FIRE for Late Starters: The Real Math of Starting at 40, 45, or 50

Starting later sometimes means a steeper climb—but the summit is still very much within reach. Photo by Jens Herrndorff on Unsplash.

Reading time: 7 minutes

FIRE for Late Starters: The Real Math of Starting at 40, 45, or 50

Quick answer:

While the stereotype of the FIRE (Financial Independence, Retire Early) movement is a tech bro retiring in his mid-30s, discovering Financial Independence (FI) at 40, 45, or 50 is far more common than most people realize.

The math is also not as bad as most late starters think. You won’t retire at 35, but you probably don’t need the full 25x expenses either that the 4% rule suggests: you’re closer to pension age, your retirement budget is likely smaller than today’s spending, and other levers we’ll explore like the 1% method, geoarbitrage, and peak-career earnings can all work in your favor. Today, we’re not only delivering a dose of motivation for late starters, but also covering different concrete solutions and levers that will substantially accelerate your timeline to Financial Independence.

What You'll Get From This Article

✔ The math of starting your FI journey at 40+

✔ Why to avoid comparing yourself to Reddit’s 30-year-old tech retirees

✔ Why trying to gamble your way to catching up usually backfires

✔ The levers that genuinely accelerate the timeline: the 1% method, housing, geoarbitrage, and more

✔ The structural advantages late starters have that shrinks their real FI number

✔ Health as the great equalizer: extending both the length and quality of the retirement

TL;DR — FIRE for Late Starters 🕰️

📊 40+-year-olds can still reach FI in 13-15 years—later than the Reddit stories, but still impressive

🎰 Resist the “catch-up” gamble of leaning in too strongly on crypto, leverage, or stock picks

📈 The 1% method: raise savings rate 1% point per month—imperceptible, yet transformative

🏠 Consider the housing lever: downsizing can cut your budget more than any other single move

💶 You’re closer to pension age—the two-phase math can cut your required FI number by ~25%

⏳ You likely need less than 25× expenses—pension math + a lower retirement budget shrink the target

🌍 Geoarbitrage can nearly halve the timeline if you’re willing to relocate

🏃 Savings rate determines how fast you reach FI; health determines how many years you enjoy it

🧭 Compare yourself to your own baseline—not to a tech bro who started at 24 in the US

Discovering FIRE at 45 Isn't Too Late — But It Is Different

The stereotype profile of the FIRE (Financial Independence, Retire Early) movement is a 32-year-old software engineer who saved 65% of a tech salary in the US for under a decade and now boasts about it on Reddit or YouTube. Good for them, but it’s important to remember that the San Francisco case is far from the average story of people working towards FI.

It’s a classic example of survivorship bias at play: these early success stories are disproportionately more likely to share blog posts and record videos sharing their journey, while far more common stories of achieving FI over a 20-25-year period rarely get highlighted.

And yet it’s a far more common profile: someone who stumbles across the concept of FI at 42 or 47, oftenthrough a friend, news article, or podcast. They do the initial math with growing excitement, only to find out that even with drastic changes they’re looking at a mid-to-late 50s retirement. Somehow, retiring at 59 doesn’t sound so FIRE anymore—and it still means more than a decade of grinding to get there.

If you add to the equation the fact that many of these 40-something-year-olds have a mortgage, kids, and a lifestyle with years of momentum behind it, you can see how the motivation around the project of pursuing early FI may fall apart pretty quickly.

But hang in there for a moment. If that is you, be sure to read this whole post before throwing in the towel. My hope is not only that you leave with a high dose of motivation, but that you fully understand the available levers to make this FI journey a faster one than you may have originally estimated.

I’ll be upfront that I didn't start at 45 myself—but spent a long time modeling these exact scenarios, and the levers I explain further below are the ones I’d genuinely reach for if I were starting my FI journey today in my mid-40s.

Most late starters overestimate what they need—until they sit down and model it properly. Photo by Jakub Żerdzicki on Unsplash.

The Late Starter Reality — and Why the Standard Playbook Stings

At its basic core, the FIRE playbook is built around a young person’s flexibility. Increase the gap between what you earn and what you spend, invest the difference into low-cost, internationally-diversified index funds or ETFs that track them, automate everything, and stay patient. With a high savings rate, this simple formula allows you to retire decades early.

We cover these foundations in our guide to what Financial Independence actually is. While the math doesn’t change at 45, what does change is the context around it. A 26-year-old can live like a student for another decade without much friction: flatshares, no dependents or major responsibilities, and a lifestyle that hasn’t gotten expensive yet.

In contrast, a 45-year-old with a family, mortgage, school and holiday routines, and fifteen years of accumulated commitments finds it much harder to make drastic financial changes. At 26, cutting your spending by 30-40% may feel like an experiment, and be genuinely exciting because you understand the upside if you do. But at 46, it’s also a negotiation with your spouse and people you love, and there are real trade-offs to consider.

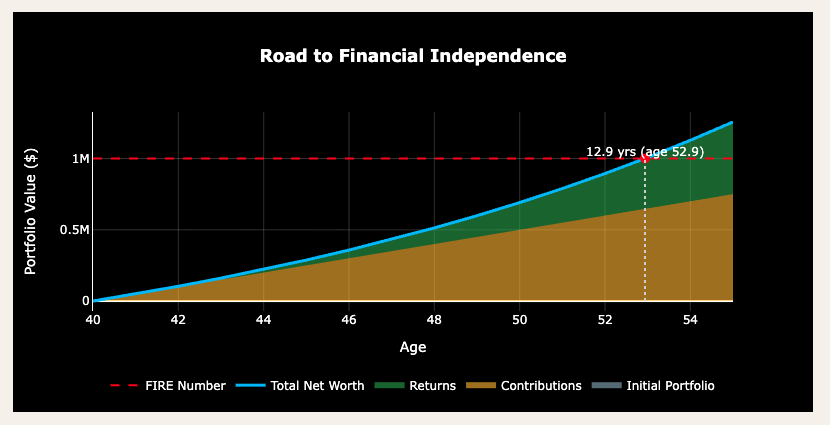

Starting at 40 with little savings, a genuinely aggressive 50% savings rate would get you to FI in roughly 13-15 years. As observed in Figure 1, a 40-year-old could realistically retire at 53, and a 45-year-old at 58, still way ahead of the curve.

Figure 1: Financial Independence timeline of a 40-year-old with no savings that decides to implement a 50% savings rate. They are able to retire in roughly 13 years at age 53. Source: our free Financial Independence Calculator (email unlock). Assumes 7% real returns from portfolio and a 5% safe withdrawal rate in retirement.

While against the traditional retirement age of 65-67, that’s an impressive result—about a decade more of freedom—when you measure it against FIRE stories on Reddit, it can sting.

This is the reason why, before going into the levers that can speed up your timeline, the most important adjustment to make for a late starter isn’t financial, but psychological: to what benchmark are we going to be comparing ourselves to?

It sounds cliché but comparison really is the thief of joy. Comparing yourself to someone who found out about this concept in their early 20s is both unfair and not helpful. The right comparison to make instead is your own counterfactual, i.e., the version of yourself who never found out about FI or who decided not to implement it. The benchmark is retiring in your mid-60s, not mid-30s.

Measured against the right counterfactual, everything you do from this point forward is pure gain.

The Catch-Up Trap — Why Taking More Risk Usually Backfires

Unfortunately, there’s a predictable pattern that shows up amongst late starters feeling behind: the attempt to substantially compress a 15-year timeline by taking on additional risk.

This shows up in different strategies that try to accelerate the FI path via chasing returns: an outsized crypto allocation, leveraged ETFs, concentrated bets on individual stocks expecting moonshots, or going all-in trying to build a small property empire with maximum debt.

The logic does feel compelling: why accept average 7% market returns for 15 years when—surely—enough effort could beat the market? After all, you’ve heard about others who’ve done it successfully, and there simply isn’t time for the conventional, boring path to FI.

Unfortunately, the math works the other way around. While there are cases of gambling working out, again, beware of survivorship bias and don’t forget about the majority of cases who tried the same strategy, failed, and went underreported.

Investing can be frustrating because it’s one of the few areas in life where the more effort you put into it, the worse outcome you’re likely to get. And taking on more risk cuts both ways; a late starter is precisely the profile who cannot absorb the downside. A 28-year-old who loses half their portfolio in a leveraged bet still has decades of income ahead to repair the damage, while a 50-year-old may turn his “FI by 57” into “working until 70.”

Besides trying to aggressively beat the market, there is another “catching up” version that is fairly common amongst late-starters: trying to brute-force the timeline through sheer work intensity. You’re so pumped that you decide to work even harder— perhaps take every promotion available regardless of stress or health considerations or add a side hustle on top of your regular job to increase your income.

This type of sprinting for a few years is survivable in your 20s, but sustaining it in your late 40s or early 50s with a family that needs you and a body that is less resilient than it once was, is a recipe for arriving at FI burned out and in poor health. This defeats the entire purpose of pursuing FI, which is ultimately to lead a better life. We’ve written before about what chronic work stress actually costs, and the price only increases with age.

The approach that actually works is more boring: keep costs low, push your savings rate up, put the difference into low-cost, broad index funds, and automate the whole process. We cover the details in our guide to how to invest for FI.

Alright, so we’ve covered what doesn’t work, but are there some levers we can reliably pull to shorten the timeline to FI for late-starters? We cover four different options to consider in the following sections.

The 1% method in one image: adjust your savings rate one step at a time, and before you know it you turn around and appreciate the progress you’ve made. Photo from Kunal Singh on Pexels.

The 1% Method: Raise Your Savings Rate Painlessly

If taking on more risk isn’t the answer, what could actually accelerate the FI timeline for late-starters?

The first lever is the 1% method. The biggest obstacle for a late starter isn’t knowledge on what needs to be done to pursue FIRE, but the shock that a sudden change in lifestyle represents. The solution could be to try to make these changes as invisible as possible by increasing your savings rate very slowly over time. As the method’s name suggests, try increasing your savings rate by one single percentage point per month.

For instance, on a $6,000 monthly income with $5,400 of spending (a 10% savings rate), the first month would ask you to save just 1% more—$60—trimming spending to $5,340, a change small enough you’d barely notice it. Perhaps it’s one less meal out that month or one annual subscription that you barely use.

The advantage of this approach is that you make these changes easier to implement. Because humans adapt easily to small changes, nobody notices the 1% changes from month to month. Thanks to hedonic adaptation, you realize you are just as happy in month 6 as you were in month 1.

But twelve months later you may find yourself saving 12 percentage points more of your income (a 22% savings rate), and after two years, 24 more (a 34% rate). The advantage of this simple approach is that going slowly gives you time to find each cut without feeling pressured: one month you finally re-quote the insurance you’ve had for years, another you cancel the subscriptions nobody uses, then you notice the grocery bill has crept up, or you switch to a cheaper provider for the same service.

Instead of slashing everything at once and resenting it, you’re slowly hunting down the next bit of low-hanging fruit—which is a far more sustainable way to change how you spend.

The caveat is that if your income is not high, this method probably won’t allow you to reach the 50%+ savings ratethat 20-year-olds or tech workers are using, but it still moves the needle very substantially in your favor: going from a 10% savings rate to a 35% one can aggressively shorten your timeline.

The Housing Lever: Downsizing Can Buy You Years

The second lever worth mentioning is housing. No single category moves more money than where you live. This is especially true in the US, where houses have inflated to sizes that anyone living in other countries finds mind-boggling. It’s not hard to find situations where couples in their early 50s are living and maintaining a house that was built for a family of 5 (or for 3 families, if you consider the perspective of someone living in Europe).

The empty-nest house or the stereotypical McMansion is a real wealth drain: heating, utilities, maintenance, property taxes, and time are all costs paid annually for rooms that nobody is using. Downsizing in some cases can represent the largest acceleration available to a late starter, with the double impact of not only simultaneously releasing home equity into investments but also cutting annual expenses aggressively.

I’m aware this won’t apply to everyone, but if you’re a late starter in a large house with children close to launching, consider re-running the numbers with different housing arrangements before dismissing the idea entirely.

Your Peak Earning Years Are a Lever Too

The next lever is focusing on the income side. Someone in their mid-40s to mid-50s is likely in their peak earning years. While a lot of the FIRE content (including my site) tends to focus more on the frugality levers available, we shouldn’t forget that late starters usually have much more career capital than 20 and 30-year-olds.

By career capital I mean the accumulated skills, reputation, professional network, and track record that make you difficult and expensive to replace. This capital is your leverage, and often a strategic job change in this stage of a career can land you a large salary jump.

A late starter who negotiates salary seriously, changes employers at the right moments, and redirects every raise straight into investments can move their FI timeline as much from the income side as from a decade of frugality. The gap between what you earn and what you spend has two sides—and in your peak years, the earning end is a powerful lever to pull.

For US readers, there’s an extra structural boost worth mentioning: once you turn 50, retirement accounts let you make catch-up contributions—several thousand dollars a year above the standard 401(k) and IRA limits, with recent legislation expanding this further into your early sixties. So, if you’re 50+ and earning peak income, that’s a lot of extra tax-advantaged room to shelter your aggressive late-stage savings. Limits adjust yearly, so it’s a good idea to check the current figures.

Coastal town in Italy. Plenty of places worldwide offer both a lower cost of living and a higher quality of life—see our rankings for retirement destinations across Europe, Asia, and Latin America. Photo by Mike L on Unsplash.

Geoarbitrage Can Nearly Halve Your Timeline

Engaging in geoarbitrage could nearly halve your FI timeline. Say your FI number is 25x of your annual expenses (or, as we’ll see in the next section, less). Of course, the number depends enormously on where you live. A budget requiring €1.5M in the US may require 30-40% less in many high-standard European countries, and much less if you consider Asia or Latin America.

For a late starter, that’s not a marginal improvement. Moving to a lower cost-of-living (COL) location—either within your country or abroad—can literally compress your “FI at 58” into “FI at 51”.

I’m aware that relocation isn’t for everyone and that family, friendship ties, and community matter and deserve an honest weight in the decision. But it’s still a lever worth thinking about, considering the enormous impact it can have. Our free Retirement Relocation Tool (email unlock) lets you find your perfect retirement location abroad.

Even a partial version of this can help: either just relocating in your country, or splitting the year seasonally between home and a cheaper base. We explore this further in our article on seasonal geoarbitrage.

Your FI Number Is Smaller Than You Think

Everything so far has accepted the premise that late starters face a harder road ahead. But there is one angle that may make it comparatively easier than building your FI path from scratch in your 20s or early 30s: your real FI number is likely smaller than the conventional 4% rule of thumb suggests (i.e., needing to accumulate 25 times your annual expenses)—for two different reasons.

First, the two-phase math. The standard 25× figure, derived from the 4% rule, assumes your portfolio must fund you forever. But many late starters are close enough to receiving state pension or Social Security age that the problem splits in two: a “bridge” period funded exclusively by your portfolio, and a later period where the pension kicks in too.

Because your portfolio doesn’t have to cover your full spending for life—just bridge you to pension age and then supplement it—the capital you actually need can be meaningfully lower than 25×—often on the order of 20-25% less. Of course, this depends heavily on your pension entitlement and when it starts—which varies both across countries and individual circumstances. We’ll break down the full math in a dedicated post soon, but it’s good to be aware of the need to model this on a case-by-case basis.

Second, your retirement budget is probably smaller than today’s spending. Most would-be retirees tend to apply the 4% rule (or another safe withdrawal rate they’re comfortable with) to their current expenses, ignoring that these are usually inflated by work itself: the commuting, second car, convenience meals, professional wardrobes, and even outsourced tasks you’d happily do if you had the time. For many, kids out of the house also means a substantially lower budget.

On top of that, the “retirement spending smile” shows that real spending tends to drift down through retirement rather than stay constant with inflation—this reflects the three classic periods of retirement: the “Go-Go years”, followed by the “Slow-Go”, and the “No-Go.”

All this considered, many late starters find that their true target portfolio is much lower than what rules of thumb in the FIRE space would suggest.

Health: The Lever That Extends the Prize Itself

Before moving onto the next article, I’d like to finish with a final reframe I think many late starters should consider. Retiring at 55 is only “late” chronologically (and in a very niche FIRE space). However, chronological age isn’t what actually ends up determining the length and quality of your retirement. It’s your biological age which will largely determine it.

The levers we presented above improve your retirement by helping you reach it sooner. But health improves it from the other end—by extending how many good years you get out of your portfolio. Consider that US male life expectancy is around 76, an average dragged down substantially by lifestyle factors you can start changing today.

Someone who arrives at 55 with the biological age of a 45-year-old is starting a fundamentally different retirement than one arriving at 55 with the body of a 65-year-old. We’re not just talking about more years, but higher-quality ones, and usually followed by a comparatively shorter decline at the end. Who’s not on board for all that?

So, focus on the levers to shorten the FI timeline on this side, but don’t forget to prioritize health and longevity to build your best possible retirement. In my view, health is the other half of the FIRE equation.

I hope that today’s article convinces you that starting at 40, 45 or 50 is not the disadvantage it may have felt like at first—it just calls for using different levers smartly.

If you enjoyed this article, here are some next steps:

👉 Model your timeline to early retirement with our free FI Calculator (email unlock)

👉 See how much less you might need: read about the Retirement Spending Smile

👉 Cut years off the timeline with location: Geographic Arbitrage & FIRE: The Complete Guide

👉 The other half of the plan: Health & Longevity

👉 Access all of our articles in our Archive

👉 Subscribe for weekly insights—one-click unsubscribe

🌿 Thanks for reading The Good Life Journey. I share weekly insights on personal finance, financial independence (FIRE), and long-term investing — with work, health, and philosophy explored through the FI lens.

Disclaimer: I am not a financial or legal adviser, and this content is for informational and educational purposes only. Please consult a qualified financial adviser for personalized advice tailored to your situation.

Check out other recent article

About the author:

Written by David, a former academic scientist with a PhD and over a decade of experience in data analysis, modeling, and market-based financial systems, including work related to carbon markets. I apply a research-driven, evidence-based approach to personal finance and FIRE, focusing on long-term investing, retirement planning, and financial decision-making under uncertainty.

This site documents my own journey toward financial independence, with related topics like work, health, and philosophy explored through a financial independence lens, as they influence saving, investing, and retirement planning decisions.

Frequently Asked Questions (FAQs)

-

No — starting FIRE at 45 is far more common than the movement’s public image suggests, and the math is better than most assume. With an aggressive savings rate you can still reach financial independence in your late 50s, and levers like geoarbitrage, the two-phase pension math, and a smaller retirement budget can pull that in further. The key shift is psychological: measure yourself against your own counterfactual, not a 30-year-old who started at 24.

-

Starting at 40 with little saved, a 50% savings rate gets you to FI in roughly 13-15 years — retiring around 53. But your real target is often lower than the standard 25× expenses suggested by the 4% rule, because you’re closer to pension age (which covers part of your later spending) and your retirement budget is usually smaller than today’s work-inflated spending. Modeling both with a calculator gives a more honest number.

-

The 1% method means raising your savings rate by a single percentage point per month rather than making one drastic lifestyle change overnight. On a $6,000 income at 10% savings, month one asks for just $60 more — barely noticeable thanks to hedonic adaptation. Twelve months later you’re saving 12 points more; after two years, potentially 24. It turns an intimidating overhaul into a series of painless steps.

-

Because risk cuts both ways, and late starters can least afford the downside. A 28-year-old who loses half their portfolio has decades of income to recover; a 50-year-old doing the same can turn "FI by 57" into "working until 70." Crypto bets, leverage, and concentrated stock picks feel like shortcuts but usually backfire — the boring index-fund path remains the reliable one.

-

Often no. The 25× figure assumes your portfolio funds you forever, but a late starter is close enough to state pension or Social Security that the problem splits into two phases: a bridge period your portfolio covers alone, then a period where the pension supplements it. This “two-phase math” can reduce the capital you actually need by roughly 20-25%.

-

Usually yes. Current expenses are inflated by work itself — commuting, a second car, convenience meals, professional wardrobes, outsourced chores — much of which disappears in retirement. Kids leaving home lowers it further for many, and the “retirement spending smile” shows real spending drifts down over time rather than rising with inflation. Many late starters find their true target is meaningfully below today's budget.

-

Significantly. Because your FI number is a multiple of your expenses, and expenses depend heavily on location, moving somewhere cheaper can compress the timeline dramatically — a budget needing €1.5M in the US might need 30-40% less in parts of Europe. Even partial versions help: relocating within your country or splitting the year seasonally between a home base and a cheaper one.

-

Yes, several. You’re in your peak earning years with the most career capital, giving you strong leverage on the income side. You need less capital thanks to the two-phase pension math and a lower retirement budget. And you know yourself — a 48-year-old usually knows exactly what they want retirement for, often avoiding the expensive mistake of reaching for a number that is too high.

-

Health determines the length and quality of the retirement you’re saving for. Chronological age is only half the picture — someone arriving at 55 with the biological age of a 45-year-old gets more active years and a shorter decline. The habits that produce this (aerobic fitness, sleep, strength training) are buildable in the same years you’re saving, and they compound like a portfolio.

-

Higher is better, but you may not reach the 50%+ rates of young tech workers — and you don’t necessarily have to. The 1% method can lift you from 10% to 35% over two years, which dramatically shortens the timeline on its own. Combined with geoarbitrage, peak-earning income, and a lower real FI number, a moderate-but-rising savings rate can still get you to an early retirement.

Join readers from more than 100 countries, subscribe below!

Didn't Find What You Were After? Try Searching Here For Other Topics Or Articles: