we need to accumulate, and how can we be sure to make it last so we don’t run out of money in old age. But not much content applies the same intentionality to the other side of the equation—how many genuinely healthy, active years we’ll actually have to draw from our portfolio before the inevitable decline.

Understanding the distinction between lifespan (total years alive) and healthspan (years lived in good health, free from serious disease and disability) is a central concept of this pillar. Unless you’re very unlucky (think, car crash) our healthspan is almost always substantially shorter than our lifespan—in many countries by a decade or more.

Our final years are frequently lived in varying degrees of illness, disability, and dependency. The constant trips to the doctor (or the trips of the doctor to us) sadly represent a central routine during the last years of life. Suffice to say that they’re not the years you’re imagining when you envision retirement after a long, hard-working career.

Consider the following example: imagine you decided to aim for a $2M portfolio nest egg for retirement, and conservatively plan for a 30-year retirement starting at 65. But then proceed to not take active steps to protect your health; if this is the case, and going by US data, it’s not unreasonable to expect an average of 8 healthy years after retirement.

It makes sense to pause here for a second to think this through: after 4 decades of grinding away, you might only have about 8 good years to enjoy before different types of health issues make your life far less enjoyable. Needless to say, your portfolio will very likely outlast your ability to spend—it’s well documented that spending goes down in the later years of retirement, a concept known as the retirement spending smile. More on this later.

For the FIRE investor that retires at 45, though, the picture looks quite different. In this scenario you have two additional decades of freedom before reaching the conventional age; time that, if invested wisely in your health, can meaningfully extend your healthspan well beyond those averages.

You simply have more time to move, to sleep properly, cook real food, manage stress, and be deliberate about the habits and routines that enable long-term health and longevity. The early retiree who takes their health seriously during those early retirement years is not just enjoying two more decades of freedom, but also enabling a longer and more active life in the later years.

The HALE Numbers — What the Data Actually Shows

HALE (Healthy Life Expectancy at birth) is the World Health Organization's metric that captures years lived in full health—defined as free from the burden of disease and significant disability.

The table below presents HALE alongside total life expectancy for a selection of countries, making the gap between the two visible. The gap represents the number of years in poor health.

Table 1: Healthy life expectancy (WHO, 2019) vs total lifespan across selected countries (UN Population Division data). HALE measures the years lived in good health—free from serious disease and disability. The gap column shows years spent in poor health at the end of life. The colour coding reflects the size of that gap: green for the best performers, amber for mid-range, red for the largest gap. These are national averages; individual outcomes vary significantly based on lifestyle, genetics, and healthcare access.

| Country | Life expectancy | Healthy life expectancy (HALE) | Years in poor health |

|---|---|---|---|

| Japan | 85.0 | 73.4 | ~11.6 |

| South Korea | 84.0 | 73.6 | ~10.4 |

| Spain | 83.9 | 71.1 | ~12.8 |

| United Kingdom | 81.6 | 68.6 | ~13.0 |

| United States | 79.6 | 63.9 | ~15.7 |

Japan and South Korea are some of the leading examples—their residents can expect over 73 healthy years on average, with a gap of around 10-11 years between healthspan and total lifespan.

Among wealthy nations, the US is one of the worst performers by a significant margin—a striking result for the richest country in human history. The US presents a HALE of just 63.9 years against a life expectancy of 79.6—a gap of nearly 16 years. An American can expect roughly a decade fewer healthy years than someone born in Japan or South Korea.

That is not explained by genetics or healthcare systems alone—all these countries have comparatively advanced healthcare. Lifestyle and environment account for most of the difference, factors we cover in detail in sections further below. The gap is large, but it is modifiable for those who put in the effort.

It’s important to stress that these are national averages. As the healthspan article linked below notes: if you're on your FI path and have the time and intentionality to care for your health, you can aim for substantially better numbers. One way to get a more personal picture is to run your own numbers through a longevity calculator—and track them as you improve your health routine.

👉 Deep dive: Invest in Healthspan Like You Invest in Index Funds

But How Many Healthy Years Do You Actually Have After Retirement?

The HALE-at-birth figures above give us one lens. But there’s a second way to explore the data, looking at life expectancy and Hale at retirement. How many years remain after you actually stop working, and how many of those are genuinely healthy?

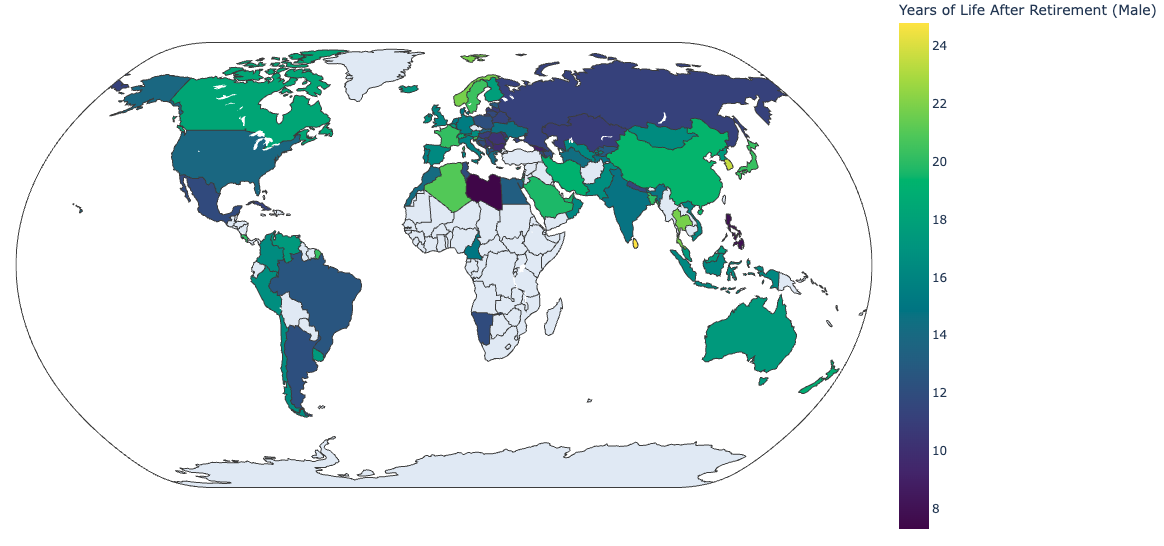

Our second deep dive article maps exactly this across countries (Figure 1). Using life expectancy and HALE at retirement age—rather than at birth—it calculates years of life remaining after the official retirement age, and what share of those years are spent in good health.

Globally, the average man lives around 15 years after the official retirement age; the average woman around 20. But only about 60-75% of those years are spent in good health—measured by WHO's HALE at 60.

Again, for the US, the picture is particularly stark: American retirees spend only about 58% of their post-retirement years in good health—among the lowest figures in the entire dataset.

Figure 1: Years of life after retirement for men across countries in 2021 (men). The variation is striking—in some countries men enjoy over 20 healthy post-retirement years; in others fewer than 10. Source: The Good Life Journey calculation based on official retirement ages and life expectancy at 60. See deep dive for full data and details.

I’m writing this based in Germany, where the official retirement age is 67. The life expectancy at retirement for men in Germany is 14.4 years—but only 9.4 of those in good health. Just nine healthy years after decades of grind. That realization certainly contributed to the decision to move away from a high-stress career much earlier than I otherwise would have.

The maps in the deep dive article bring this to life visually across countries—showing not just how long people live after retirement, but what share of that time is genuinely active. Understanding deep down the large variety of outcomes across countries is very motivating—it means lifestyle does have a major impact on not only improving our life expectancy, but the share of years we’ll spend in good health.

👉 Deep dive: How Long You'll Really Live After Retirement (and How Much Is Healthy)

The Rising Retirement Age Makes the Window Smaller, Not Larger

It’s no secret that across rich countries, the official retirement ages are rising rapidly—pushed by aging populations, shrinking worker-to-retiree ratios, and pension systems under increasing financial pressure. Several countries are moving towards 67-68, while other proposals push already towards 70-71. The most common stated justification is simply that people are living longer, so we need to work longer.

But the critical question is whether healthy life expectancy is rising at the same rate as official retirement ages. The WHO 2000-2019 data suggests it is not—in words of the WHO “the increase in HALE (5.3 years) has not kept pace with the increase in life expectancy (6.4 years).”

If this pattern continues—which is not guaranteed, but is a possibility—the gap between official retirement ages and when you are still healthy enough to fully enjoy it may widen further.

For younger generations like Millennials, Gen Z, Generation Alpha, who will face retirement ages of 68-71 under current policy trajectories, the risk of retiring into the Slow-Go years rather than the Go-Go years is real.

Personally, I view the pursuit of Financial Independence, in part, as a hedge against that risk. It's not only about escaping a job you dislike and providing you with the runway to explore other careers and interests, but also about making sure you are enjoying your healthy years and not just following the script established by others and retiring into poor health.

👉 Deep dive: Retirement Age Rising to 71? Plan Your Early Exit

My Grandparents Figured This Out Before FIRE Had a Name

One of the most vivid illustrations I have of what a long, healthy, and vibrant early retirement looks like actually comes from my own family.

My grandparents retired at 58 and proceeded to live to 96 and 97, giving them nearly four full decades of retirement. Of course, they didn't refer to it as FIRE; they just wanted to enjoy life and they happened to live in a way aligned with almost everything the longevity research now recommends.

Each morning they followed a routine they genuinely looked forward to: early wake-up, a 30-minute walk, swimming laps, jacuzzi, then breakfast. They were unknowingly doing intermittent fasting before it was a thing.

That was how they started almost every day of their retirement. Without knowing it, they were maintaining their aerobic fitness—the single strongest predictor of longevity—almost every day through sustained, moderate-intensity movement.

They ate real food, cooked mostly at home, maintained strong social bonds and kept a sense of purpose throughout. For 95% of their retirement, they kept physically and mentally in great shape; not only through the physical regiment described above, but through strong ties in their local communities (including volunteering) and substantial travel, which was their biggest passion.

But their final years told very different stories from each other. My grandfather, despite dementia in his final years, maintained his gratitude and positive engagement with life all the way to his last breath—he managed to find meaning through connection with others rather than fixating on personal decline. This is what gerontologists call “self-transcendent aging.”

He rarely seemed to experience the regrets common among the dying. In contrast, my grandmother, despite an equally extraordinary life by any measure, struggled a lot in the final years—becoming inwardly focused, preoccupied with her own decline, and losing connection with the people around her.

Watching the contrast was a sad, but powerful lesson that how we orient our minds now in midlife is not completely separate from how our outlook and health trajectory will affect our final stages of life.

Their story is also a reminder for me that a long healthspan is not accidental. It is the compound return on decades of deliberate lifestyle choices—the same way a FIRE portfolio is the outcome of deliberate financial choices.

👉 Deep dive: Lessons on Early Retirement and Healthy Aging From My Grandparents

The average American has just 63.9 healthy years. Those who invest deliberately in movement, nutrition, and stress management can beat that number significantly—and keep doing this well into their 80s. Photo by Nik on Unsplash.

2. What Actually Drives Longevity — The Science

Now that we understand what's at stake, and how large the gap between lifespan and healthspan can vary, the next question is: what actually moves the needle? The science here is much more actionable than most people realize.

Medicine 1.0, 2.0, and 3.0 — A Framework for Thinking About Health

To understand what drives longevity, it helps to understand how medicine has evolved, and where most people’s healthcare is still stuck. We borrow Dr. Peter Attia’s framework for thinking this through.

Medicine 1.0 was the era before germ theory: illness was treated with whatever worked by observation and tradition, with little understanding of any underlying mechanism. It was effective in limited ways, but fundamentally pre-scientific.

Medicine 2.0 is the current standard we all know: evidence-based, highly effective at treating acute conditions and managing established chronic disease. If you have a heart attack, you get treated. If you develop type 2 diabetes, it gets managed. You show up at the hospital or local doctor, share your symptoms, and receive a diagnosis and a treatment plan.

Before going further, it’s worth pausing to acknowledge the merits of this approach. Medicine 2.0 has managed to extend lifespans dramatically: global average life expectancy was just 32 years at the start of the 20th century, but by 2023 it had already reached 73 years, more than doubling in little over a century. Though much of this was driven by very high child mortality, it’s still arguably one of the most remarkable achievements in human history.

According to Attia, though, its main limitation in relation to longevity is that it waits. For the most part, it waits for disease to appear before intervening. Unfortunately, by the time most chronic conditions are diagnosable, they have been developing for 10-20 years, and the opportunity to intervene meaningfully has often passed.

In this context, Medicine 3.0 approaches health in a different way: what if we treated the diseases of aging as preventable rather than inevitable, and intervened decades before symptoms started to appear?

Using a personal finance analogy, you probably wouldn’t wait until you run out of money to start thinking about the sustainability of your portfolio withdrawals in retirement, right? The same logic applies here to health. It means tracking and improving your cardiovascular fitness, metabolic health, and other biomarkers at 35 rather than being surprised by an unfavorable diagnosis at 55.

The Four Horsemen — The Diseases That Actually Kill Us

Dr. Attia identifies four major conditions responsible for the vast majority of death and disability later in life—what he calls the Four Horsemen: cardiovascular disease, cancer, neurodegenerative disease (Alzheimer's, dementia), and metabolic dysfunction. The last one includes issues like insulin resistance, type 2 diabetes, obesity, etc.

We tend to be surprised when some of these come up—say cancer or a stroke—and lament our bad fortune when it does. But Attia argues this is not random misfortune; they develop slowly over decades, and are heavily influenced by lifestyle and usually share the same drivers: poor metabolic health, chronic inflammation, sedentary behavior, and poor sleep. All four are interconnected—for instance, metabolic dysfunction increases cardiovascular and cancer risk, and poor sleep accelerates both metabolic and neurological decline.

The most important takeaway is that we have a lot more agency than we think over these conditions and their outcomes. Almost all of the major risk factors for the Four Horsemen are addressed by the same small number of interventions: aerobic fitness, strength training, sleep quality, and diet. We really don’t need an extraordinarily complex protocol; we just need to get right the fundamentals (the 80/20) and apply them consistently during our lives.

We talk a lot about the portfolio risks to an early retiree (e.g., sequence-of-returns risk), but for a FIRE investor with a 40-50 year retirement ahead an equally important threat to the quality of those years are these Four Horsemen, not only market volatility. If your finances and portfolio are already on track, stop running the 20th simulation on your SWR and apply that same rigor to your health and lifestyle design. For the complete breakdown of each Horseman and the specific biomarkers worth tracking, see our dedicated article below:

👉 Deep dive: Medicine 3.0 and the Four Horsemen: Peter Attia's Case for Treating Disease Before It Starts

You don't need a gym or a structured training plan. What matters is sustained moderate effort most days—zone 2 cardio at a pace where you could hold a conversation but wouldn't want to. Photo by Andrea Piacquadio on Pexels.

VO2max — The Single Most Important Number for Longevity

VO2max is the maximum amount of oxygen your body can use during intense exercise. It’s considered a direct measure of cardiovascular and aerobic fitness. Of all the different metrics that predict longevity, VO2max consistently comes out at the top.

I think most people aren’t surprised when they find out that this factor is relevant, but they are surprised to discover how important it actually is: it’s a stronger predictor than smoking, high blood pressure, or high cholesterol. A 2018 study of over 120,000 adults found VO2max to be the most powerful predictor of survival they identified. Comparing someone of low fitness to elite fitness, there is a five-fold difference in mortality over a decade, which is larger than the mortality impact of smoking, coronary artery disease, type 2 diabetes, or hypertension.

One of the key insights from Attia is that going from a low to an above-average cardiorespiratory fitness produces the same reduction in mortality risk as eliminating end-stage renal disease. You do not need to be an elite athlete; the biggest gains come from just moving out of the bottom quartile.

VO2max declines with age but is highly trainable at any age. The main tools are zone 2 cardio—moderate intensity at a conversational pace, where you could hold a sentence but wouldn't want to, and could still breathe through your nose—and occasional higher-intensity work.

Zone 2 accounts for roughly 80% of training volume in most longevity-focused protocols, with the remaining 20% consisting of harder efforts. If you’re running, this means intervals, hill sprints, tempo runs, or equivalent. But you can find this 80/20 balance in almost any aerobic-focused sport.

Attending a gym is not required; what matters is sustained moderate effort most days, with occasional harder pushes. My grandparents got there through daily walking and swimming laps. I get there through running—which is simply the type of exercise that best fits my schedule.

Resistance Training — The Other Exercise Pillar Most People Underweight

VO2max tends to get most of the attention in longevity discussions, and rightly so—but resistance training is not far behind. While cardiovascular fitness protects mostly against heart disease and all-cause mortality, resistance training preserves all our “physical infrastructure:” muscle mass, bone density, and metabolic function. As you’d expect, all three decline with age, but all three are preserved by regular strength work.

The proxy metric Attia and many other doctors focus on is grip strength. They do so not because a strong handshake matters in itself, but because grip strength correlates well with overall muscle function, balance, and metabolic health. Low grip strength in midlife is a strong predictor of frailty, disability, and cognitive decline in later life. But the strong handshake is the outcome, what matters, of course, is all the process involved in building it.

Ideally, a good resistance routine would look like 2-3 times per week, targeting major muscle groups. Again, although it probably does help, it doesn’t necessarily require a gym. Personally, I have my routine at home following YouTube fitness channels focused on dumbells and barbells.

Beyond the core exercise pillars, practices like cold water exposure and sauna have accumulated meaningful evidence as complementary tools. They support cardiovascular adaptation, reducing inflammation, and improving recovery—though the research base is still at an earlier stage compared to the exercise and sleep literature.

Sleep — The Foundation Everything Else Runs On

Although sleep does not top the longevity statistics the way VO2max does, Attia still makes a compelling case that it is the foundation everything else depends on. In his own protocol, he ranks it even above exercise and nutrition, because poor sleep undermines every other intervention. Just remember the last type you felt genuinely sleep deprived; you probably were not cooking the healthiest meals or engaging in the best exercise routines that day.

Sleep is the chance we get for our brain to clear metabolic waste, including amyloid plaques linked to Alzheimer's. It’s when the body repairs muscle tissue, regulates hormones, and consolidates memory.

Most adults need somewhere between 7 and 9 hours, but the right amount varies by individual. The best signal is simply whether you wake feeling restored or not. Research consistently shows that chronic under-sleeping—whatever your personal threshold need—is associated with increased cardiovascular disease risk, metabolic dysfunction, immune impairment, and cognitive decline

Poor sleep impairs the benefits of both exercise and nutrition: muscle protein synthesis is reduced, cortisol rises, and insulin sensitivity worsens, making the other two pillars less effective. For parents of young children navigating disrupted nights—including yours truly—this is an uncomfortable reality. Hopefully, the situation is temporary, and having the awareness might mean getting back on track as soon as it is possible.

Nutrition — More Complex Than a Diet, Clearer Than You Think

Nutrition research has a reputation for confusion, much of which is well earned. Studies have repeatedly contradicted each other, headlines seem to reverse last year’s advice, and the food industry does fund research that conveniently supports its products.

Despite the noise, researchers from different fields are converging on the same core principles, increasing our confidence in what we can actually do. Some of the clearest researchers and communicators in this space are Dr. Peter Attia, Prof. David Sinclair, and the gut microbiome researchers Dr. Emeran Mayer, and Drs. Justin and Erica Sonnenburg. While they emphasise different angles, the overlap is very striking.

Ultra-processed food is the point of strongest agreement across all frameworks, and the population-level evidence is now consistently associated with worse cardiovascular outcomes, metabolic dysfunction, obesity, and increasingly cognitive decline. Viewed through the microbiome lens, the mechanism becomes clearer: ultra-processed food disrupts gut diversity, and that disruption is one of the strongest drivers of modern chronic disease.

The importance of the gut microbiome has received increasing attention in the last decade. The roughly 38 trillion microorganisms living in your digestive system influences inflammation, immune function, hormone regulation, and is increasingly linked to cardiovascular, metabolic, and neurological health.

Feeding your gut microbiome well means a diversity of plants, fibre, and fermented foods like kefir, kimchi, or kombucha. The gut-brain connection adds a further dimension: the microbiome communicates directly with the brain and influences the body far beyond digestion—affecting inflammation, insulin sensitivity, immune regulation, and neurological function.

In other words, gut health connects upstream to all four Horsemen, with the cardiovascular and metabolic links the most established, and the neurodegeneration connection the most rapidly developing area of current research.

Fasting and caloric restriction is also among the most evidence-backed longevity interventions at the cellular level—activating sirtuins and autophagy pathways associated with cellular repair. The core principle shared across most longevity frameworks is not eating constantly throughout the day; even a 12-hour overnight fast carries measurable metabolic benefits. The most common approach is usually a 16/8 fasting window.

If you want to go all in on the dietary component of longevity, you can follow Bryan Johnson. If you’re just interested in the 80/20 takeaway, and as a partial summary of what we covered, try to focus on the following points:

Minimize ultra-processed food

Eat a wide diversity of plants—variety matters more than any specific superfood

Include fermented foods regularly—yoghurt, kefir, kimchi, fermented vegetables

Eat adequate protein, especially post-40

Consider fasting or a time-restricted eating window—even 12 hours overnight helps

Limit or avoid alcohol

The Blue Zones lifestyles—more on this in further sections below—remain the best real-world proxy for what some of this looks like in practice: broadly plant-based, minimally processed diet, eaten in community, without caloric excess. No macros or overthinking required, but implementing a broader lifestyle that has worked for the longest-lived populations on earth.

All of the interventions above—aerobic fitness, strength, sleep, nutrition—don't just reduce disease risk in the abstract. They measurably change how fast your body is aging at a cellular level. Which brings us to one of the more useful concepts in longevity medicine: biological age.

Your Biological Age May Not Match Your Calendar Age — and You Can Change It

In contrast to our chronological age, which was fixed by the year we were born, our biological age is modifiable, and shows how old our body actually is at a cellular and physiological level.

Biological age tests, which can be based on epigenetics, blood biomarkers, or functional assessments like VO2max and grip strength, can estimate how fast your body is aging. Research shows biological age can differ from chronological age by 10 years or more in either direction—and, as you’d expect, it’s mostly lifestyle interventions that determine it.

The most intuitive illustration at the population level is observing that some people die of “old age” in their 60s, while others are fully active at 90. The gap in biological aging between two people of the same chronological age can plausibly exceed 20-30 years. Two 50-year-olds can have the physiological profile of a 38-year-old and a 62-year-old, respectively, which has important implications for both how many healthy years they have ahead (healthspan) and how long they will live (lifespan).

From a FIRE perspective this is important too. Would-be early retirees tend to obsess over their FIRE number and how fast they can retire—say at 40. But how early is that really if one is in bad health and making poor lifestyle choices that increase your chances of not making it into your 70s?

For FIRE planning, biological age is a more honest input than chronological age when thinking about your retirement. The 50-year-old with the biological age of a 38-year-old has a fundamentally different retirement horizon than the one with a 62-year-old biological age.

Until recently, measuring biological age meant a lab test—epigenetic clocks, blood panels, or a formal VO2max assessment. But wearables have now made it trackable at home and, crucially, actionable day to day: rather than a single annual number, you get continuous feedback on which specific habits are moving the needle and which ones are hurting your health.

I’ve written a detailed personal account (linked below) of tracking my own biological age this way—currently 32 at a chronological age of 39—including the nine factors that drive the score and the exact routine changes that have moved it most.

👉 Deep dive: I'm 39, But My Biological Age Is 32: What I Changed and Why It Matters for FIRE

👉 Deep dive: Should Your Retirement Plan Reflect Your Biological Age?

Manarola, Italy. Part of the region that gave us one of the world’s original Blue Zones. The same environment that makes life beautiful here also makes healthy behaviour the default. Photo by Alexandra Mitache on Unsplash.

3. The Longevity Lifestyle — Environments Over Willpower

While the previous section focused on what to do and the specific interventions that move the longevity needle most—exercise, sleep, nutrition—this section zooms out to ask a different question: why do some people do these things naturally, without effort or discipline, while others struggle to sustain them?

The answer, more often than not, is environment. The world's longest-lived communities are not necessarily more disciplined than the rest of us. They simply live in places that make healthy behaviour the default.

What Blue Zones Show — and Why It Matters More Than Protocols

Blue Zones are regions of the world known for high longevity, where people live significantly longer and healthier lives. The term “Blue Zones” was coined by Dan Buettner, a National Geographic Fellow, who identified the following five regions as Blue Zones (see Blue Zones map below):

Ikaria, Greece

Okinawa, Japan

Ogliastra Region, Sardinia, Italy

Nicoya Peninsula, Costa Rica

Loma Linda, California, United States (specifically, the Seventh-day Adventists community)

Of course, none of these communities follow strict health or longevity protocols. They don’t count macros, measure their VO2max, or subscribe to longevity optimisation communities on Reddit. Their secret is that live in an environment that makes healthy behaviour the path of least resistance.

Some of the key characteristics in these areas are related to constant movement woven naturally into their daily life (think gardening, walking in hilly landscapes, or manual tasks), plant-rich diets low in ultra-processed food, strong social bonds and a genuine sense of community belonging, low chronic stress, a clear sense of purpose that continues into old age, and a slower pace of life. Sounds like a dream, right?

The lesson from Blue Zones isn’t that these communities try harder. It's that they don't have to. Where you live, how you move through your daily environment, and what community you are embedded in can shape health outcomes more reliably than any specific diet or fitness routine you impose on yourself by willpower.

👉 Deep dive: Netflix's Blue Zones Explained: 8 Secrets to Living Past 100

Several Blue Zone Regions Are Also Top FIRE Retirement Destinations

There is very good news for those FIRE investors who considered geoarbitrage and moving abroad in retirement as part of their early retirement strategy. It turns out there is significant overlap between Blue Zone regions and top FIRE retirement destinations.

Costa Rica ranks at the top of our Latin America retirement rankings, while Greece and Italy are present in the top five European destinations. Japan was also highlighted as a very desirable destination for retirees across a wide range of metrics (just not the most inexpensive option).

The health advantage comes from the lifestyle environment found locally in many of these countries: walkable communities, strong food culture, genuine social fabric, and a slower pace that makes healthy behaviour the natural default rather than a daily act of willpower.

The bottom line is that, for those keen on shortening their FIRE timeline, retiring abroad in a Blue Zone environment can not only reduce your annual spending, but introduce you to a daily lifestyle that extends your healthspan—the amount of health years you’ll enjoy in retirement.

👉 Deep dive: Retire Early in a Blue Zone: Where Healthy Aging Meets Lifestyle Design

Alicante, Spain. Spain is one of Europe's most popular retirement destinations and a top-5 pick in our rankings. But southern and easter Spain are already very hot in the summer months, a health consideration that will only intensify in the next decades. Photo by Dean Milenkovic on Unsplash.

Heat as a Health Risk — Where You Retire Shapes How Long You Live

The Blue Zones principle cuts both ways. In the same way the right environment can make healthy behavior effortless, the wrong one can undermine it. Increasingly, climate can be one of those factor to watch out for.

Across the summer months, many parts of Spain, Portugal, Italy, or Greece regularly exceed 35-40°C. As I write this, many regions in these countries already reached mid-30s in May.

Heat stress at these temperatures poses physiological risks: cardiovascular strain, disrupted sleep, heat exhaustion, and reduced outdoor mobility. All these risks affect older adults more. A 55-year-old retiring somewhere in southern Spain today may find those same numbers much more limiting at 75, even before considering the increases we’ll experience in that region from climate change.

Climate projections for southern Europe suggest substantially more days above 35°C by 2050—well within the retirement horizon of anyone retiring today. It’s likely that northern coasts, Atlantic-facing regions, and higher-altitude locations will become increasingly attractive from a health perspective as heat continues to intensify.

When choosing a retirement destination through a longevity lens, climate deserves weight not just for comfort but for long-term health outcomes too. It shapes, after all, what you can actually do with your days, and for how many years.

👉 Deep dive: How Climate Change Will Reshape Europe's Best Retirement Destinations

4. Mental Health, Stress, and the FI Connection

Chronic Stress Is One of the Most Damaging Forces on Healthspan

Chronic stress, understood as a sustained low-level activation of the body's stress response, is a direct driver of multiple Four Horsemen pathways. Elevated cortisol over extended periods accelerates cardiovascular disease, impairs metabolic function, disrupts the quality of our sleep, increases inflammation, and contributes to neurological decline.

The main sources of chronic stress for most working adults are not acute crises, but the sustained presence—sometimes in combination—of financial insecurity, lack of control at work, time pressure, and the inability to fully disconnect. While these may not seem like dramatic stressors in isolation, the fact that they never fully switch off over years is what is concerning.

According to Gallup data, roughly 80% of global workers are disengaged or emotionally detached from their jobs, and 40% report feeling stressed on most days. Viewed through a health lens, that is a large proportion of the working population spending 40+ hours per week under low-grade chronic stress, for careers spanning 30-40 years. Again, the Four Horsemen don’t show up randomly; this is the type of enabling environment in which they develop.

The good news is that pursuing FI can help address this. FI doesn’t just give you time, it also removes one of the most persistent and physiologically damaging stressors in our modern life. For some, lower cortisol, better sleep, and reduced inflammatory markers are the consequences of removing chronic financial anxiety.

From my own experience, after leaving my corporate consulting role—before reaching full FI—Sunday scaries disappeared almost immediately, and stress and baseline anxiety also reduced within months.

For those still in the accumulation phase, mini-retirements offer another way to reduce chronic stress before reaching full FI. They represent intentional recovery periods that prevent the compounding damage of years of sustained overwork. We explore this in detail in the article below.

👉 Deep dive: Only 21% of People Are Engaged at Work. What Does That Mean for the Rest of Us?

👉 Deep dive: Mini-Retirements: Boost Your FIRE Journey with Intentional Breaks

Your Information Diet Is Also a Health Decision

Another important factor affecting mental health is our information diet, which is today delivered by platforms algorithmically optimised for engagement. They are literally designed to capture our attention through outrage, anger, or anxiety—all of which contribute to fuel the same low-grade chronic stress we mentioned earlier. It’s difficult to manage, even when you’re aware of the problem.

Research consistently shows that frequent news consumption during crises is associated with higher anxiety and elevated stress without it necessarily improving our understanding of the situation nor our ability to act on it. The mechanism is fairly straightforward: repeated exposure to threat-signalling information activates the stress response.

If that exposure is near-continuous—as it tends to be with smartphone news feeds today—it contributes to the background cortisol load that, again, drives the Four Horsemen risk. We examine in depth how to stay informed without losing perspective (or your health) in the article below:

👉 Deep dive: The Information Diet: How to Stay Informed Without Losing Perspective

Chronic financial and work stress is one of the strongest upstream drivers of the Four Horsemen. Financial Independence removes one of the most persistent sources of that stress—and the health benefits are often felt immediately. Photo by Mavis M. on Unsplash.

5. Health and Your FIRE Plan — The Concrete Numbers

How Health Shapes the Retirement Spending Smile

Research by economist David Blanchett documents a consistent pattern in retiree spending: the “Go-Go” years (traditionally thought of as roughly 60-75) present the highest discretionary spending—think travel, experiences, hobbies, and generally active living. Eventually the so-called “Slow-Go” years start to creep in (75-85), where we start to observe physical decline. During this phase our spending activity reduces gradually as our daily preferences tend to shift toward wanting to spend more time at home and with our family. Finally, in the “No-Go” years may see a modest spending uptick driven by health and care-related costs. If you plot the spending over time on a chart, you get a curve with a shape of a smile.

Most FIRE plans don't account for this, but simply assume you'll spend the same inflation-adjusted amount from age 45 to 95, which doesn't match how people actually live.

Blanchett's research suggests retirees may be over-saving by around 10-20% relative to what they actually need. This means in practice working several extra years to build a portfolio that will go largely unspent. Bill Perkins’ Die With Zero author would argue you’re trading healthy years of life for money that arrives too late to be used.

For FIRE investors, of course, the spending pattern is slightly different, because the spending smile is shifted to later in life. If you retire at 45 rather than 65, you dramatically extend the Go-Go phase—you may have 30-35 years of very active lifestyle ahead of you, not 10-15 of traditional retirees.

The practical implication is not necessarily to dramatically reduce your FI number early on or to reduce your safe withdrawal rate, but to revisit the picture around age 60, when the Slow-Go transition begins to approach. Depending on where you are at financially, you could consider front-loading spending into those remaining active years. We address the issue of what to do with the final healthcare costs further below.

Outside the US, and specially in countries with solid public healthcare systems, the spending smile may not really apply. If you plot the spending on a chart it might look more like a smirk—a steady decline without a very strong uptick towards the end. The reason is that publicly-funded healthcare (or more reasonably priced private healthcare) absorbs much of the late-life cost increase that drives the US smile shape.

This may give European FIRE investors even more confidence that actual lifetime spending will be lower than flat projections using fixed withdrawal rates suggest. We cover this in detail in our Die With Zero summary—including the case for front-loading experiences into your healthiest years rather than smoothing spending across a full retirement.

👉 Deep dive: Retirement Spending Smile: What It Is, Why Spending Drops, and How to Plan

A Healthier Life Changes Your Retirement in Both Directions

While the spending smile describes the general trajectory, your personal health determines what it will look like in practice. A longer healthspan doesn't simply add years, but extends the Go-Go phase, compresses the Slow-Go decline, and shifts the entire curve to the right.

But on the other hand, a longer, healthier life also means more retirement years to fund. A 45-year-old who invests seriously in their health and reaches their late 80s or 90s in good shape has a 45-50 year retirement to consider.

The key insight is not to think of health investment as adding more years of expensive decline, but as extending the Go-Go years, compressing and delaying the Slow-Go and No-Go years, and arriving at the final phase of life later and in better condition.

The research term for this is compressed morbidity, which reflects an active and independent life, then a much shorter, concentrated decline. It is the opposite of the Western default of long, gradual deterioration, and it is primarily a function of lifestyle choices made across the preceding decades, not just genetics or luck.

Nursing Costs — The Tail Risk Worth Planning For

Nursing care is a specific, concentrated cost event that may occur over a 2-4 year window at the very end of life, and which sits on top of the otherwise declining baseline.

In Europe, nursing home costs vary by country but are generally rising. In Germany, for instance, residential care currently costs €3,000-5,000 per month, with the State covering a meaningful but partial share.

Remember though, that when you transition to a nursing home, that will be your total cost, because it’s typically a room and board situation that covers everything. So, for many retirees the monthly spending may not be dissimilar to their monthly cost before this transition. In contrast, for Lean FIRE folks, this is certainly an expense to prepare for.

In my view, the right response is not to work five or six extra years building a vastly larger portfolio and implement a lower withdrawal rate as a buffer against a 2-4 year scenario which could potentially never materialize. Instead, consider insuring that event for peace of mind; specifically, a small Deferred Income Annuity (DIA) purchased at 60-65, with payments beginning at 80 or 85, can provide a guaranteed income floor for those final years.

We cover this in detail in the annuities article below—the key insights are that, firstly, insuring the tail risk gives you the psychological permission to spend more confidently across all the decades that precede it and avoids you extending your working career unnecessarily. Secondly, this type of annuity (DIA) is efficient because it uses mortality credits to your advantage—assuming you are healthy and live longer than average, it can be a cheap way to protect your peace of mind.

The most powerful hedge remains health itself. People who invest seriously in physical function, metabolic health, and cognitive resilience tend to experience what researchers call “compressed morbidity”: they remain genuinely independent and active well into their 80s and 90s, in many cases declining over months rather than years.

👉 Deep dive: Rising Nursing-Home Costs in Europe: What They Mean for FIRE

👉 Deep dive: Can Annuities Ever Make Sense for FIRE Investors?

Putting It All Together — Health as Part of Your FIRE Framework

The central argument of this article is straightforward: the same evidence-based, compounding approach that we use for building a FIRE portfolio should be applied for building a long and healthy life.

Start early, be consistent, focus on the highest leverage actions (the 80/20), and don't rely on willpower alone—instead build systems and environments that make the right choices the easy ones.

We should see health and FI not as competing priorities, but as two sides of the same coin. Ultimately, they’re both part of the same project we’re building: the portfolio funds the life, but the health determines whether you are capable of living it to its fullest extent and how long you’ll enjoy those portfolio returns.

A FIRE investor who reaches their FI number at 45 with poor metabolic health, chronic inflammation, and a sedentary lifestyle may have managed to successfully build the financial instrument needed to retire early, but they neglected the very purpose it was meant to serve.

Invest in the big four—VO2max, resistance training, sleep, and diet—and choose your environment deliberately. Where you live shapes your health outcomes more than any individual protocol. Walkable neighbourhoods, natural movement opportunities, real food, and a genuine sense of community are all health infrastructure, not just a lifestyle preference. The Blue Zones centenarians didn't get there through willpower alone; they were helped by their enabling environment.

Plan your retirement spending honestly. The smile pattern is real, so don’t overestimate how much you need to retire. When possible, front-load experiences into the Go-Go years, and revisit your situation carefully at 60. Consider insuring the tail risk through deferred income annuities cheaply rather than over-saving (and over-working) for a high-spend situation that may or may not ever materialize.

Finally, don’t sacrifice the journey for the destination. A FIRE path that grinds you into the ground during the accumulation phase of FI is not only making your life miserable then, but also setting you up potentially for an early retirement in suboptimal health and/or for a shorter life.

The same intentionality we applied to building our FI journey applies also to the health side of things—and we should apply it now, not in the future when we’re FI. My grandparents, who walked and swam laps every morning of their four-decade retirement, ate real food, kept their social connections, and travelled until their late 80s, understood intuitively that a long, healthy life is the compound return on decades of deliberate daily choices.

The earlier you start making them, the more the compounding will work in your favour.

If you enjoyed this guide, here are some next steps:

👉 For the science behind preventing the Four Horsemen, see our article on Medicine 3.0

👉 For the longevity lifestyle in practice, see Retire Early in a Blue Zone

👉 For the spending side of retirement, see Retirement Spending Smile

👉 Use our FI Calculator to model your early retirement timeline (email unlock)

👉 Subscribe for weekly insights—one-click unsubscribe

👉 Browse 130+ articles on FI, investing, work, and lifestyle at The Good Life Journey

🌿 Thanks for reading The Good Life Journey. I share weekly insights on personal finance, financial independence (FIRE), and long-term investing — with work, health, and philosophy explored through the FI lens.

Disclaimer: I am not a financial adviser, and this content is for informational and educational purposes only. Please consult a qualified financial adviser for personalized advice tailored to your situation.

Check out other recent articles

About the author:

Written by David, a former academic scientist with a PhD and over a decade of experience in data analysis, modeling, and market-based financial systems, including work related to carbon markets. I apply a research-driven, evidence-based approach to personal finance and FIRE, focusing on long-term investing, retirement planning, and financial decision-making under uncertainty.

This site documents my own journey toward financial independence, with related topics like work, health, and philosophy explored through a financial independence lens, as they influence saving, investing, and retirement planning decisions.

Frequently Asked Questions (FAQs)

-

Healthspan is the number of years you live in good health — free from serious disease, disability, or dependency — as distinct from total lifespan. For FIRE investors, healthspan is more important than lifespan as a planning input, because it determines how many years of your retirement you'll actually be capable of living actively. WHO data shows the average American has around 63.9 healthy years — meaning most people exhaust their healthy years around traditional retirement age, before they've had the chance to enjoy early retirement. Investing in healthspan is, in a direct sense, extending the return on your FI portfolio.

-

VO2max is the maximum amount of oxygen your body can use during exercise and is the single strongest predictor of all-cause mortality across the research literature — stronger than smoking, blood pressure, or cholesterol. A 2018 study of 122,000 adults found those in the lowest fitness category had five times the mortality risk of those in the highest. The biggest gains come not from elite fitness but from moving out of the bottom quartile. Zone 2 cardio — sustained moderate-intensity exercise at a conversational pace — is the primary tool for building and maintaining VO2max, and it can be achieved through running, swimming, cycling, walking, or almost any sustained aerobic activity.

-

The retirement spending smile, documented by economist David Blanchett, shows that retirees typically spend the most in the active Go-Go years, less in the Slow-Go years as activity naturally decreases, and may see a modest uptick in the No-Go years due to care costs. Assuming flat, inflation-adjusted spending throughout retirement — as most 4% rule calculations do — tends to overestimate actual spending needs by 10-20%. For FIRE investors with very long horizons, the smile shifts later in life, but the principle still applies: revisit your actual spending needs around age 60 and consider front-loading experiences into your remaining active years.

-

Dr. Peter Attia identifies four conditions — cardiovascular disease, cancer, metabolic dysfunction (including insulin resistance, type 2 diabetes, and obesity), and neurodegenerative disease (including Alzheimer's and dementia) — as the primary drivers of death and disability in later life. He calls them the Four Horsemen because they account for the vast majority of chronic disease burden, develop slowly over decades, and share common upstream drivers: poor metabolic health, chronic inflammation, sedentary behaviour, and poor sleep. Almost all major risk factors for the Four Horsemen can be meaningfully reduced by the same cluster of interventions: aerobic fitness, resistance training, sleep quality, and diet quality.

-

Chronological age is fixed by your date of birth. Biological age reflects how old your body actually is at a cellular and physiological level — based on factors like VO2max, metabolic markers, grip strength, and epigenetic methylation clocks. Research shows two people of the same chronological age can have biological ages 20-30 years apart, depending on their lifestyle history. This gap has direct implications for FIRE planning: a 50-year-old with a biological age of 38 has a fundamentally different retirement horizon, spending trajectory, and health cost profile than one with a biological age of 62. Biological age tests — through epigenetic kits or comprehensive blood panels — can give a more personalised picture than national HALE averages.

-

Blue Zones are five regions identified by researcher Dan Buettner where people live significantly longer and healthier lives than average: Ikaria (Greece), Okinawa (Japan), Sardinia (Italy), Nicoya (Costa Rica), and Loma Linda (California). Their defining characteristic is not discipline but environment — communities where healthy behaviour is the natural default through walkable design, plant-rich food culture, strong social bonds, and a slower pace. Several Blue Zone regions appear among the top-ranked FIRE retirement destinations — Costa Rica tops our Latin America rankings, Greece and Italy are in the top five European destinations. For FIRE investors, retiring in a Blue Zone-adjacent environment can simultaneously reduce spending, improve the FI timeline, and extend healthspan.

-

Yes — and the mechanism is specific. Chronic low-level stress keeps cortisol elevated over extended periods, which accelerates cardiovascular disease, impairs metabolic function, disrupts sleep quality, increases systemic inflammation, and contributes to neurological decline — all upstream drivers of the Four Horsemen. Gallup's 2025 State of the Global Workplace data shows 80% of global workers are disengaged or emotionally detached from their jobs, and 40% report feeling stressed on most days. Viewed through a health lens, that represents a large proportion of working people spending 40+ hours per week under low-grade chronic stress for careers of 30-40 years. Pursuing Financial Independence removes one of the most persistent sources of this chronic stress load.

-

Nursing home costs in Europe are rising but are frequently lower than their US equivalents, partly because publicly-funded systems absorb a significant share. In Germany, residential care currently costs €3,000-5,000 per month, with Pflegeversicherung covering part of the cost. The key planning insight is that nursing care is typically a concentrated 2-4 year event near end of life — not a decades-long baseline. The most efficient response is not working extra years to build a larger portfolio as a buffer, but targeted insurance: a small Deferred Income Annuity (DIA) purchased at 60-65 with payments beginning at 80-85 can insure the tail risk cheaply and give the psychological permission to spend more confidently across all the preceding healthy decades.

-

Compressed morbidity, first described by Dr. James Fries at Stanford, refers to the pattern where people who invest seriously in their health tend to remain functionally independent and active until relatively close to death — experiencing a shorter, more concentrated period of decline rather than the long gradual deterioration typical in Western populations. Blue Zone centenarians are the clearest examples: many remain active into their late 90s and then decline over months rather than years. For FIRE planning, this means the expensive, prolonged residential care scenario is disproportionately a consequence of poor health across preceding decades — not an inevitable feature of a long life.

Join readers from more than 100 countries, subscribe below!

Didn't Find What You Were After? Try Searching Here For Other Topics Or Articles: